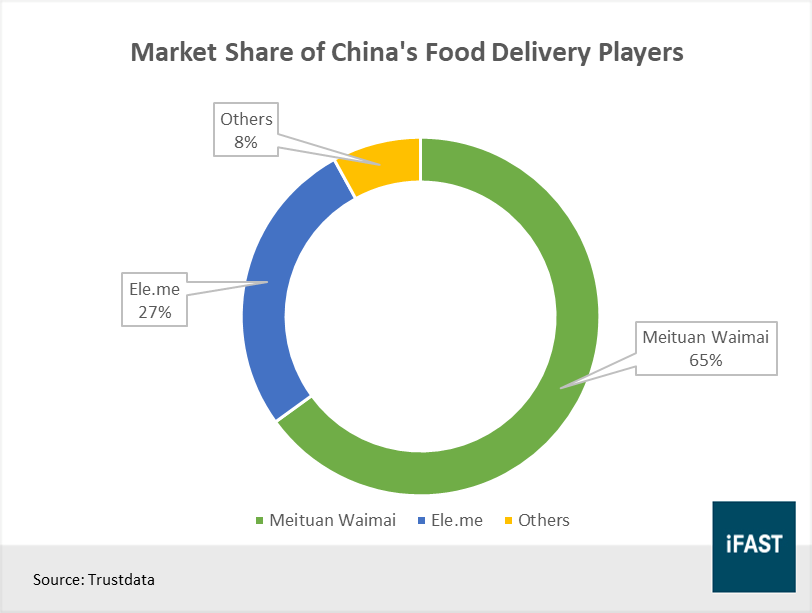

• Meituan Waimai is the food delivery arm of Meituan Dianping, the largest e-commerce platform for services in China. With a market share of 65%, Meituan is currently the leader in China’s food delivery industry.

• China’s food delivery industry is ripe for robust growth, led by the changing consumption habits and higher spending power of its people.

• As the company continues to increase its market share, it can potentially achieve higher revenues for its food delivery segment by raising its delivery order commission rate.

• The growing proportion of revenue contributed by online marketing services should continue to lift the overall margins for the food delivery segment.

• Despite the recent sell-off caused by the coronavirus outbreak, we remain positive on the long-term prospects of Meituan, and continue to maintain a target price of HKD 124 per share.

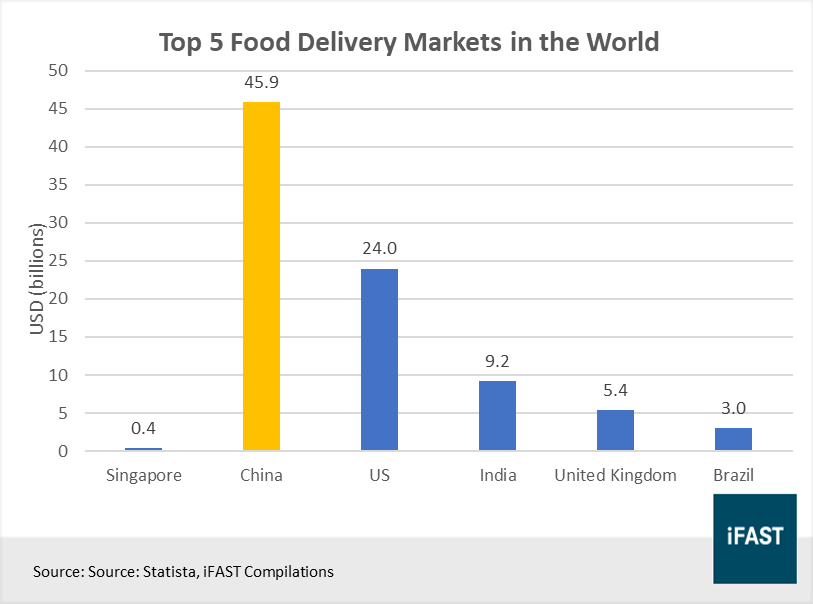

Figure 1: China is home to the largest food delivery market in the world

The rate at which China’s food delivery industry has grown relative to the US may come as a surprise to many, as the industry is still relatively young, having only taken off sometime in the middle of the last decade, driven by the fierce competition between two industry giants, Meituan Dianping (HKEX:3690) and Ele.me.

