Note: This is an edited version of an article published earlier on our affiliates on 9 Apr 20.

Highlights:

- Evergrande experienced a decline in its earnings in 2019, as a result of the pressured profit margins from previous price cut. Concurrently, the group’s credit metrics also worsened.

- However, Evergrande has generated a strong cash collection amid the coronavirus pandemic, with improved liquidity especially after the recent refinancing. The Group claimed that it will officially enter the era of deleveraging and reduce its land bank, which serves as a positive signal for bondholders.

- Evergrande’s stocks and bonds have faced a heavy sell-off, resulting in some of their USD bonds now yielding over 20%. We think they are more attractive now and investors can consider the shorter term bonds.

Last September, we mentioned in “When the Yield Exceeds 12% — A Comprehensive Analysis on Evergrande” that the price of Evergrande’s bonds fell due to several reasons.

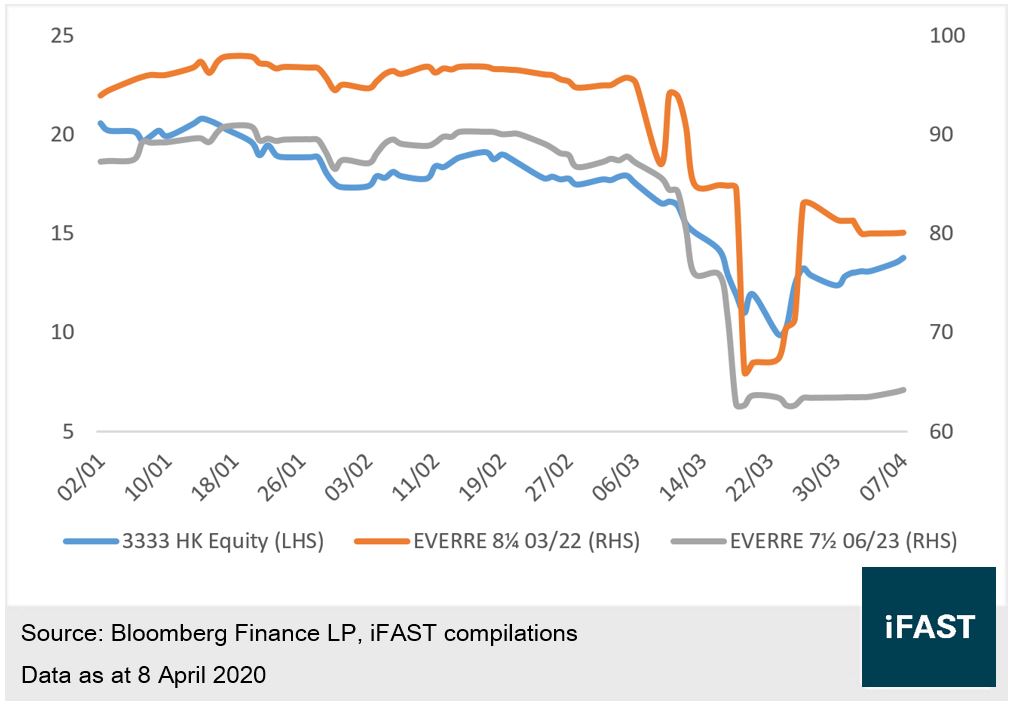

Recently, the collapse of global stock and bond markets have led to a sell-off of Evergrande's shares and bonds once again (see Chart 1). At its low, the stock price fell below the HKD 10 mark; some of the bond yields exceeded 20%, with the peak yielding more than 30%. This situation is similar to that in 2011.

Chart 1: Evergrande’s Stocks and Bonds Year-to-Date Performance

In this article, we analyze Evergrande’s recent situation and 2019 annual results.

Evergrande’s Latest Update

Decline in Earnings; Pressured Margins Due to Price Cut

As reported earlier last year, Evergrande’s results were disappointing for the first half of 2019. In the second half, although the annual revenue improved to RMB ¥250.6 billion (same currency below), both net profit attributable to shareholders and core business profit recorded a decline. The gross profit margin has even plunged to 22.2% (see Table 1).

