' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

In our recent video, iFAST Global Wealth and Fintech Services’ Managing Director (Mr Lim Wee Kiong) interviewed MoneyOwl’s Chief Executive Officer (Ms Chuin Ting Weber) to discuss recent developments with regards to the MAS consultation paper, as well as the MAS and MoneySense Basic Financial Planning Guide. In the video, Ms Weber shared that while many believe that they are over-insured, they are actually overspending on their insurance. In this article, we highlight the differences between the two and share tips on how to avoid overspending on your insurance.

Full video of the interview can be found here:

Over-insured vs Overspending

Over-insured refers to the act of having more coverage than necessary. This means your insurance policies could overlap in terms of coverage, or you may be paying for policies and/or coverage that you do not need.

Overspending refers to getting covered at a higher cost than needed. This could either mean spending a significant portion of your income on your insurance premiums or purchasing expensive policies that offers more than the basic necessary coverage.

To avoid overspending on your insurance

Step 1: Determine how much coverage you need

When purchasing insurance, it is important to first determine how much insurance coverage you need. As a general rule of thumb, the Monetary Authority of Singapore (MAS) and MoneySense Basic Financial Planning Guide1 recommends you to have insurance protection for:

MAS and MoneySense Basic Financial Planning Guide: The Basic Financial Planning Guide is an initiative launched by the Monetary Authority of Singapore (MAS) and MoneySense, together with the Association of Banks in Singapore (ABS), Association of Financial Advisers (Singapore) (AFAS) and Life Insurance Association (LIA) to help Singaporeans with their finances. This guide outlines several rules of thumb to help Singaporeans plan for their savings, insurance, and investment needs. |

While this is not a hard or fast rule to have, you may take reference from this guide to check if you have adequate insurance coverage. Once you have determined how much coverage you need, you may then proceed to check if you are overspending on your insurance.

Step 2: Calculating your insurance expenses

After determining your necessary insurance coverage, the next step would be to ensure that you are paying as “little” as you can for your protection needs. One way to do this is to avoid “bundled products” (i.e. investment-linked policies, endowments, whole life insurance), and instead opt for pure protection products such as term insurance.

In the table below we compare using a term life plan for death coverage as compared to using a whole life or endowment plan. While using a term life plan for $500,000 death coverage will cost the insured $1,410, using a whole life or endowment to do the same would result in much higher premiums. This is because term life insurance is a pure protection product whereas whole life and endowment plans are products that are used for more than just protection needs.

Term Life Plan A |

Whole Life Plan B |

Endowment Plan C |

|

Death coverage |

$500,000 |

$500,000 |

$500,000 |

Coverage period |

Covers up to age 99 |

Covers up to age 99 |

Covers up to age 99 |

Premium payment period |

68 years |

69 years |

25 years |

Annual premiums* |

$1,410 |

$6,604 |

$9,974 |

*Profile: Age 30 non-smoker female (birthdate: 01/01/1994). Information is accurate as of 23 April 2024. Premiums are rounded down to the nearest whole number.

As insurance is an expense you do not want a return on, you should not be looking to profit from getting insured. Instead, check that the amount you are spending on your insurance is not more than 15% of your take-home pay, and that you can comfortably pay for the insurance premiums required. This will help you to gauge if you are overspending on your protection needs.

Introducing our solution for simple low-cost term life insurance: iFAST Digital Term

We acknowledge the difficulties of understanding what you are getting insured for and that some may be wary about meeting agents for insurance coverage. However, we feel that insurance is a necessity as having adequate coverage will help you and your loved ones to safeguard your financial future. This is why we designed an online solution that is simple and easy to understand. iFAST Digital Term is underwritten by Raffles Health Insurance (RHI), and purchases can be made just by answering a few questions. DIY your coverage and get insured from the comfort of your own home.

iFAST Digital Term: Benefits and features

We intentionally kept iFAST Digital Term simple, offering coverage for what we think is essential – death and terminal illness (TI). This allows you the flexibility to only choose to opt for coverage or features that you need.

We designed our product with affordability in mind, ensuring that premiums remain accessible for all by focusing on only giving you the coverage that you need. Get $1 million coverage from just $230 a year*, and enjoy additional savings with our Insurance Rebate Program offering up to 45% commission rebates!

If you are in the pink of health, there is no need to undergo a health check-up to buy this plan. Apply online anywhere, at any time, and for any amount that you wish to purchase.

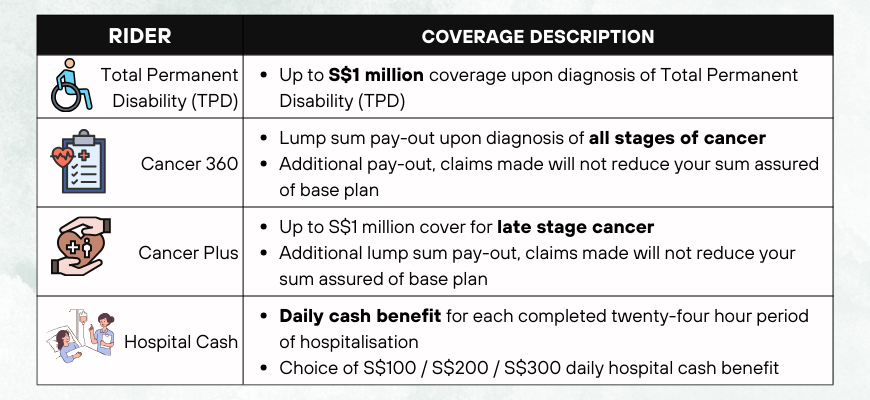

We have 4 riders available for add-on should you wish to enhance your coverage.

