' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

What is personal accident (PA) insurance?

Personal Accident (PA) plans offer financial protection against accidents and can be used to supplement existing life or health insurance plans. Coverage includes inpatient and outpatient medical treatments, hospitalisation expenses, as well as accidental death. Some PA plans may also include extra benefits such as a daily allowance during hospital stays, or a weekly income for those temporarily unable to work due to their injuries.

Who needs personal accident insurance?

Consider a personal accident plan if you fall into one of the following groups.

#1 You have young children

If you have a young one in childcare, you are likely familiar with the risk of Hand, Foot, and Mouth Disease (HFMD). This ailment is prevalent among toddlers and infants and is highly contagious, and transmittable.

While HFMD is not a severe medical condition, it may still take 7 to 10 days for a child to recover.1 Fortunately, PA plans cover infectious diseases like HFMD, which may offer parents a peace of mind. This will allow them to make a claim for their child's treatment expenses, which may include hospital stays and outpatient treatments that may not covered by MediShield Life.

Personal Accident plans with Hand Foot Mouth Disease (HFMD) benefit:

Allianz Accident Protect Plus |

FWD PA |

Great Eastern PA Supreme |

Income PA Assurance |

MSIG Protection Plus |

Singlife Accident Guard |

Sompo PA Star |

Sompo PA Ease |

|

Exclusive 35% off with promo code "ifast$35%". Valid until 31 July 2024. |

|

|

||||||

Cover for HFMD |

Yes |

Yes |

No |

Yes (Optional cover) |

No |

Yes |

Yes |

Yes |

#2 You actively engage in sports or outdoor activities

Did you know that 28% of sports injuries are from a fall, and one fifth of sport injuries result in fractures?3 Engaging in sports and outdoor activities can lead to injuries like sprains, strains, or fractures. In the event that you suffer an injury, you may only be able to partially claim your medical expenses from your Shield plans if you are hospitalised. In the event that you are not hospitalised for your injuries, you will not be able to claim from your Shield plan for your outpatient medical expenses.

Personal accident insurance however, can protect against this with PA plans typically including benefits such as coverage for physiotherapy, chiropractic treatment, and Traditional Chinese Medicine (TCM) treatments. You may also receive daily hospitalisation allowance in the unfortunate event that you need to be hospitalised due to your accidental injury.

#3 You live near a dengue cluster

Did you know that we are currently experiencing peak dengue season? With weekly cases quadrupling in the last three months, Singapore is in the midst of a dengue outbreak and dengue cases is expected to continue increasing in July and August.2 If you are living near a dengue cluster, you could be at risk of getting dengue.

While most dengue cases are usually mild, severe cases may require hospitalisation. Having a personal accident plan with dengue cover can help to mitigate the financial costs by offering a medical expense or hospitalisation benefit in the event that you have dengue fever and require medical treatment.

Note that coverage offered for dengue in personal accident plans will vary across the different insurers and plans.

Personal Accident plans with Dengue Fever coverage:

