' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

• With inflation concerns and weak economic growth ahead, we see divergence amongst developed markets, with Europe being expected to produce the weakest GDP growth in 2024.

• With our expectations that interest rates would remain higher-for-longer, Europe would feel a swifter transmission of interest rates due to a higher percentage of corporate borrowings at floating rates.

• China’s ongoing economic challenges would reduce cross border trade and foreign direct investments with Europe, denting its economy’s growth prospects overtime.

• Europe faces longer term structural issues, such as the lack of energy self-sufficiency and low productivity growth.

• Based on our revised fair PE ratio of 14X, we project a target price of EUR 553 for the STOXX 600 Index, translating to an upside potential of 15.9% by the end of 2025. We maintain the Star Rating for Europe at 2.5 Stars “Neutral”.

Europe’s economy managed to narrowly escape a recession in the first half of 2023, but the situation has gotten worse in the second half of the year, with interest rate hikes by the European Central Bank (ECB) and weak growth in China weighing on its economy. As we head into 2024, we think that Europe would experience the weakest growth, making it most susceptible to a recession amongst developed markets if economic conditions deteriorate.

Inflation conundrum and weak economic growth

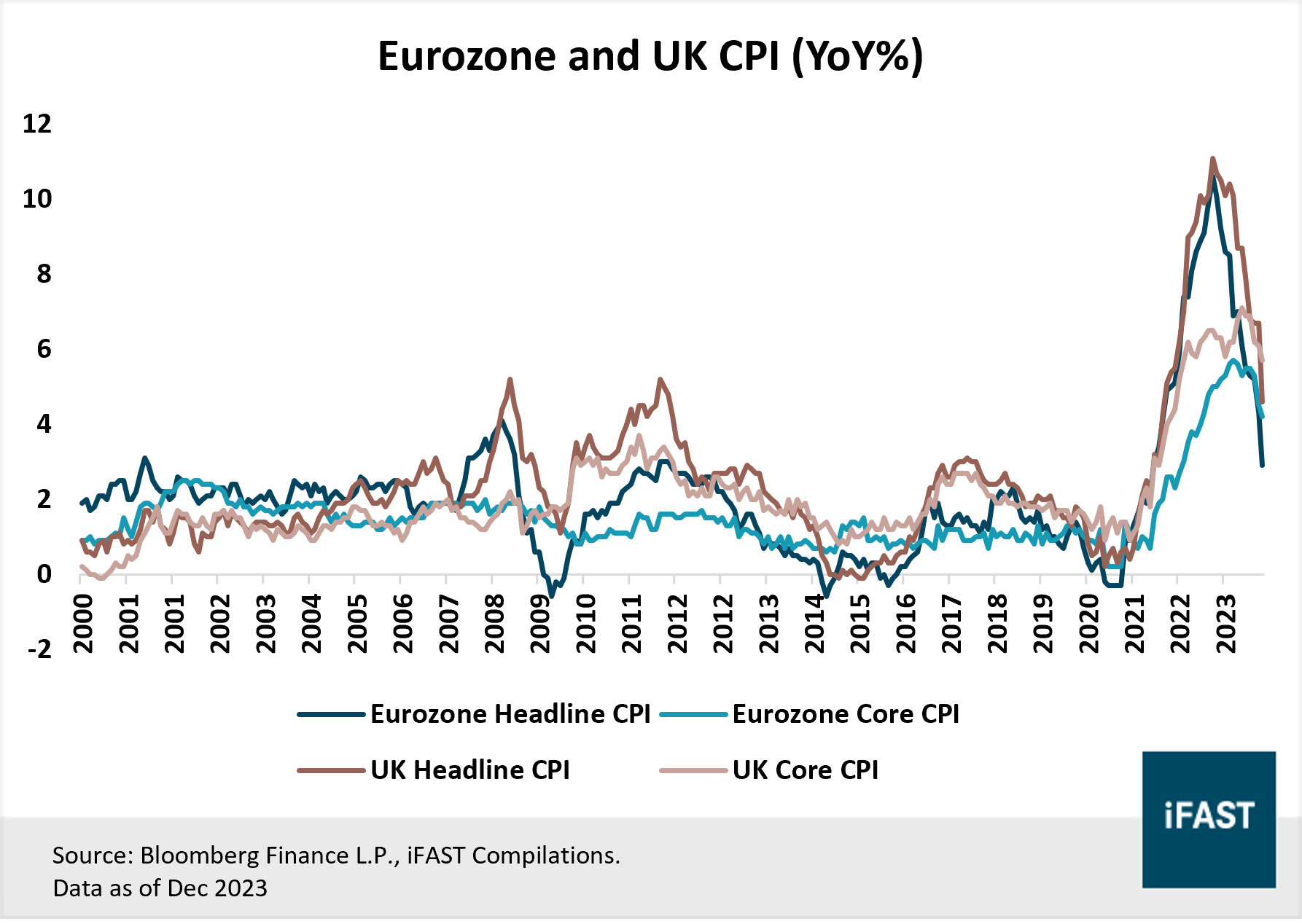

Although headline inflation in the Eurozone has already peaked and has been steadily trending down, core inflation remains elevated at 3.6% year-over-year (YoY), above the 2% target set by the ECB (Figure 1).

