' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

- As Japan gradually moves away from decades of deflation and stagnant growth, the positive impact of economic normalisation cannot be understated.

- A stronger yen doesn’t necessarily mean lower earnings for Japanese companies. There are quality Japanese companies that are less dependent on the tailwind of a weaken yen due to their global competitiveness and focus on megatrends.

- Japan's compelling long-term growth story remains strong, driven by its commitment to enhancing shareholder value and its potential to re-emerge as a dominant force in the global semiconductor industry.

- The dip in share prices from the July peak has enhanced Japan’s risk-reward profile, presenting a compelling opportunity for investors to increase their positions.

- We maintain a target price of 48,000 for the Nikkei 225, implying an upside potential of 35% as at 11 September 2024.

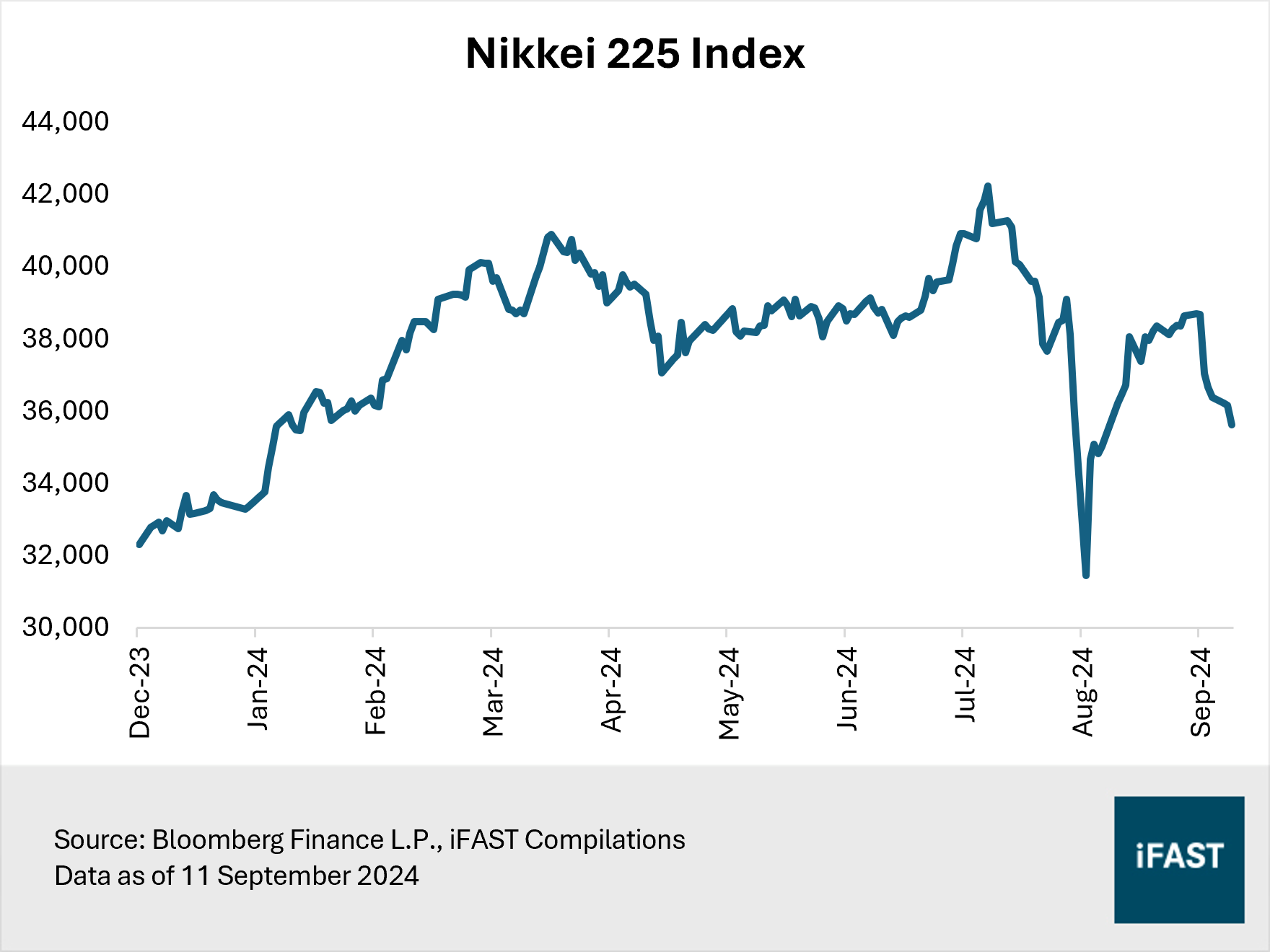

In August 2024, the Nikkei 225 Index experienced its widest monthly trading range since the property market bubble burst in 1990. This heightened market volatility came following the Bank of Japan’s (BOJ) second rate hike in 17 years which triggered a rapid surge of the yen and an unwinding of yen carry trades. However, the volatility has partially subsided as market focus shifted back to Japan’s resilient economic and corporate fundamentals.

In our article from early August 2024, we recommended investors to buy the dip in Japan. Today, we stand by our recommendation to seize the opportunities and continue to advocate for Japan’s compelling investment case.

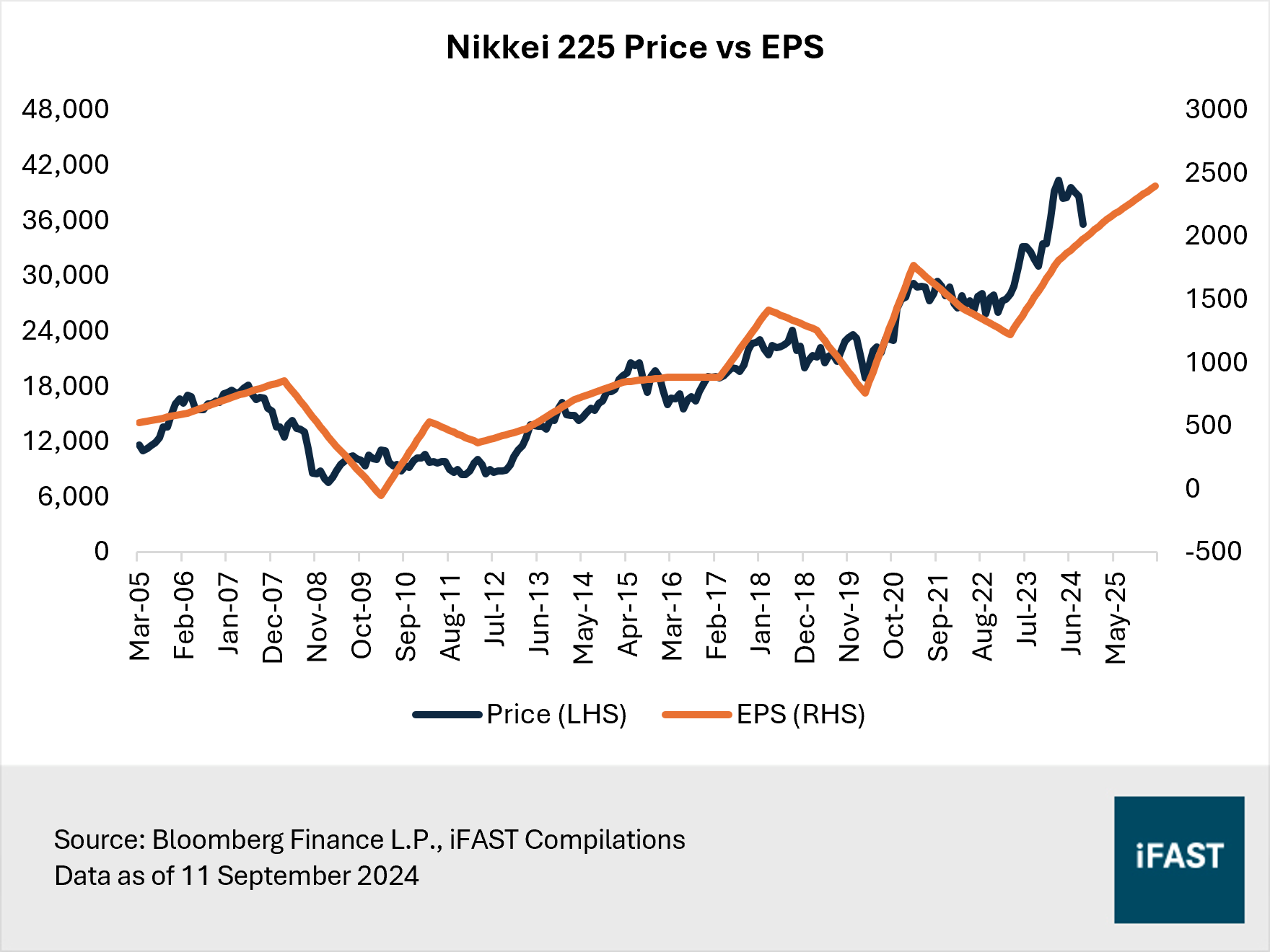

Figure 1: The Nikkei 225 Index has partly rebounded from its dip in early August

(Related article: BOJ hikes rates again. Buy the dip in Japan.)