Table 1: Evergrande’s 2019 Operating Performance

|

(in billion RMB) |

2019 Full Year |

YoY Change |

2019 2nd Half |

2019 1st Half |

|

Operating Revenue |

477.6 |

+2.4% |

250.6 |

227.0 |

|

Core Business Profit |

40.8 |

-47.9% |

10.4 |

30.4 |

|

Net Profit Attributable to Shareholders |

17.3 |

-53.8% |

2.4 |

14.9 |

|

Gross Profit Margin |

27.8% |

-8.4ppt |

22.2% |

34.0% |

|

Source: Annual Results, Interim Report, iFAST Compilations Data as at 31 Dec 2019 |

||||

While the Group's delivered floor area and revenue have increased in the second half, the overall profitability was not satisfactory given the sharp decline in profit margins. The Group has stated that the decline in gross margin was mainly attributable to the delivery and settlement of revenue of the lower-priced clearance stock properties.

We observed that Evergrande offered a considerable amount of discount promotions in recent years to generate cash inflow. Given that the group only delivers the properties and recognizes the revenue a few years after the sales, the financial impact of having provided discounts is now reflected on their profit margins through this income statement.

Nonetheless, we are not surprised by the decline in gross margin. After all, Evergrande holds the largest amount of land reserve in the industry and such promotions are commonplace. Instead, bond investors should be more concerned about the impact on the group's credit status.

Deteriorated Credit Metrics

As at end-2019, the Group's key credit indicators have all deteriorated compared to June (see Table 2). Evergrande's performance is comparatively disappointing as most of their rivals have seen their credit status improve.

Table 2: Evergrande’s Key Credit Indicators

|

December 2019 |

June 2019 |

|

|

Net Gearing Ratio |

181% |

176% |

|

Cash to Short Term Debt |

0.40x |

0.55x |

|

Average Borrowing Cost |

8.99% |

8.62% |

|

Net Debt / EBIT |

7.24x |

6.03x |

|

Source: Annual Results, Interim Report, iFAST Compilations Data as at 31 Dec 2019 |

||

Apart from the slight increase in the net gearing ratio, the average borrowing cost also rose to 8.99%, which is at a high level even compared to its single B rated peers. The continuous yearly increase reflects that the Group needs to offer even higher interest rates to attract lenders. In addition, the latest cash to short term debt ratio fell to 0.4x, reflecting that the Group's liquidity has further tightened.

Despite the poor numbers, Evergrande's sales in 2019 was a phenomenal ¥600 billion, dominating the whole industry and surpassing top rival Country Garden’s attributable contracted sales. As for other developers, their sales figures also proved no match for the industry-leader, Evergrande.

