' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

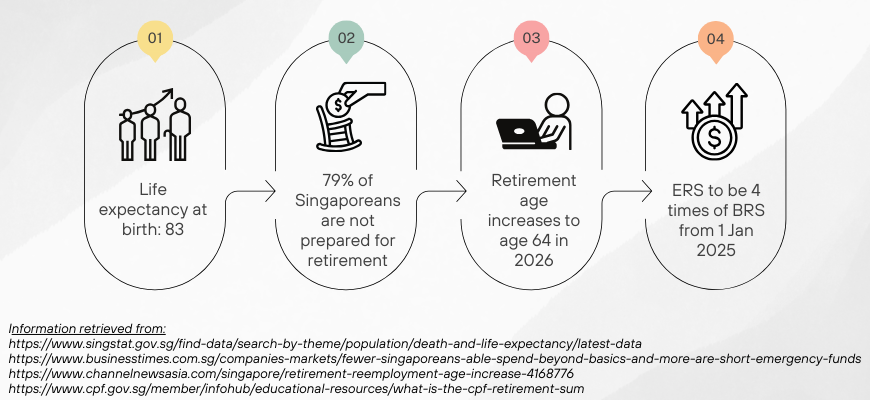

Did you know that there is an increasing number of Singaporeans who are not well-prepared for their retirement? According to a study done by a local bank, 79 per cent of Singaporeans either do not have a retirement plan or are not on track with their retirement plans.1 With Budget 2024 announcing the changes to our CPF Special Account and Enhanced Retirement Sum (ERS), here are our thoughts on how this will affect our generation’s plans for retirement.

#1 Closure of CPF Special Account (SA)

Current: CPF Shielding refers to the practice where individuals invest their SA monies a few months before they turn 55 to avoid their SA monies from going into their CPF Retirement Account (RA). Once the RA has been opened on their 55th birthday, individuals will then liquidate their investments which will return to their SA and allow them to maximise the higher interest rates of the SA while enjoying the withdrawal flexibility.

The changes: From early 2025, CPF SA will automatically be closed for those aged 55 and above. CPF SA savings will be transferred to your RA up to the Full Retirement Sum (FRS), which is two times the Basic Retirement Sum (BRS). The remaining monies in your CPF SA will be transferred to your CPF Ordinary Account (OA) and remain withdrawable.2

How this affects us: CPF Shielding was previously promoted as a “CPF hack” to help individuals with their retirement planning. However, the changes to CPF SA have made the practice of CPF Shielding no longer viable. Individuals will now have to look for alternative solutions for their retirement planning.

#2 Increased Enhanced Retirement Sum (ERS)

Understanding the retirement sums: BRS, FRS, ERS3

Current: ERS is pegged to three (3) times of your BRS.

The change: From 1 January 2025, ERS will be increased to four (4) times of your BRS.

How this affects us: Savings in the RA will go towards paying for CPF Life premiums. As CPF Life monthly pay-outs are first paid from your CPF Life premium5, a higher ERS limit will mean that individuals can accumulate more in their RA for higher pay-outs. However, while a higher ERS allows us to utilise CPF Life for higher monthly pay-outs, will the ERS still be an attainable amount when it is our turn to retire?

Approximately how much will my Retirement Sum be in future?

Year |

Inflation rate |

Basic Retirement Sum (BRS) |

Full Retirement Sum (FRS) |

Enhanced Retirement Sum (ERS) |

2024 |

3.5% |

$102,900 |

$205,800 |

*$308,700 |

2029 |

3.5% |

$122,227 |

$244,454 |

$488,907 |

2034 |

3.5% |

$145,167 |

$290,334 |

$580,668 |

2039 |

3.5% |

$172,413 |

$344,826 |

$689,652 |

*2024’s ERS is still pegged to 3 times of BRS. New ERS requirement will take effect from 2025 onwards.

Assuming an inflation rate of 3.5% according to MAS Core Inflation projection6, we can expect our BRS to be approximately $172,413 in 15 years’ time. If ERS remains pegged to 4 times the BRS, we would need to have over $600,000 in our CPF RA to fulfil the ERS criteria in 2039.

Will my CPF savings be enough for the Retirement Sum?

Projected CPF savings assuming monies compound annually at 2.5% interest rate, with a monthly contribution of $1,000 to your CPF account. Projection assumes CPF account starts with $0 savings.

Year |

Interest rate |

Annual contribution |

Your CPF account savings |

Basic Retirement Sum (BRS) |

Full Retirement Sum (FRS) |

Enhanced Retirement Sum (ERS) |

2024 |

2.5% |

$12,000 |

$0 |

$102,900 |

$205,800 |

*$308,700 |

2029 |

2.5% |

$12,000 |

$63,076 |

$122,227 |

$244,454 |

$488,907 |

2034 |

2.5% |

$12,000 |

$134,441 |

$145,167 |

$290,334 |

$580,668 |

2039 |

2.5% |

$12,000 |

$215,183 |

$172,413 |

$344,826 |

$689,652 |

Based on the above assumptions, an individual can expect to have over $200,000 in his/her CPF account savings in 15 years’ time. While this allows the individual to fulfil the projected BRS amount, he/she would not be able to fulfil the projected ERS for higher pay-outs.