As a result of the aggressive expansion plans carried out by both companies, China’s food delivery industry today is essentially a duopoly between Meituan and Ele.me. In 2019, approximately 90% of the total industry revenue flowed to these two companies, with the lion’s share of 65% going to Meituan (Figure 2). Over the recent few years, Meituan has been steadily increasing its market share at the expense Ele.me.

Figure 2: Meituan Waimai is the undisputed leader in China’s food delivery industry

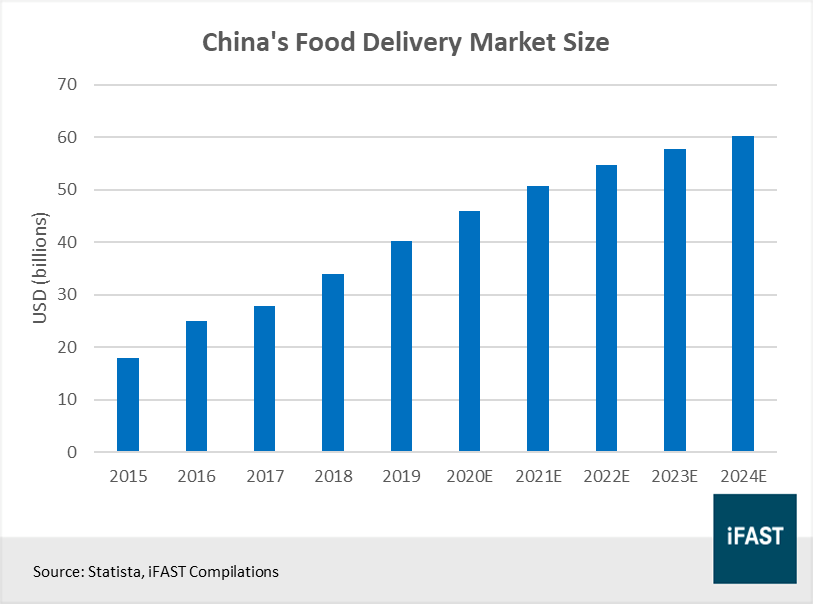

The good news for investors is that despite the explosive growth over the past few years, the boom in China’s food delivery industry is not showing any signs of slowing down yet. Revenue is expected to grow at a rate of close to 10% per year over the next 5 years, bringing the food delivery industry to a value of approximately USD 60 billion by 2024 (Figure 3).

Figure 3: China’s food delivery industry continues to grow strong

Changing consumption habits and rising incomes to drive growth in China’s food delivery industry

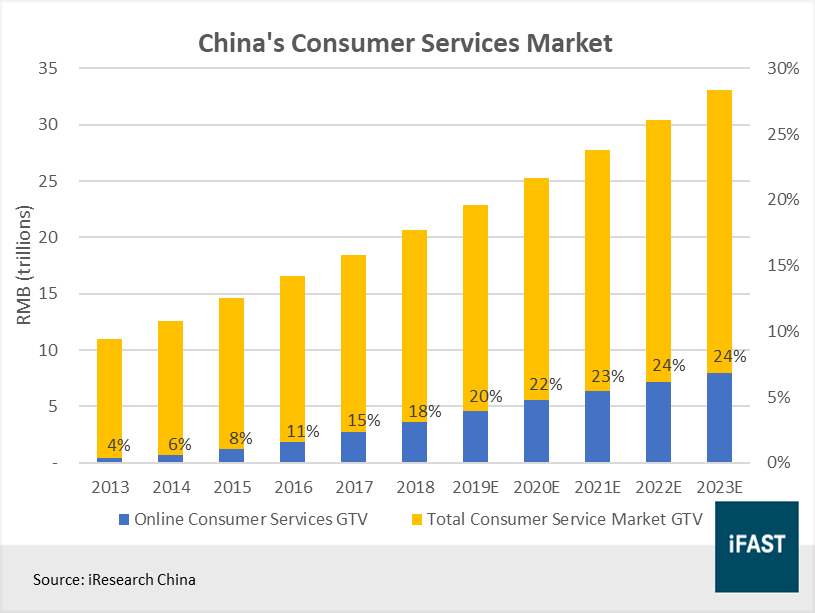

We believe that the future growth of China’s food delivery industry will come from two sources, the first of which is the changing consumption habits of the Chinese population. In stark contrast to the past, a greater proportion of services consumed in China today is captured in the digital space as consumers, especially those from the younger generation, are more willing to pay for the convenience of on-demand services, such as food delivery.