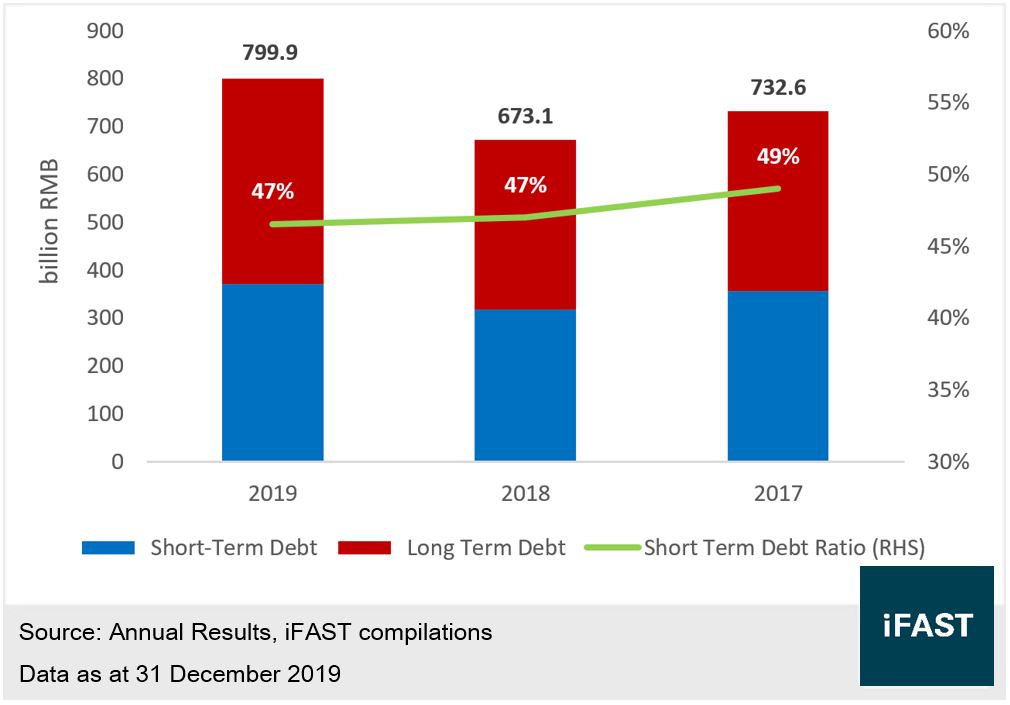

It is not the first year Evergrande has faced a huge amount of short term debt. In the past three years, its short term debt accounted for 47% to 49% of the total debt (see Chart 2). However, the Group has consistently overcome the debt pressure.

Chart 2: Evergrande’s Debt Distribution in Last 3 Years

Let's take a look at the group's cash flow and see if it offers enough capacity to repay the upcoming debts.

Evergrande’s Cash Flows

Sales and Cash Collection Remain Strong amid the Pandemic

As at December 2019, Evergrande had cash and cash equivalents of ¥150.1 billion (up 16.0% YoY) and restricted cash of ¥78.7 billion. Meanwhile, the Group's total debt was ¥799.9 billion (up 18.8% YoY); short term debt was ¥372.2 billion. We estimate that the cash interest expenses in 2020 will reach ¥70 billion.

Nevertheless, since the current assets included properties with a total value of ¥1.3 trillion under development and completed properties held for sale, the contracted liabilities-adjusted current ratio was a decent 1.44x.

So the question is, does Evergrande have the ability to convert these assets into cash flow?

Xia Haijun, the vice chairman and CEO of Evergrande, stated that this year's sales target was set at ¥650 billion, while the internal target stood at ¥800 billion.

While the targets may seem high, Evergrande achieved contracted sales of ¥44.7 billion and ¥62.1 billion in February and March respectively (up 107.8% and 13.1% YoY), despite the direct impact from the coronavirus outbreak. The high yearly growth is somehow attributable to the lower numbers last year, but Evergrande stands tall as the only first-tier developer that recorded a YoY increase of more than 20% in the first quarter of 2020.

With Evergrande's extremely high attributable ratio, we estimate that the sales in the first quarter alone will already generate about ¥100 billion cash inflow. The Group’s Chairman Xu Jiayin also pointed out that the actual cash collection within these three months was ¥113.3 billion. If Evergrande can achieve the ¥800 billion target, the cash collection will increase to ¥700 billion, which is sufficient to meet the current liabilities.

Evergrande has always positioned itself as a mid-end market provider for home buyers (as opposed to investment property owners). With land reserves scattered across the country, 67% of them are distributed in first- and second-tier cities, and only around 5% of sales located in Hubei Province, we think its overall sales performance will not be heavily affected by the pandemic.

Still, even though the pressure of the pandemic has recently been alleviated in China, we should not be over optimistic. As the overall sales volume in China declines, Evergrande must consider refinancing or reducing expenses in order to maintain cash flow.

Liquidity has Improved after Refinancing; Deleveraging Becomes the Key

The group managed to issue bonds just before the virus hit, providing it with some short term liquidity. In January, it issued a total of 5 bonds - 4 offshore and 1 onshore - worth a total amount of ¥46.5 billion, reducing the gap between total cash and short-term debt to less than ¥100 billion.