According to the CPF website, the monthly pay-out from BRS for an individual who turns 55 in 2024 is estimated to be $840 to $9007. Based on a 2019 study, a single man or woman aged 65 and above would need at least $1,379 a month in retirement to sustain a basic standard of living.8 Adjusting for inflation at 3.5% per annum, you would need to have $1,637 in 2024 for your basic retirement needs. This means that your monthly pay-outs from CPF Life may be insufficient for your retirement.

If you foresee your retirement expenses to be higher than this amount, you may wish to start considering other retirement options now.

How else can I plan for my retirement?

With these changes to your CPF SA, and the potentially inadequate CPF Life pay-outs, you may wish to consider alternative options such as annuities to help with your retirement planning.

#1 Annuities for a regular stream of income

A type of life insurance, annuities can provide you with a regular and guaranteed income for life or for a specified period of time. Premiums are made for a specified period of time and pay-outs will commence upon reaching your desired retirement age. This provides you financial security in retirement knowing that you will never run out of money or outlive your savings in retirement.

#2 Annuity pay-outs are not subjected to market volatility

Market volatility can increase or decrease the value of your assets, leading to uncertainty in the future worth. As assets are subjected to market volatility, the current value of $1 million could change significantly over the next decade. Annuities, on the other hand, offer pay-outs comprising of guaranteed and non-guaranteed components. The guaranteed component in annuities offers income certainty and will not be subjected to market volatility.

Annuities available on FSMOne:

Enrich Income |

Enrich Retirement |

Gro Retire Flex Pro |

Retire Ready Plus (III) |

Singlife Flexi Retirement II |

|

Insurer |

Etiqa |

Etiqa |

Income |

Manulife |

Singlife |

Premium payment term |

3, 5, 10, 15, 20 years |

2, 5, 10 years |

Single, 5, 10, 15, 20, 25, 30, 35, 40 years |

Single, 5, 10, 15, 20 years |

Single, 5, 10, 15, 20, 25 years |

Frequency of pay-outs |

Monthly |

Monthly |

Monthly |

Monthly |

Monthly |

Pay-out period |

Up to age 125, starting from as early as 37th policy month |

10 or 20 years |

10 or 20 years or up to age 100. Pay-outs starts after a accumulation period |

5, 10, 15, 20 years or lifetime |

From 5 years up to age 120 |

Annuities are suitable for:

Annuities are not suitable for:

Save more when you insure with FSMOne

Enjoy up to 45% commission rebates when you apply through us

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Information obtained from:

1Source: https://www.businesstimes.com.sg/companies-markets/fewer-singaporeans-able-spend-beyond-basics-and-more-are-short-emergency-funds

2Source: https://www.cpf.gov.sg/member/faq/retirement-income/general-information-on-retirement/i-am-aged-55-and-above--what-will-happen-when-my-special-account

3Source: https://www.cpf.gov.sg/member/infohub/educational-resources/what-is-the-cpf-retirement-sum#:~:text=The%20Basic%20Retirement%20Sum%20(BRS,much%20one%20needs%20in%20retirement

4Source: https://www.cpf.gov.sg/member/retirement-income/retirement-withdrawals/withdrawing-for-immediate-retirement-needs/withdrawal-of-cpf-savings-for-property-owners

5Source: https://www.cpf.gov.sg/member/faq/retirement-income/monthly-payouts/how-does-the-cpf-life-standard-plan-work-#:~:text=Your%20CPF%20LIFE%20monthly%20payouts,matter%20how%20long%20you%20live.

6Source: https://www.mas.gov.sg/news/monetary-policy-statements/2024/mas-monetary-policy-statement-29jan24#:~:text=9.,from%20the%20October%202023%20MPS.

7Source: https://www.cpf.gov.sg/member/infohub/educational-resources/what-is-the-cpf-retirement-sum#:~:text=The%20Basic%20Retirement%20Sum%20(BRS,much%20one%20needs%20in%20retirement.

8Source: https://www.straitstimes.com/singapore/study-finds-1379-a-month-needed-to-meet-basic-living-standard-for-single-elderly

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product.

This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to read the precise terms, conditions and exclusions specified in the relevant policy contract.

This comparison does not include information on all similar products. iFAST does not guarantee that all aspects of the products have been illustrated. You may wish to conduct your own comparison for products that are listed in www.comparefirst.sg

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

As buying a life insurance policy is a long term-commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid.

While iFAST and/or any of its third-party providers has/have tried to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice. This advertisement has not been reviewed by Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")