Japan raises outlook of its economy

In our view, the BOJ is likely to adopt a cautious approach rather than opting for rapid rate increases. The central bank is data-dependent and has indicated that it will continue to raise interest rates and tighten monetary policy only if growth and inflation remain on track.

There are reasons to remain optimistic about the economic environment even after the July hike. In its August report, the Japanese government upgraded its monthly economic assessment for the first time in 15 months, citing signs of a recovery in consumption. Retail spending in Japan has been positive for the 28th consecutive month as of July 2024 as rising wages continue to support consumption.

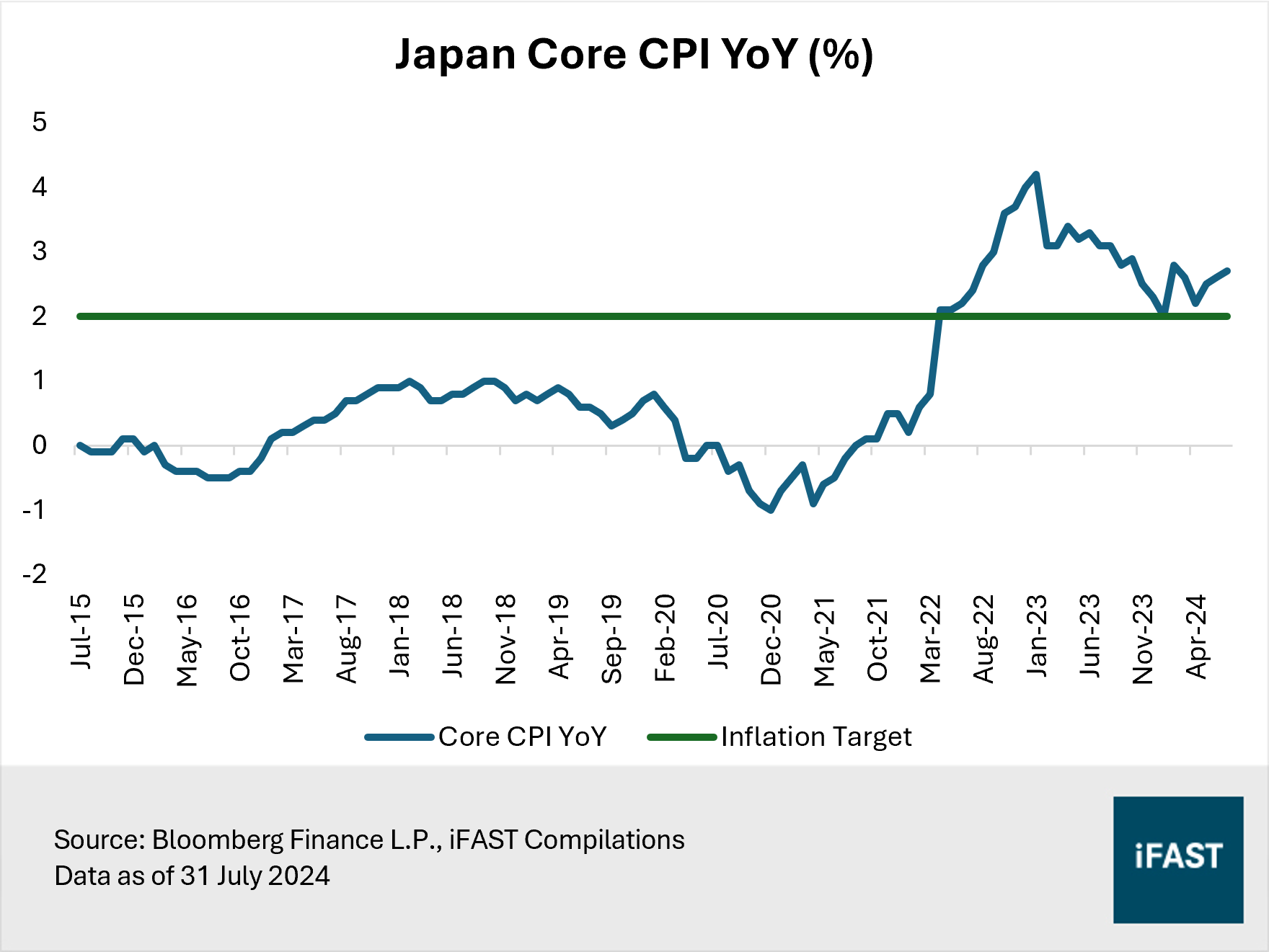

Meanwhile, the core consumer price index (CPI) accelerated for the third consecutive month in July. Standing at 2.7%, it remains well above the BOJ’s 2% for over two years now (Figure 2). Companies have continued to pass on rising labour costs through price hikes. This year’s shunto wage negotiations saw companies raising wages north of 5% on average, the highest in over three decades. The Japanese labour market will likely remain structurally tight in the coming years due to demographic changes. This should result in persistent wage pressures moving forward, and consequently higher inflation.

Figure 2: Inflation appears to be sticky

For too long, Japan's economy has been mired in a deflationary mindset, where falling prices stifled investment and spending. Today, the change in corporate attitudes towards price hikes is finally within reach. To illustrate Japan moving away from its deflationary norms, consider Sony’s recent decision to raise prices across its gaming gear portfolio in Japan. Sony Group announced it will be raising the price of its PlayStation 5 in Japan by about 19%. The company also lifted prices of accessories like the DualSense wireless controller and Pulse wireless headset.

