' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

What is an Investment Linked Policy (ILP)?

An ILP is an insurance product that contains both insurance and investment elements. This is a product that is often marketed as a wealth accumulation product.

Do not confuse a participating product (E.g., Endowment or Annuity) for an ILP. The difference is that for participating products, returns of the insurer’s participating fund are given to the policyholder in the form of bonuses. Policyholder of such policies will not have the freedom to choose where their premiums are invested in but will get to enjoy a minimum level of guaranteed bonuses. The insurer may also apply smoothing of bonuses so that policyholders will be able to get a stable return.

On the other hand, ILPs give policyholders the flexibility to choose their own sub funds according to their own risk appetite.

How do you know if the product you are purchasing is an ILP?

Is ILP suitable for you?

1. Are you buying an ILP for protection?

There are cheaper options available in the market and ILP is definitely not a product that you should go for if your main focus is to get a product just for protection only.

2. Are you buying an insurance product for wealth accumulation?

You will have to consider these two questions:

If you are looking to save up a pre-determined amount of money within a fixed period of time, we would suggest an Endowment instead. Such product will provide you with stable returns and guaranteed elements. The last thing you would want is to purchase an ILP with a policy value that has fallen by the time your child requires educational funds.

Alternatively, there are also investment products such as T bills or Singapore Saving Bonds with potentially higher returns than endowments should you hold to maturity.

Buying an ILP is a long-term commitment with numerous fees and charges involved. Have you searched around for a comparable/alternative investment instrument that may provide similar returns yet at a lower cost?

You should check with your agent on all the underlying charges that are applicable to your policy, common charges of an ILP include (but are not limited to): Administrative charges, Premium Shortfall charges, Partial Withdrawal charges and Surrender charges. All these charges may potentially reduce the overall returns of your ILP.

3. Dissecting an ILP

If you look closely at an ILP, you will realize that your premiums are divided into investing into sub funds as well as going towards paying for mortality charges for your insurance protection. What if you can separate the insurance and investment components into two different products?

You can consider going for a term life insurance in which you can keep your insurance cost as low as possible yet at the same time achieve adequate coverage.

ILP is often marketed as a product for policyholders who do not want to actively monitor their investment portfolio. Policyholders of an ILP aim to achieve a good investment return over the long term through a “Dollar Cost Averaging” strategy. These sub funds that you choose to invest in are often managed by professional fund houses and are likely not your agent who sells you the policy.

If you would like to invest on your own, platforms like FSMOne allow you to set up recurring investment into professionally managed funds in which you will also be able to achieve a “Dollar Cost Averaging” strategy over the long term as well. However, do note that the available funds may not be identical to the one offered to you via an ILP.

Through this method of self-investing, you will also likely be able to avoid being tied down to a “Minimum Investment Period” associated with an ILP.

Understanding a product well before making your decision

The purpose of this article is to invoke a thought process for potential buyers of an ILP. This is to ensure that everyone can fully understand a product before deciding on a long-term commitment.

Due to the nature of an ILP being a combination of both insurance and investment, there is a possibility that one might end up not achieving both objectives.

Policyholders may not be able to maximise their investment opportunities during favourable market conditions. This is because the mortality charge increases every year as a policyholder grows older. Insurance cost of an ILP is often paid through your account value by deducting investment units of equivalent value. This means that more of your purchased units may be used to pay for the cost of insurance as you age. If the market were to turn unfavourable, even more units may have to be sold to cover for the increasing mortality charges due to your units being less valuable as compared to a favourable market condition.

Therefore, we would recommend to keep protection and investment separated.

Look for affordable products that focus just on protection

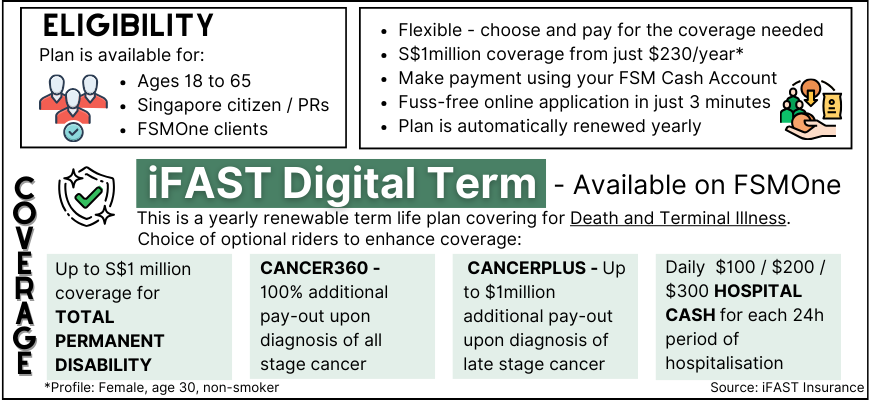

If you decide to focus on getting insurance products just for protection, you may want to consider iFAST Digital Term. Our product is designed to be simple and affordable so that clients will not need to spend a majority of their cash flow just for insurance. More information on our product can be found below:

Get covered with iFAST Digital Term

And enjoy up to 45% commission rebates!

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Manulife, NTUC Income, QBE, Sompo and Tokio Marine Life Insurance *Please check with our advisory team if the product you want is available on FSMOne Insurance |

You may also be interested in...

iFAST Digital Term – *NEW* on FSMOne

How is iFAST Digital Term different from the rest?

Are my Shield plans enough to cover me for cancer?

All You Need To Know About Hospital Insurance

Can I rely on my MediShield Life or Integrated Shield plan for Cancer Coverage?

Will the New Cancer Drug Change Affect Me?

Our Rebate Program – Save more when you insure with us

My agent recommended me a savings plan, should I buy it?

----

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product. This article is not a contract of insurance.

iFAST Digital Term and its riders are issued and underwritten by Raffles Health Insurance Pte Ltd and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to read the precise terms, conditions and exclusions specified in the policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

As buying a life insurance policy is a long term-commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid.

While iFAST and/or any of its third-party providers has/have tried to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")