This has led to the steady rise in China’s online consumer services market, which grew from a mere 4% of the total consumer services market’s gross transaction value (GTV) to nearly 20% in a span of five years (Figure 4). Going forward, we expect online consumption to account for an even larger share of the total consumer services market, propelled by the growing pool of Internet users.

Figure 4: Growth in online consumption to rise on the back of more Internet users

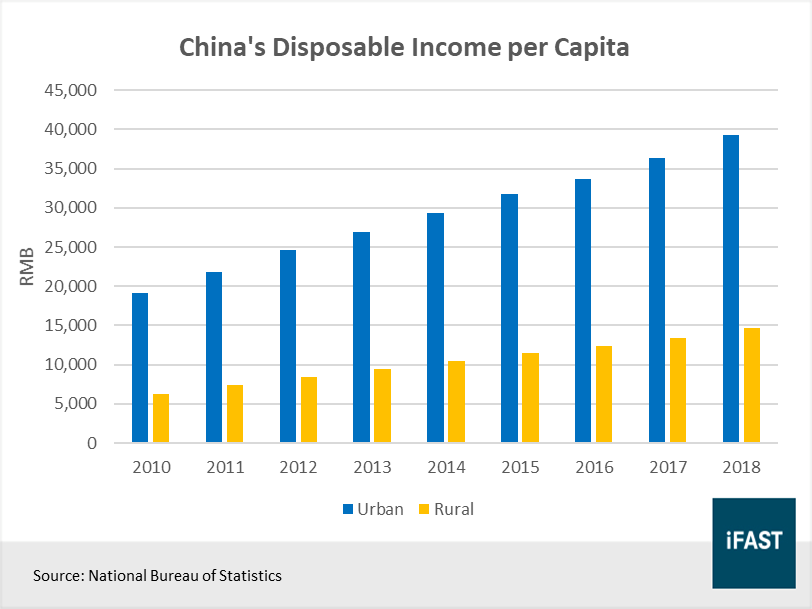

Secondly, China’s economy is becoming more consumption-driven. As the country continues on its journey towards becoming a developed market, its citizens are becoming wealthier as disposable incomes rise (Figure 5). Armed with higher disposable incomes, Chinese consumers are gradually shifting their spending from basic needs to more discretionary spending.

With greater spending power and more willingness to spend on discretionary items, China’s food delivery industry is ripe for robust growth. This is undoubtedly a huge positive for Meituan, thanks to its market leading position in China’s food delivery industry.

Figure 5: Chinese consumers today have greater spending power, courtesy of rising disposable incomes

Food delivery is Meituan’s bread and butter

Of the three business segments that Meituan has, food delivery is arguably the most important as it makes up nearly 60% of the group’s total revenue. Since the very beginning, Meituan has explicitly stated that it intends to adopt a “Food + Platform” strategy, under which it intends to focus the majority of its efforts on growing its food delivery segment.

Related Article: Meituan Dianping: The unicorn that might one day become China’s next ten-bagger