As Japan gradually moves away from decades of deflation and stagnant growth, the positive impact of economic normalisation cannot be understated. An economic environment of stable growth and inflation is likely to drive lasting changes in consumer and business behaviour in Japan, creating a virtuous cycle between wages and prices that would be beneficial for the economy and stock market for years to come.

A stronger yen won’t derail Japan’s growth

Historically, the Nikkei 225 tends to have a positive correlation with the USD/JPY exchange rate, meaning that a weaker yen often coincides with a stronger Nikkei 225, and vice versa. Based on our compilations, approximately 40% of companies in the Nikkei 225 derive more than half of their revenue from overseas, highlighting the export-oriented nature of many Japanese firms. Investors may be concerned that a stronger yen, driven by additional BOJ rate hikes, could disrupt the rally in the Japanese stock market.

But on a more positive note, we think a stronger yen can help to mitigate prevailing macro risks. A stronger yen reduces the cost of imports, alleviating pressure on consumers and manufacturers alike. This can bolster confidence which encourages increased consumption and investments that drive long-term growth. Besides, the yen appreciation could renew optimism of foreign investors and lead to higher inflows into Japanese assets.

It is also important to recognise that Japan is home to several quality businesses which provide a sustainable trend in earnings. These companies are characterised by strong market positions, innovative products, and robust business models that enable them to thrive even without the tailwind of a weakening yen.

