- Singapore fell into a deep recession in the second quarter this year, driven by a severe hit on its exports and deeply globalized services sectors due to the Covid-19 pandemic.

- The economic recovery back to pre-Covid levels might take longer than its Asian peers. Singapore's past economic resilience, which stemmed from its deeply globalised services-oriented economy (finance, air travel, shipping and hospitality) is being greatly tested by the nature of the Covid-19 induced slowdown.

- While Singapore equities are cheaply valued, we think the impetus for a meaningful re-rating maybe lacking ahead, due to (i) mediocre economic growth expectation, (ii) lacklustre earnings growth and (iii) challenges facing STI constituent companies.

- Singapore's high dividend yield of 3.6-4.5% means that investors will remain adequately compensated while waiting for prices to recover. We also expect an attractive upside potential of +25% by end-2022, which is easily achievable considering its cheap valuation.

-

Given that the macro

outlook remains challenging while equities plagued by growth and structural

headwinds, we

temper our expectation for the market and downgrade our ratings for Singapore equities to 3.5 Star "Attractive".

Chart 1: Global trade weakness affected Singapore even before Covid-19

Chart 2: … Domestic demand also soft before the pandemic

Slumped into recession in 2Q 2020

Chart 3: Slump in exports dragged Singapore into a recession

Chart 4: Services industries hit severely this time

Long road to recovery back to pre-Covid levels

Chart 5: Dependency on exports means SG lacked the domestic demand to drive a recovery

Chart 6: Accommodation and food services, largest contributor to growth, contracted the most

Nascent signs of recovery but long journey ahead

Chart 7: Protracted recovery expected. GDP to rebound back to pre-Covid level in 2022

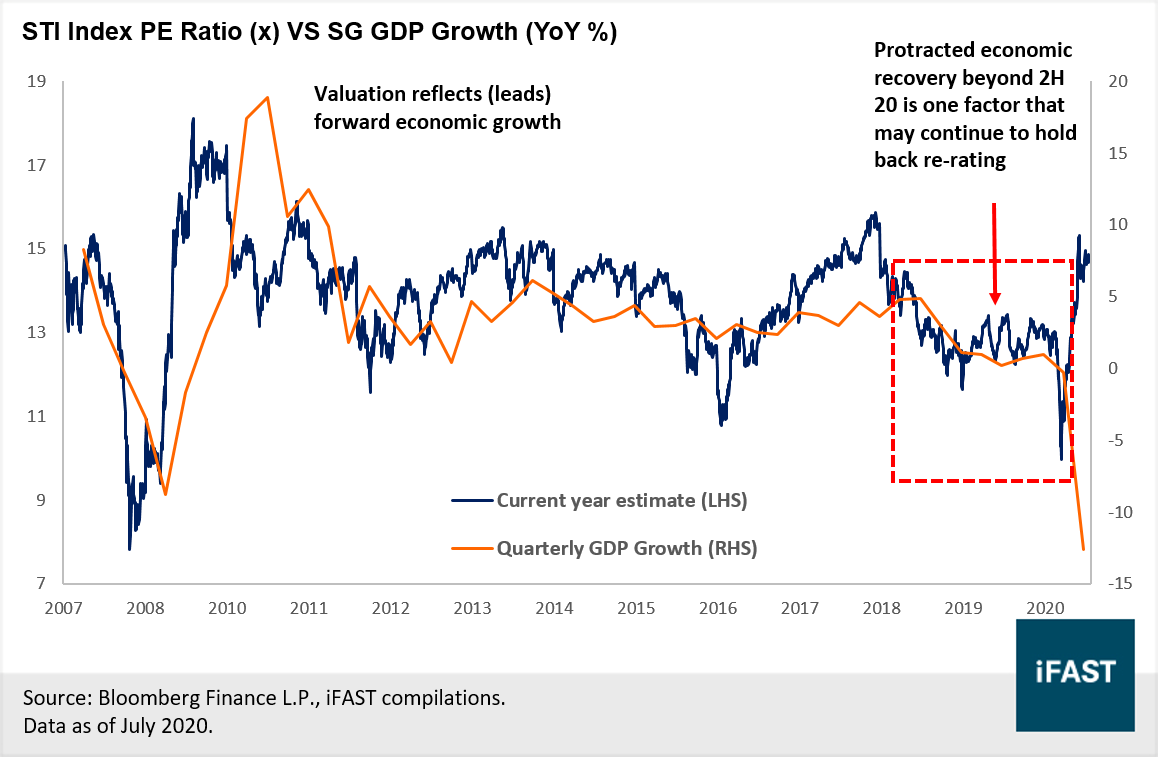

Valuation lacking catalysts to drive mean reversion

Chart 8: Valuation lacking catalysts to re-rate since mid ’18…

Chart 9: … Relationship is clear for forward Y+1 PE ratio

(i) Factors holding back re-rating - Mediocre economic growth expectation

Chart 10: Valuation reflective of forward economic growth

(ii) Factors holding back re-rating - Lacklustre earnings growth

Chart 11: Earnings and profit margin hit hard by the trade war after 2018

(iii) Factors holding back re-rating - Challenges facing constituent companies

Chart 12: Singapore equity market is heavily weighted towards Financials and Real Estate.

Challenging Backdrop ahead for the Financials sector

Chart 13: Falling interest rate environment in Singapore and Hong Kong due to accommodative monetary policies.

Chart 14: Singapore banks face steep decline in interest income due to the falling rates environment.

Outlook for Real Estate sector is not rosy either

Chart 15: While lower interest rates support the REITs performance, but outlook remains mixed among the REITs.

Attractive dividend yield is Singapore's silver lining

Chart 16: Singapore equities offer highest yield among all Asian markets

Chart 17: Dividend yields at an attractive level, even if they normalise to historical average.

Downgrade Singapore to 3.5 Stars ‘Attractive’

|

Singapore Equities |

FY 2020 |

FY 2021 |

FY 2022 |

|

PE Ratio (X) |

15.1 |

13.0 |

11.1 |

|

Expected Earnings Growth %YoY |

-30.0% |

16.0% |

16.0% |

|

Earnings Per Share |

171.2 |

198.6 |

230.4 |

|

Projected Fair Price |

2,397 |

2,780 |

3,225 |

|

Potential Upside from Today (%) |

- |

- |

+25% |

|

Source: Bloomberg Finance L.P., iFAST estimates. Data as of Jul 2020. |

|||

|

Equity Market |

Actively Managed Fund |

Passive tracking ETF |

|

Singapore |

SPDR Straits Times Index ETF |

Chart 18: While cheap, valuation of Singapore equities may remain depressed due to the lack of positive catalysts.

Chart 19: Investor remains compensated with a decent dividend yield while waiting for valuation and prices to recover upon a more optimistic outlook.

The Research Team is part of iFAST Financial Pte Ltd.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.