' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

• In 2024 our MAPS Growth portfolios delivered returns ranging from 5.8% to 12.9%, while our income portfolios saw returns of between 5.1% and 11.9%.

• The most significant change we made to the portfolios in 2024 was to transition away from a GDP weighted approach, opting instead for a more conventional market-cap weighted approach.

• Looking forward, we intend to take a prudent approach towards asset allocation - maintaining a neutral stance on both equities and fixed income.

• We like high quality companies, such as those with strong economic moats and resilient earnings. We favour developed markets such as US and Japan, which are both supported by structural tailwinds.

• As for fixed income, our preference is to maintain an overweight on short duration bonds. We look to gradually extend duration when (i) the yield curve steepens further, and (ii) 10-year UST yields move sustainably towards the 5% mark.

2024 MAPS portfolio performance wrap

2024 was an eventful year for global markets and our portfolios.

Over the past year, our MAPS Growth portfolios delivered returns ranging from 5.8% to 12.9%. Returns for the income portfolio in 2024 were comparable, ranging from 5.1% to 11.9%. While the performance of the conservative and moderately conservative portfolios trailed their more aggressive counterparts, they still managed to deliver positive gains of 5.8% and 7.3% respectively, despite a turbulent environment for fixed-income assets. The balanced portfolio also did fairly well, delivering returns of 9.3%.

Finally, the moderately aggressive and aggressive portfolios were the top performers in 2024, delivering the highest absolute return among all five portfolios at 11.0% and 12.9% respectively. Since inception, the growth portfolios have delivered returns between 11.1% and 55.9% (Figure 2).

Figure 1: Performance of MAPS Growth portfolios for 2024

Figure 2: Portfolio performance since inception (MAPS Growth)

What did we do well, and what can we improve on?

Throughout the year, we made several adjustments to our portfolios in response to changing market conditions and to better align with our longer-term outlook. Let's take a look at what went well and what can be improved.

Among the things that we have done well in 2024 was to increase our equity exposure from underweight to neutral. This change, which was implemented early in the Jan 2024 has allowed our portfolios to benefit from the strong performance of equity markets. Over the course of 2024, the MSCI AC World Index delivered returns of 22.3% (equity market returns in SGD terms unless stated otherwise) compared to a -1.7% return for fixed income.

We also took the opportunity to increase our exposure to growth while reducing our exposure to value stocks. This adjustment also had a positive impact on portfolio performance as growth stocks, particularly those from the US technology sector, outperformed their value counterparts by a wide margin last year (Figure 3).