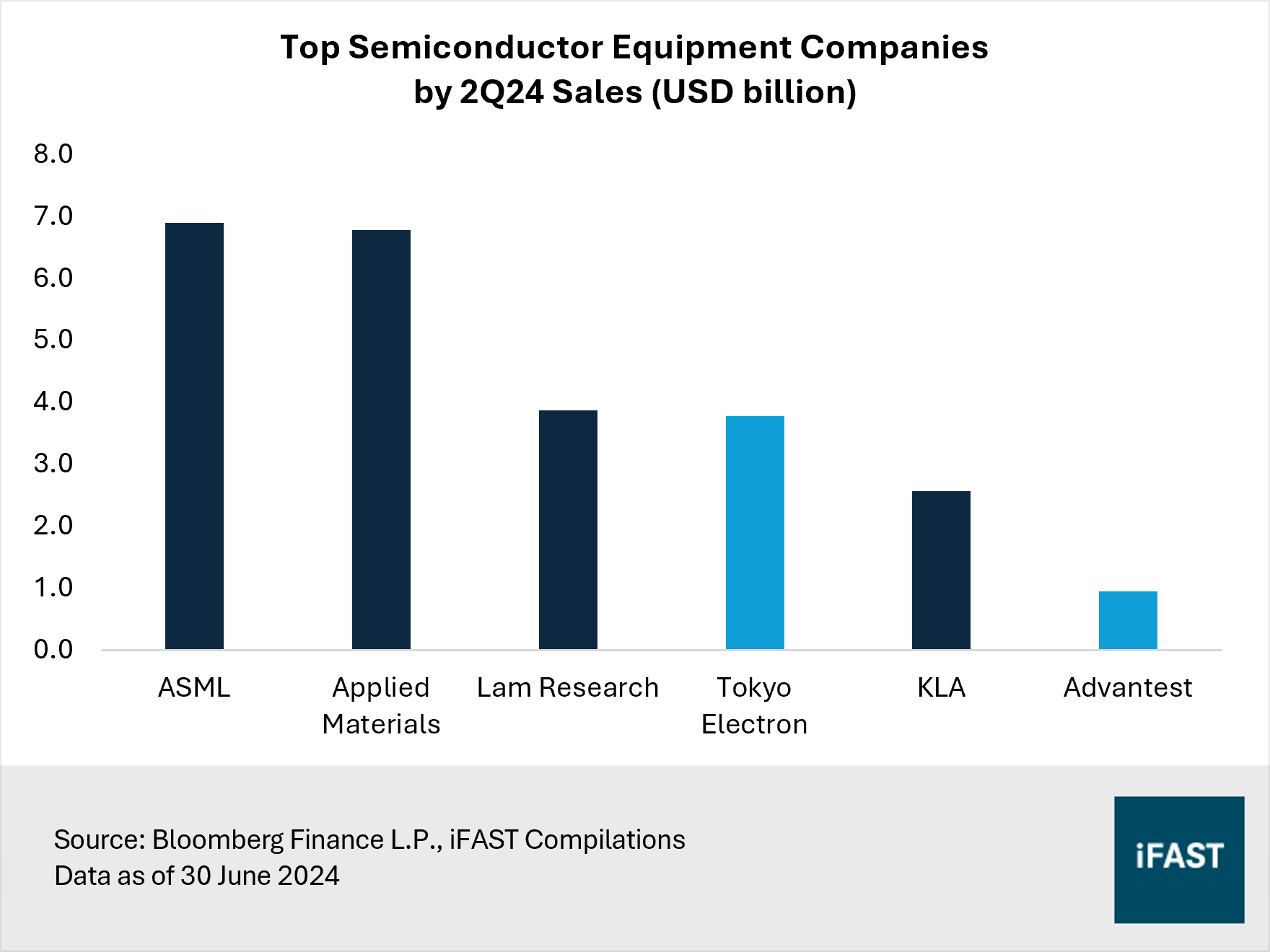

A case in point would be Japan’s semiconductor companies. Tokyo Electron and Advantest are among the world’s largest makers of semiconductor production equipment, serving chip giants like Intel, TSMC, Samsung, Micron, and NVIDIA (Figure 3). As of 30 June 2024, both companies derive almost all of their revenue from overseas.

Figure 3: World’s chip-making equipment giants

Tokyo Electron (TEL) denominates its export sales in Japanese yen (JPY). As a result, exchange rate fluctuations tend have a negligible impact on its revenue and profits. For the current financial year ended March 2025, TEL has projected double-digit percentage growth in the production of wafer fab equipment (WFE) helped especially by AI-linked demand.

Meanwhile, Advantest forecasts a 7.6% year-on-year increase in earnings for the financial year ended March 2025, driven by stronger demand for testers in high-performance computing (HPC) and AI. This projected earnings growth issued by the company, a reversal from the previous year’s decline, comes even as it anticipates the JPY to strengthen towards 140 per dollar.

Within the consumer discretionary sector, Fast Retailing, the parent company of Uniqlo, has built a robust global brand that emphasises quality, innovation, and affordability. The company estimates its profits for the financial year ended August 2024 to see an increase of 17% year-over-year, excluding the impact of forex (its estimates were calculated based on a USD/JPY exchange rate of 138.6). This is primarily driven by the strong sales of products that captured global mass fashion trends.

Beyond large-caps, the story is very different. Japan’s small and mid-caps are typically domestic-oriented; their revenues are generated primarily within Japan. As such, many could even benefit from a stronger yen as it reduces their import costs.