As we mentioned earlier, in order to alleviate its debt pressure, Evergrande can choose to extend the investment trusts repayment period at a higher cost. In addition, the agreement of refunding the ¥130 billion capital in the previous strategic investments should the Group fail to be listed as A-share, has been extended to the end of 2020. While Evergrande failed to meet profit targets and had to pay extra fees to the investors, it only had limited impact on the credit profile.

Therefore, we think Evergrande still has the financial flexibility to manoeuvre debt repayment. This includes a bond repurchase in the open market, which can reduce its principal and interest expenses. More importantly, the Group announced that it will focus on “high growth, scale control, debt reduction” as the key development strategy in the future, aiming to reduce total debt to less than ¥400 billion by the end of 2022. This would mean a reduction of the current debt amount by 50%.

Entering the Era of Shrinking Land Bank is a Positive Signal to Bondholders

Evergrande’s latest land reserves consists of a total construction area of 293 million square metres, with an extremely low average cost at ¥1,800/square metre.

Meanwhile, the Group's average selling price in 2019 was ¥10,281/square metre, which means the Group's average sales/land cost maintained an excellent level of 5.7x.

In 2019, Evergrande repeatedly engaged in a series of price reduction promotions, such as the limited time offer and marketing mix in September and October. Therefore, even if it continues to launch discount campaigns in the future (such as the 25% off offer during the pandemic), we expect that the total saleable resources for the Group will cross ¥2,000 billion, which is adequate to support the sales in the next four to five years.

Because of its large land bank, the Group has stated their decision to reduce the net land reserves by 30 million square metres per year. This would save ¥60 billion on land expenses annually and help the Group achieve deleveraging.

We believe that Evergrande’s determination to execute deleveraging may disappoint some stock investors looking for earnings growth. However, from the perspective of bond investors, reducing the debt size is definitely good news as it will help improve the Group’s long term debt servicing capacity.

Investing in Evergrande’s Bonds

Consider the Shorter-Term Bonds

With the coronavirus pandemic, we pointed out earlier in several articles that investors should pay more attention to issuers of BB grade or above which provide significantly increased yields, as they have better credit quality to withstand the economic shock.

However, as one of the B grade issuers, Evergrande has a considerable advantage in terms of scale over its peers, and we currently remain optimistic about its prospects. However, if its credit performance does not improve by June, we will re-evaluate the Group's outlook.

Due to its high market liquidity, Evergrande's bonds are more exposed to the selling pressure caused by panic sell-off. Therefore, attractive investment opportunities may appear more frequently.

Taking into consideration that the Group may fall into a vicious cycle of rising borrowing costs which will affect its long term debt servicing, we believe that bonds with shorter terms offer better investment opportunities, including the USD bonds due in 2022 or earlier (see Table 3). The current investment return of 15% to 22% (as at 8 Apr 2020) is highly attractive.

Table 3: Evergrande's USD Bonds due in 2022 or Earlier

|

Bond Name |

Years to Maturity |

YTM |

|

EVERRE 6.250% 28Jun2021 Corp (USD) |

1.22 |

14.96% |

|

EVERRE 8.250% 23Mar2022 Corp (USD) (Available on Bond Express) |

1.95 |

19.86% |

|

EVERRE 9.500% 11Apr2022 Corp (USD) |

2.00 |

21.69% |

|

Source: BSM Data as at 8 Apr 2020 |

||

Corporate Risks

Although we hold a positive view towards the Group’s outlook, the current credit status may lead to a possibility of credit downgrade and influence the bond price.

With the recent turmoil in the bond market, Evergrande's bonds, like many other bonds, will occasionally have inverted yields. Investors need to understand that this is a rational situation because it reflects the short term liquidity risk caused by the market’s concerns towards the pandemic, and we do not rule out the possibility of coronavirus cases rebounding in China.

Evergrande’s large amount of non-standard financing which is less transparent poses a higher level of difficulty and complications in analyzing the full debt structure of the Group.

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a principal position in EVERRE 8.250% 23Mar2022 Corp (USD) and EVERRE 7.500% 28Jun2023 Corp (USD). The analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.

Please note that only certain bond(s) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to FSM's prevailing policies and procedures. Please read our full disclaimers in the website.