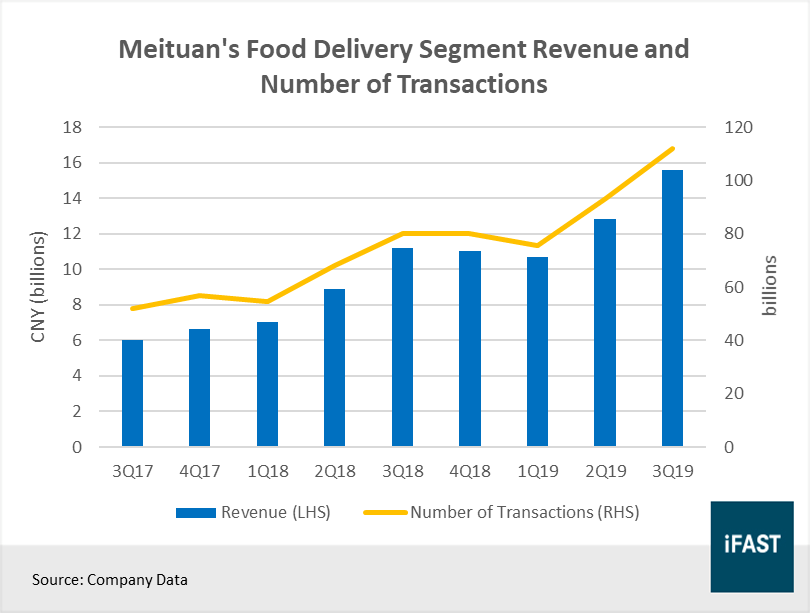

This strategy has proven to be successful, as the segment has experienced tremendous growth over the past few years. Food delivery revenue hit a record high of RMB 15.6 billion in 3Q19, up by a staggering 40% from the same period last year (Figure 6). The gains were driven by a sharp increase in the number of food delivery orders, from 1.8 billion to 2.5 billion, as well as an increase in the average order value.

Figure 6: Revenue and number of transactions has ballooned in the recent quarters

Meituan’s food delivery segment consists of three revenue streams - delivery services, platform services and online marketing services. As of June 2019, revenue generated from delivery services, in the form of commissions made up 92% of the total segment revenue.

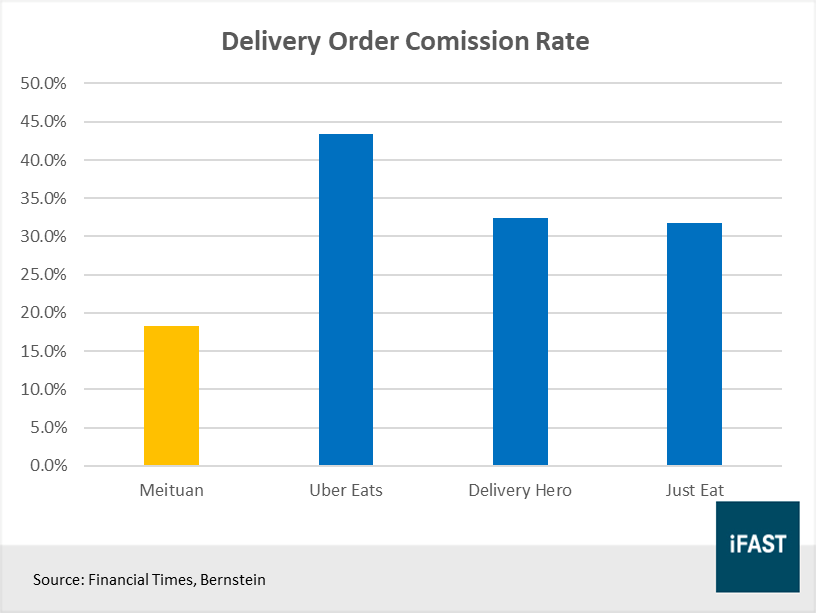

The good news for investors is that at this point in time, Meituan’s average delivery commission rate of approximately 18% is significantly lower than its global peers (Figure 7), which means that there is still plenty of room for commissions to grow. Moving forward, as competition between Meituan and Ele.me gradually winds down, with the former widely expected to control the majority of the market, we expect Meituan to have better pricing power, enabling the company to negotiate for better commission rates with merchants.

Figure 7: At just 18%, there is still plenty of room for Meituan’s delivery order commission rate to grow

However, the downside of a revenue model that is purely commission-based is that, at some point in the future, Meituan will not be able to raise prices without losing either customers or merchants. When this happens, earnings growth should naturally slow down assuming fixed costs (delivery fees) remain stable.

While the above scenario is unlikely to materialise in the near term, Meituan has already been preparing for it. To address this issue, the company has expanded its service offerings beyond delivery services, to include other services such as online marketing and other platform services, which tend to have higher margins compared to delivery services.

Over the years, Meituan has collected an enormous amount of user data, ranging from purchasing habits to food preferences and even favourite restaurants. Leveraging on this vast pool of information, Meituan has been able to develop innovative and unique online marketing campaigns for its merchants, increasing their exposure to potential customers. The successes of many of these marketing campaigns have led to a change in perception among merchants, as a large number of them now view Meituan as a consultant rather than just a platform to list their products.