Figure 3: Growth continued its strong performance against value in 2024

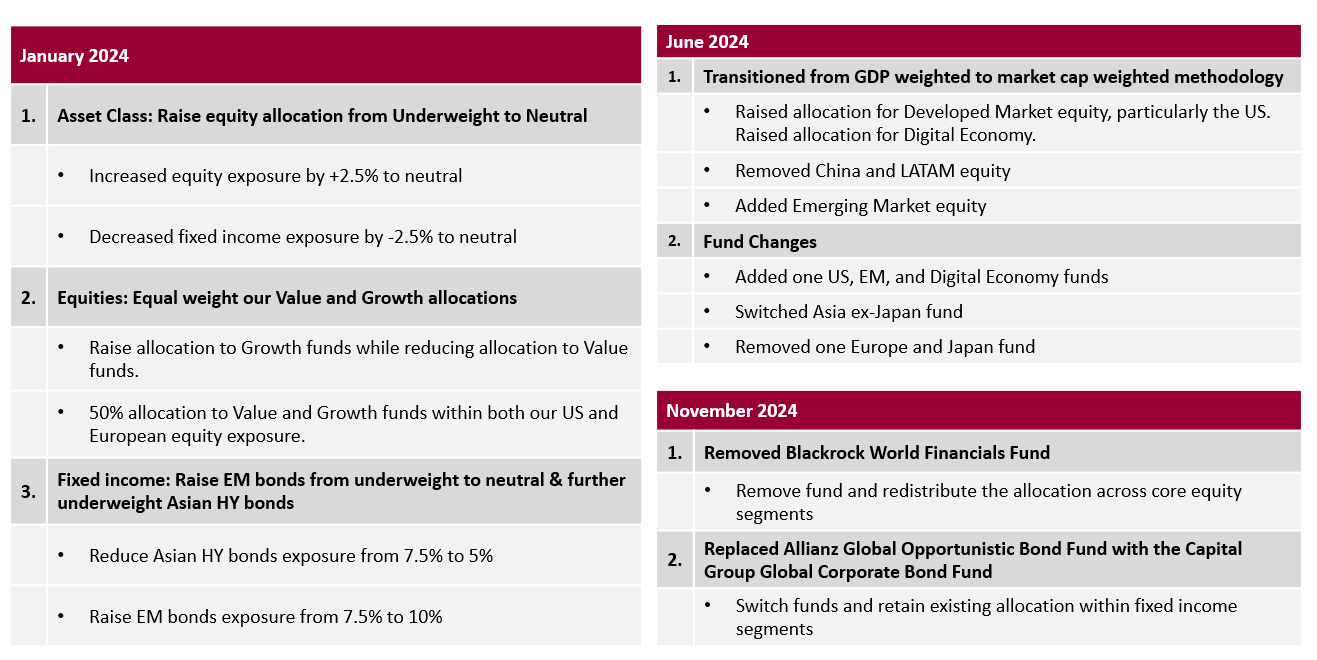

The biggest change that we made was in June 2024, when we transitioned away from the GDP-weighted approach, opting instead for a more conventional market-cap weighted approach. While this is a drastic change, we felt that it was necessary, and more importantly in our client’s best interest as the GDP weighted methodology was fast losing its relevance and ill-aligned with our long-term views.

In a nutshell, this shift reduced our portfolios' exposure to emerging markets like China while increasing exposure to developed markets such as the US and Japan, where we see greater opportunities. In addition, we also doubled our allocation to digital economy stocks, from 10% to 20% to reflect our long-term view that this sector will continue to play a major role in driving innovation and shaping the future of global markets.

Although it has only been six months since we implemented these changes, they have already positively impacted our portfolios as developed markets outperformed emerging markets by 5.3% in 2H24. Digital economy stocks have also done well, rising close to 15% on aggregate over the same period.

Table 1: Equity neutral allocation post methodology change

|

Market |

Old Neutral Allocation |

New Neutral Allocation |

|

US |

23.5% |

40.0% |

|

Europe |

23.0% |

16.0% |

|

Japan |

6.0% |

9.0% |

|

Asia ex-Japan |

25.5% |

10.0% |

|

Latin America |

6.0% |

- |

|

China |

6.0% |

- |

|

Emerging Markets |

- |

5.0% |

|

Digital Economy |

10.0% |

20.0% |

|

Source: iFAST |

||

Related Article: Transitioning from GDP-weighting: Our new portfolio strategy revealed

On the fixed income side, our decision to maintain an overweight position on short duration bonds has worked out well for us.

Despite the Fed cutting rates by 100bps last year, bond yields have risen significantly, leading to heavy losses in longer duration bonds. Most notably, the benchmark 10-year UST yield surged approximately 70bps in 2024, reflecting the rapid shift in investor expectations as the US economy turned out to be more resilient than previously anticipated.

Still, our short duration bond funds managed to deliver gains of 4.2% on average last year, compared to a -1.7% decline for the global bond benchmark. Their positive performance, coupled with the significant overweight (+7.5%) of the short duration segment played a pivotal role in the outperformance of our conservative and moderately conservative portfolios (relative to their respective benchmarks) in 2024.

Now, let’s take a look at what could we have done better.

One area which we can improve on is in fund selection. Using Japan as an example, while our overweight position has allowed us to capture the stock market rebound, our fund selection fell short of expectations. In 2024, our fund pick - the Eastspring Investments - Japan Dynamic AS SGD saw a gain of just 8.2%, compared to a gain of 12.1% for the Nikkei 225 Index.