Overall, a stronger yen does not necessarily equate to a decline in earnings for Japanese companies. For large-cap stocks, we believe the inherent competitiveness of quality companies suggests that they are no longer dependent on a weak yen. For instance, TEL and Advantest are well-positioned to delivered sustained earnings growth by capitalising on global megatrends like digitalisation and AI. Meanwhile, small and mid-caps are potential beneficiaries of the yen appreciation. A stronger yen may also act as a stabilising force for the Japanese economy and capital markets.

(Related article: This market’s stock rally is likely far from over)

Long-term structural drivers remain in place

In addition, the normalisation of monetary policy and stronger yen does not take away Japan's compelling long-term growth story.

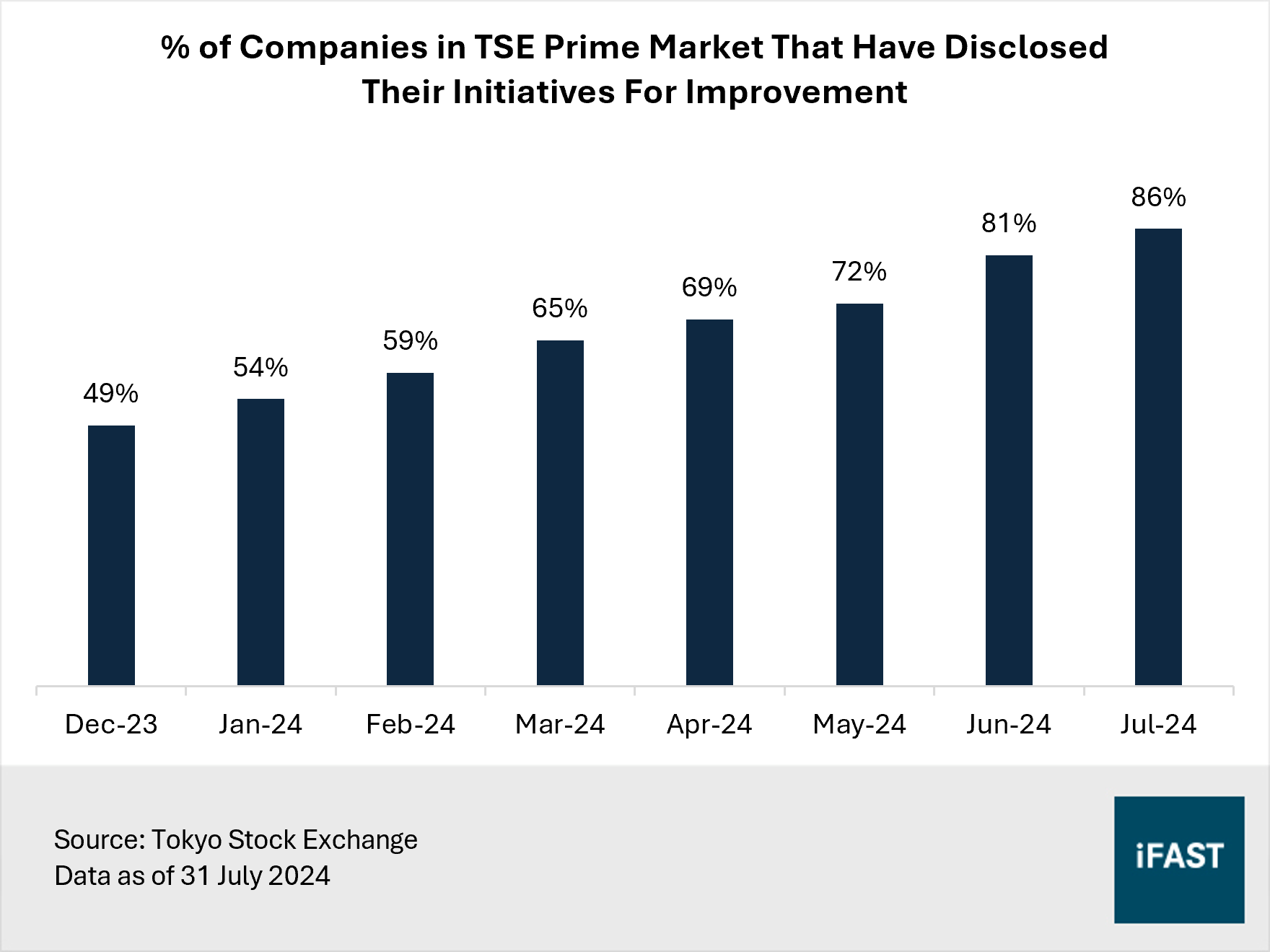

Japan’s commitment to corporate governance reforms has started to bear fruit as companies are increasing prioritising shareholder returns. As of 31 July 2024, 86% of companies listed on the Prime section (the market division with the highest listing standards) of the Tokyo Stock Exchange have responded to calls to enhance capital efficiency (Figure 4). This paves way for more dividends, share buybacks, and greater transparency in management practices, making Japanese equities more attractive on a global scale.

