The Ping An ecosystem business model

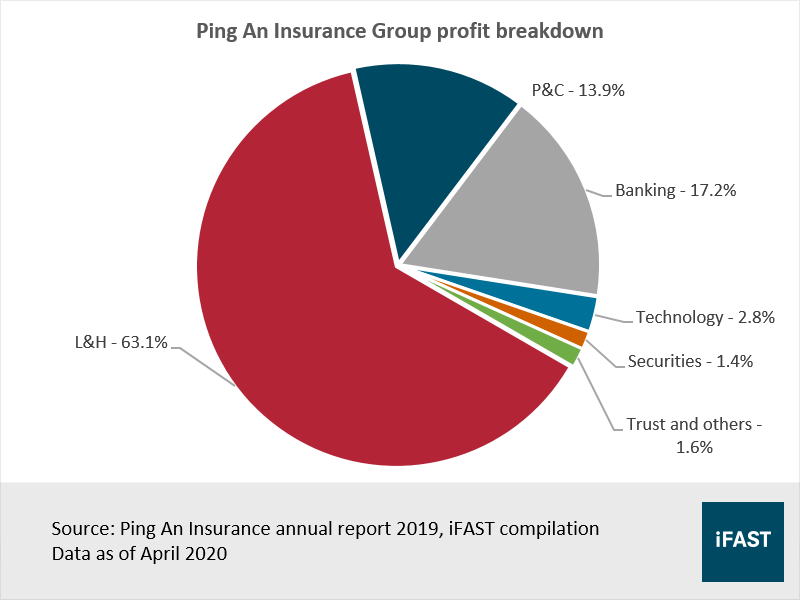

Chart 1: Breakdown of Ping An’s profit

Ecosystem strategy enables cross-selling opportunities

Table 1: A detailed explanation of Ping An’s “patient-provider-payer” ecosystem

| Description | |

| Patient | · Refers to users of the Ping An Good Doctor platform. · From the patient’s perspective, the platform is a one-stop portal to access extensive healthcare resources in a

cost-effective and convenient manner. |

| Providers | · Refers to doctors, hospitals, clinics, pharmacies, and retailers. · Increases the efficiency of medical

resources. · Providers can benefit from the high

volume of traffic from the platform. · Lowers customer acquisition costs for

providers. |

| Payers | · Refers to organisations that pay for the medical services – usually the

employer, insurance companies and the government. · Collaborate with insurance companies

to provide policyholders with value-added healthcare services that are complementary to the insurance products to reduce costs. · Using their technologies to help the

government reimburse and administer claims, increasing efficiency and reducing costs. · Collaborate with insurance companies

to provide policyholders with value-added healthcare services that are

complementary to the insurance products to reduce costs. |

Source:

Ping An Good Doctor’s prospectus, iFAST compilations Data as of April 2020 |

|

Chart 2: The healthcare ecosystem

Chart 3: Cross-selling efforts materialising

Technology has brought in many tangible benefits for Ping An

Chart 4: Ping An has the highest agent productivity amongst listed peers

COVID-19 outbreak to affect new business value growth, but a rebound is expected

Key investment risks

Once in a lifetime opportunity to scoop up Ping An Insurance at such cheap valuations

Table 2: SOTP valuation for Ping An Insurance

| Business segment | Shareholding | Valuation | Valuation methodology | Multiple | Weighted valuation |

| Life & Health | 99.5% | 334,487 | P/B | 3.0 | 1,008,207 |

| P&C | 99.5% | 93,539 | P/B | 2.0 | 182,433 |

| Banking | 58% | 252,277 | Market cap | 1.0 | 146,270 |

| Fintech & Health-tech | Disclosed | 192,458 | Disclosed Valuation | - | 192,458 |

| Securities | 97% | 30,431 | Peers P/B | 2.0 | 60,862 |

| Ping An Trust | 100% | 4,000 | Peers P/E | 15.0 | 60,000 |

| Others | 100% | 63,050 | Book value | 1.0 | 63,050 |

| Total | 1,713,280 | ||||

| # of shares | 18,280 | ||||

| End 2020 target price (RMB) | 93.7 | ||||

| End 2020 target price (HKD) | 105.0 | ||||

| Current share price (HKD) | 76.3 | ||||

| Upside potential | 37.7% | ||||

Source:

Bloomberg Finance L.P., Ping An annual reports, iFAST estimation Data as of April 2020 |

|||||

Table 3: Peer comparison

China Life |

Ping An Insurance |

China Pacific |

New China Life |

|

| Fundamentals | ||||

| FY2018 Gross written premiums (RMB billion) | 568.4 | 493.9 | 202.414 | 138.1 |

| Number of agents | 1.573 million | 1.286 million | 796,000 | 386,000 |

| Agent productivity (NBV per agent) | 29,770 | 48,789 | 28,988 | 31,689 |

| Valuations | ||||

| P/Embedded Value | 0.5 | 1.1 | 0.5 | 0.4 |

| P/B ratio | 1.1 | 1.6 | 1.1 | 0.9 |

| P/E ratio | 7.4 | 8.3 | 8.0 | 6.3 |

| Profitability | ||||

| Dividend yield | 4.1% | 3.4% | 5.9% | 4.6% |

| 2020E ROE | 15.1% | 20.9% | 13.1% | 13.0% |

Source: Bloomberg Financial L.P, iFAST estimations Data as of April 2020 |

||||

Chart 5: Ping An share price vs. EPS

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) hold a NIL position in the abovementioned securities. The analyst who produced this report has a position in Ping An Insurance.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.