Another area where we could have done better is our tactical portfolio. Among the three tactical ideas, the JPMorgan Global Natural Resources was the bottoming performing fund, ending the year with a loss of -3.5%. Despite elevated inflation levels in most countries, weak demand from China - driven by its economic challenges, posed a significant headwind for the sector. On a more positive note, the Principal ASEAN Dynamic Fund returned 19.6% over the year, while the Blackrock World Financials Fund returned 33.5% between Jan to Nov 2024 (when we exited the position).

Lastly, the timing of the transition from the GDP-weighted approach to a market-cap weighted approach. While there have been noticeable improvements since we made the change, making this transition earlier would have yielded a greater positive impact on our portfolios.

Table 2: Summary of portfolio changes made in 2024

Portfolio positioning for 2025

Given that we have already made several major changes to our portfolios last year, we do not anticipate making any drastic adjustments in the foreseeable future unless necessary. Looking ahead, we remain firm on our prudent approach towards asset allocation – maintaining our neutral stance on both equity and bonds.

Within global equities, we continue to favour developed markets such as the US and Japan, both of which are supported by structural tailwinds. We expect US exceptionalism to endure even in an increasingly uncertain world.

The country is home to numerous high-quality companies spanning various industries, particularly in the tech sector. And because these companies hold dominant positions both domestically and internationally, they benefit not only from growth in the US but also from global expansion. Moreover, their globally diversified operations help ensure that a downturn in one market would not significantly impact their overall revenue and earnings.

Within the US equity market, we are especially keen on the digital economy and semiconductor sectors, both of which have a substantial allocation in our portfolios. We believe that structural megatrends, such as the rise of artificial intelligence and the digitalisation of the global economy will greatly benefit US big tech companies, given the dominant positions they hold.

While the recent release of DeepSeek has sparked debates over the massive investments big tech companies have poured into AI and how effectively these resources have been utilised, we remain unfazed. We think that by evaluating and adopting DeepSeek’s cost effective training methods, big tech companies will potentially be able to get more out of their AI capex. Additionally, their unfettered access to cutting edge AI chips also gives them an edge over their Chinese peers. On aggregate, we expect US tech companies to deliver earnings growth well in excess of double digits over the next two years, which should push share prices even higher.

We also like Japan given the structural changes to the economy and stock market. The country is currently undergoing a period of structural transformation from deflation to inflation. Core inflation has remained above the BOJ’s 2% target for over two years now, with the latest reading (Jan 2025) coming in at 3.2% year-on-year, marking the highest level since June 2023.

Earlier in January, the Bank of Japan raised interest rates to the highest level in 17 years. Policymakers pledged to continue hiking rates as wage and price pressures broaden. Recent macroeconomic data also paints a picture of resilience. Japan’s GDP grew 0.7% in the fourth quarter, topping estimates of 0.3% boosted by a jump in exports.

On the fixed income front, our intention is to keep our overweight on shorter duration and higher quality bonds as we head into 2025. Our decision to overweight shorter duration bonds has worked out well for us in 2024 and we believe that this will continue to be the case for the foreseeable future.

Despite the Fed cutting rates by 100 bps last year, bond yields have risen significantly. Most notably, the 10-year UST yield surged approximately 70 bps in 2024, reflecting the rapid shift in investor expectations. This comes as the US economy remains resilient, with inflation likely to stay elevated for an extended period. Donald Trump’s trade policies have also brought about more uncertainty, clouding the inflation outlook.

At this juncture, we do not feel that investors are adequately compensated for taking on duration risk. Our preference is to see further yield curve steepening, along with 10-year UST yields moving sustainably towards the 5% mark before gradually extending duration. Until then, we believe that the right place to be is still in shorter duration bonds.

Markets are fraught with uncertainty, with investor sentiment easily swayed by the latest news. In such times, we believe it is wise to adopt a forward-looking, fundamentals-based approach to investing. While the path ahead might not be smooth, we believe that our portfolios are adequately positioned for now. We will continue to monitor markets closely and make timely adjustments if necessary.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")