These online marketing services are typically offered on a subscription basis, and include items such as display ads, marketing tools that enable merchants to dispense coupons to targeted customers, and other value-added services such as peer comparison and online storefront decorations. The addition of these services not only provides Meituan with another source of revenue, but they also serve to increase the stickiness of its platform for merchants.

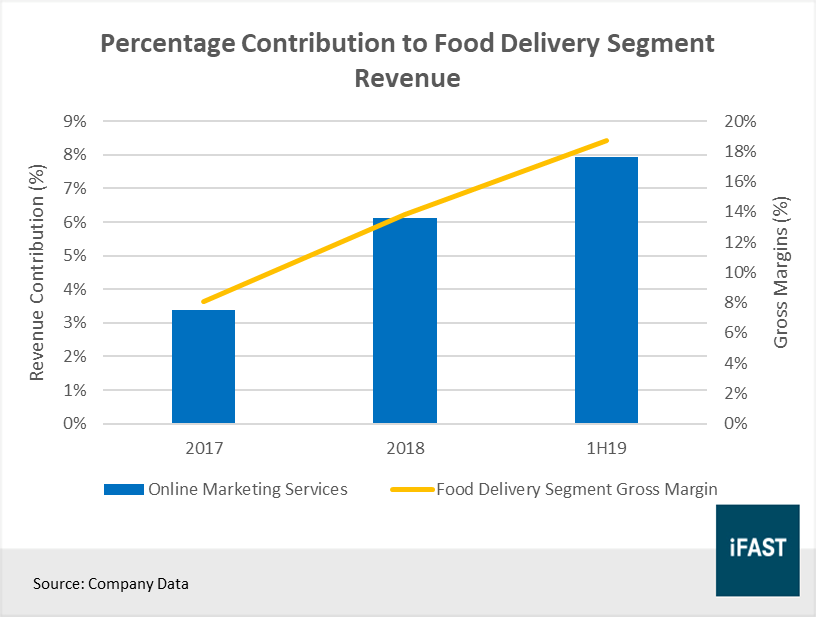

Figure 8: The proportion of revenue from online marketing services continues to grow each year

If Meituan continues to raise its commission rates, along with expanding its range of value-added services for merchants, we believe that the margins for Meituan’s food delivery segment will likely increase, placing the company on a path to greater profitability.

Recent sell-off presents an attractive buying opportunity

As of late, equity markets around the world have been pummelled by the outbreak of the coronavirus, which has already infected more than 60,000 and claimed the lives of over 1300 people across the globe. China, which makes up the vast majority of all the reported cases, has been severely affected as travel is halted and entire cities are placed on lock down.

Unsurprisingly, consumer discretionary stocks, such as those operating in the travel and retail industry are especially hard hit as the worsening situation in China has prompted many of its citizens to stay home, defer travel plans and cut back on discretionary spending. Meituan Dianping (HKEX:3690), which operates in this industry, has seen its share price decline by more than 15% since the news of the viral outbreak started to make waves on the market.

We recognise that in the short-term, Meituan is likely to see some negative impact to its earnings, and this could last for as long as it takes for the virus to be contained. However, if we set our sights further ahead, we do not believe that this event (as unfortunate as it is for the people who are affected) will derail our long-term investment thesis for Meituan, based primarily on the increasingly digitalised consumption habits of the Chinese population.

In addition, it is worth noting that Meituan has a much healthier balance sheet compared to its peers, which should come in handy when the company is faced with tough times such as the present. That being said, we continue to maintain our target price of HKD 124 for Meituan Dianping (HKEX:3690), after taking into consideration the long-term prospects of the company.

Table 1: Strong earnings growth expected for Meituan as margins continue to improve

|

2019E |

2020E |

2021E |

|

|

PE Ratio (X) |

317.95 |

76.35 |

35.80 |

|

Earnings Growth |

- |

316% |

127% |

|

EPS (CNY) |

0.29 |

1.19 |

2.54 |

|

Source: Bloomberg Finance L.P. |

|||

In our next article, we will explore the remaining two segments of Meituan Dianping, in-store hotel and travel and new initiatives.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.