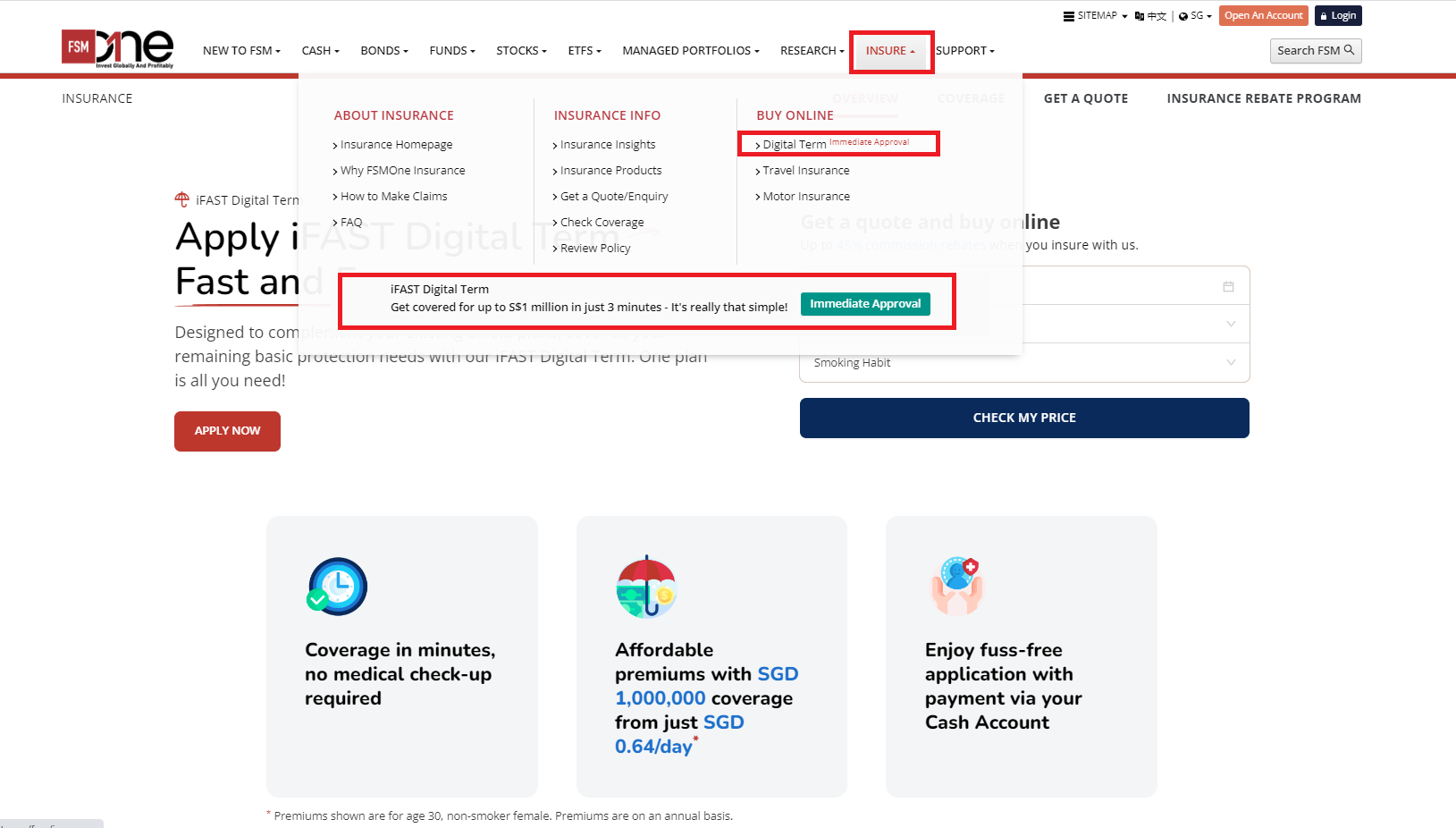

Purchase iFAST Digital Term in 4 simple steps

To get a quote, go to "Insure" > "Buy Online" > "Digital Term", or click here to go to the iFAST Digital Term landing page.

You can get covered in just 4 steps! All you have to do is:

Step 1: Just fill in a few simple details or log into your FSMOne account to have these details pre-filled for you.

Step 2: Select your coverage amount and choose to add-on riders (optional).

Step 3: Answer 3 simple health declaration questions.

Step 4: Login, review your application, and make payment with your Cash Account.

Upon a successful purchase, you may also view your policy details under Account Summary > Protection > View Policy Detail.

Save more when you insure with FSMOne

Enjoy up to 45% commission rebates when you apply through us

Or, reach out to us for a second opinion on your insurance policy or a complimentary review

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

You may also be interested in...

[PROMOTION] Enjoy UPSIZED REWARDS when you refer your friend to join and insure with us

Our Rebate Program – Save more when you insure with us

What you need to know about the cost of cancer treatments and cancer plans

Best Travel Insurance plans in Singapore

Top questions about CareShield Life and its supplements, Answered!

Information obtained from:

1https://www.mas.gov.sg/news/media-releases/2023/mas-and-financial-industry-launch-basic-financial-planning-guide

Disclaimer:

*Profile: Age 30 (birthdate: 01/01/1994), non-smoker female.

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product.

This article is not a contract of insurance.

iFAST Digital Term and its riders are issued and underwritten by Raffles Health Insurance Pte Ltd and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to read the precise terms, conditions and exclusions specified in the policy contract.

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

As buying a life insurance policy is a long term-commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid.

While iFAST and/or any of its third-party providers has/have tried to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice.

More information on iFAST Digital Term can be found here.

This advertisement has not been reviewed by Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")