Figure 4: Corporate reforms are making progress

One notable example of this shift is the recent buyout offer for Japan’s Seven & i Holdings – the parent company of 7-Eleven – by Canadian convenience store giant Alimentation Couche-Tard. This deal has been watched closely at home and abroad as a litmus test of Japan’s evolving corporate landscape. Couche-Tard is pursuing deal talks after an initial rejection which cites the offer as too low and fraught with regulatory risks. Seven & i has signalled a willingness to consider a sweetened offer.

Previously, an attempt at such a transaction would have been dismissed as unlikely. For years, activist investors have pushed for change in Japanese corporations, only to be met with resistance from companies that insisted they were not for sale at any price. Despite increases in share prices in recent years, Japanese companies remain undervalued compared with counterparts overseas. As companies like Seven & i Holdings become more open to strategic acquisitions, it sends a strong signal to the market that Japan is no longer a place where capital is locked away at the detriment to shareholder interests.

From a broader perspective, Japan’s long-term growth story is underpinned by more than just favourable corporate governance trends. Japan, with a highly educated and skilled workforce, has a long history of technological innovation and is known for its advanced manufacturing capabilities. As the world faces the complexities of ongoing US-China rivalries, Japan is positioned to leverage its technological prowess to re-emerge as a dominant force in the global semiconductor industry.

At present, Japan is making a concerted effort to revive its lost status as a semiconductor powerhouse, fuelled by a combination of government support, strategic partnerships, and a renewed focus on innovation. Rapidus, backed by significant subsidies, plans to prototype its 2-nanometre chips next year, with mass production set for 2027. The company aims to leverage robots and AI to establish a fully automated production line, enabling it to deliver chips in just a third of the time compared to its rivals.

Japan: Seize the opportunities

In our view, Japan remains as one of the most promising markets in the years ahead. Investors should not be deterred by noise or short-term volatility. Instead, the focus should be on the underlying fundamentals. The BOJ’s measured approach to rate hikes signals confidence in the country’s economic resilience and marks the beginning of a return to more normalised conditions. Furthermore, Japan’s commitment to enhancing shareholder value could lead to the expansion of valuation multiples, while its resurgence as a semiconductor powerhouse further adds appeal to the market. Even with the potential of a stronger yen, there are compelling opportunities within the Japanese market.

We believe the dip in share prices from their July peak has further improved Japan’s risk-reward profile, making it hard to ignore. Investors should increase their positions in Japanese stocks while valuations are still compelling. We maintain our target price of 48,000 for the Nikkei 225 Index, derived based on a fair PE ratio of 20X applied to our 2026 EPS estimates. This translates into an upside potential of 35% as of 11 September 2024.

We recommend investors to maintain exposure to the yen through an unhedged share class. This way, any appreciation of the yen would contribute to the total returns received by investors.

Figure 5: Share prices are driven by earnings

Table 1: Projections for the Nikkei 225 Index

|

|

2023 |

2024 |

2025 |

2026 |

|

PE Ratio (X) |

25.9 |

19.6 |

16.7 |

14.8 |

|

EPS |

1,292 |

1,813 |

2,135 |

2,400 |

|

Earnings Growth |

-11.5% |

40.3% |

17.8% |

12.4% |

|

Target Price (based on 20X Fair PE) |

48,000 |

|||

|

Potential Upside |

35% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 11 September 2024 |

||||

Table 2: Recommended products

|

Market |

Product |

Comments |

|

Japan |

Looks into underappreciated stocks, has substantial exposure to small-mid companies compared to benchmark |

|

|

Top constituents of Nikkei 225 include Fast Retailing, Tokyo Electron |

||

|

Japan (Small Cap) |

Small-caps likely to benefit from a stronger yen (Related article: Uncover hidden gems with Janus Henderson Horizon Japanese Smaller Companies Fund) |

|

|

Japan (Dividend Paying) |

Banks are among top holdings, which are beneficiaries of rate hikes |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")