Allianz Accident Protect Plus |

FWD PA |

Great Eastern PA Supreme |

Income PA Assurance |

MSIG Protection Plus |

Singlife Accident Guard |

Sompo PA Star |

Sompo PA Ease |

|

Exclusive 35% off with promo code "ifast$35%". Valid until 31 July 2024. |

|

|

||||||

Cover for Dengue fever |

Yes |

Yes |

No |

Yes (Optional cover) |

No |

Yes |

Yes |

Yes |

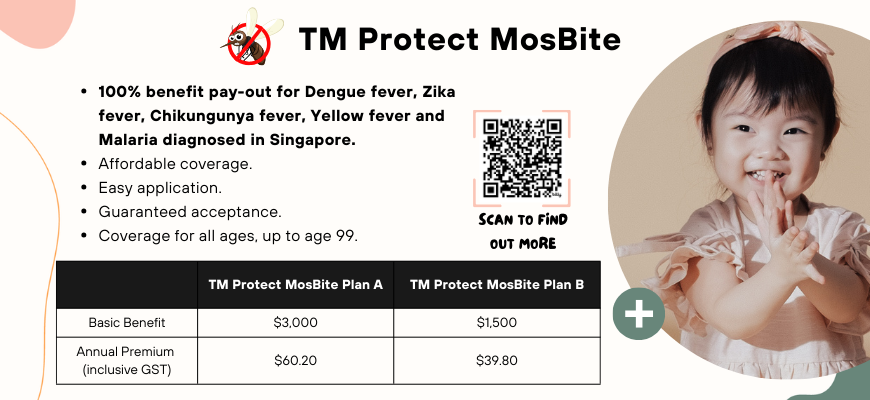

If you're in the market for a standalone plan that offers cost-effective coverage from as low as $39.80 annually (which breaks down to just $3.31 monthly), you might want to look into TM Protect Mosbite.

Tip: [Only in July’24!] Don’t miss 3.5% cashback on insurance premium when you use FSMOne Debit Card to pay for the premium.

#4 You are prone to accidents or falls

Having personal accident insurance can be beneficial for this group of individuals as a PA plan can complement existing shield plans to offer more comprehensive coverage in the unfortunate event of an accidental injury.

An Illustration:

Mr Tan suffered an unexpected leg fracture and was taken to the hospital in an ambulance and admitted for further checks. He learnt that he would be required to stay at a hospital for eight days, and was given 11 weeks of medical leave to recover.

Coverage |

Claimable with Integrated Shield plan from Insurer A? |

Claimable with Personal Accident plan from Insurer A? |

Ambualnce fee |

No |

Yes |

Hospitalisation and treatment at Private Hospital |

Yes, subject to co-payment and deductibles |

Yes, for balance not claimable under Integrated Shield plan |

Daily Hospital Income |

No |

Yes |

Weekly Cash |

No |

Yes |

As shown in the table above, a personal accident plan would allow Mr Tan to make a claim for his ambulance fee, daily hospital income, and weekly cash – these are benefits that are excluded from a shield plan. Additionally, he may also use his PA plan to claim the balance co-payment or deductible amount that is not claimable under a shield plan.

#5 You are unable to get traditional life or hospital insurance

Individuals who find themselves unable to purchase traditional life or hospitalisation insurance due to a pre-existing medical condition may wish to consider personal accident plans. Unlike life insurance which may not cover those with existing health issues, personal accident plans do not require individuals to undergo medical underwriting to purchase. This allows individuals with pre-existing conditions to still be able to obtain some form of coverage.

Personal accident insurance is suitable for:

Personal accident insurance is not suitable for:

Save more when you insure with FSMOne

Enjoy up to 45% commission rebates when you apply through us

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

You may also be interested in...

Top questions about CareShield Life and its supplements, Answered!

Is Attaining the Enhanced Retirement Sum by 55 a Myth?

What you need to know about the cost of cancer treatments and cancer plans

Your TPD cover is not a disability insurance. Here’s why

Are you over-insured or simply overspending on your insurance?

Information obtained from:

1Source: https://www.nuhs.edu.sg/For-Patients-Visitors/find-a-condition/Pages/Hand-Foot-and-Mouth-Disease-Children.aspx

2Source: https://www.ncid.sg/Health-Professionals/Articles/Pages/Rise-in-dengue-cases-underscores-need-for-constant-vigilance.aspx

3Source: https://www.mountelizabeth.com.sg/health-plus/article/sports-injuries-by-the-numbers#content

Information retrieved on 24 June 2024.

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product.

This article is not a contract of insurance.

All materials and contents found in this article does not have any regard to the specific financial objectives, financial situation and particular needs of any specific person. You are advised to read the precise terms, conditions and exclusions specified in the relevant policy contract and consider carefully whether the product in question is suitable. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to read the precise terms, conditions and exclusions specified in the relevant policy contract.

This comparison does not include information on all similar products. iFAST does not guarantee that all aspects of the products have been illustrated. You may wish to conduct your own comparison for products that are listed in www.comparefirst.sg

While iFAST and/or any of its third-party providers has/have tried to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice. This advertisement has not been reviewed by the Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")