Figure 1: Core CPI in Eurozone and UK remains elevated

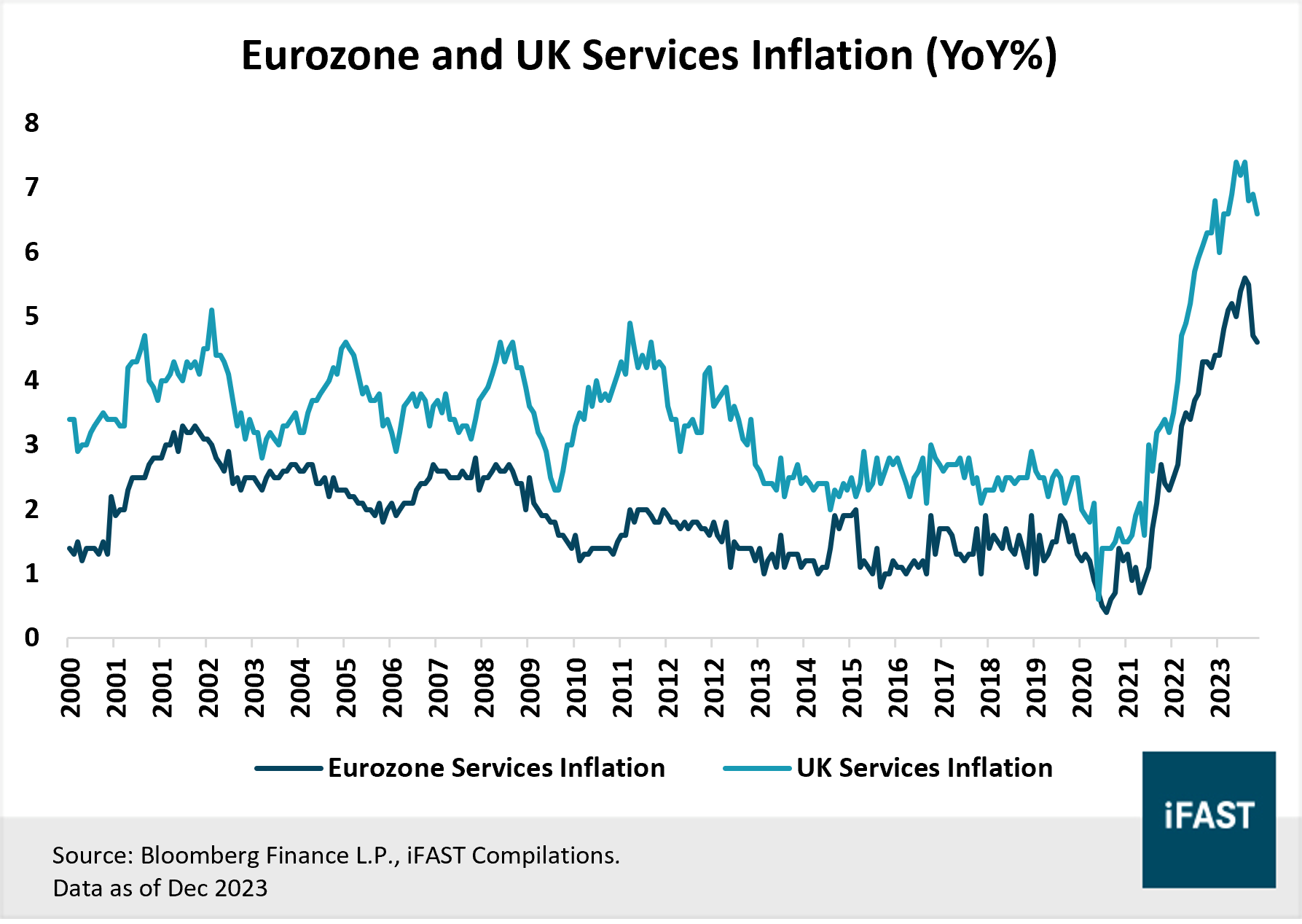

The case is even more severe over in the UK, where both headline (4.6% YoY) and core inflation (5.7% YoY) remain well above the Bank of England’s (BOE) 2% target, while services inflation continues to remain sticky. (Figure 2).

Figure 2: Services inflation remains sticky, particularly in the UK

Although markets expect inflation to continue declining gradually, we believe Europe is unlikely to reach inflation targets anytime soon, as the bulk of the recent deceleration in inflation was driven by falling energy prices, given the high base effects from last year. We also believe that getting core inflation down to the 2% target would prove challenging because of sustained wage growth, coming in at 4.6% YoY in the second quarter of 2023. Labour markets have remained tight with the unemployment rate hovering close to its historical low at 6.5%, and services inflation continues to remain sticky.

Besides the inflation conundrum, economic growth in Europe is expected to remain sluggish. Consumer spending continues to weaken in the face of rising borrowing costs and higher prices, as evident by Europe experiencing 13 consecutive months of negative retail sales growth on a YoY basis.

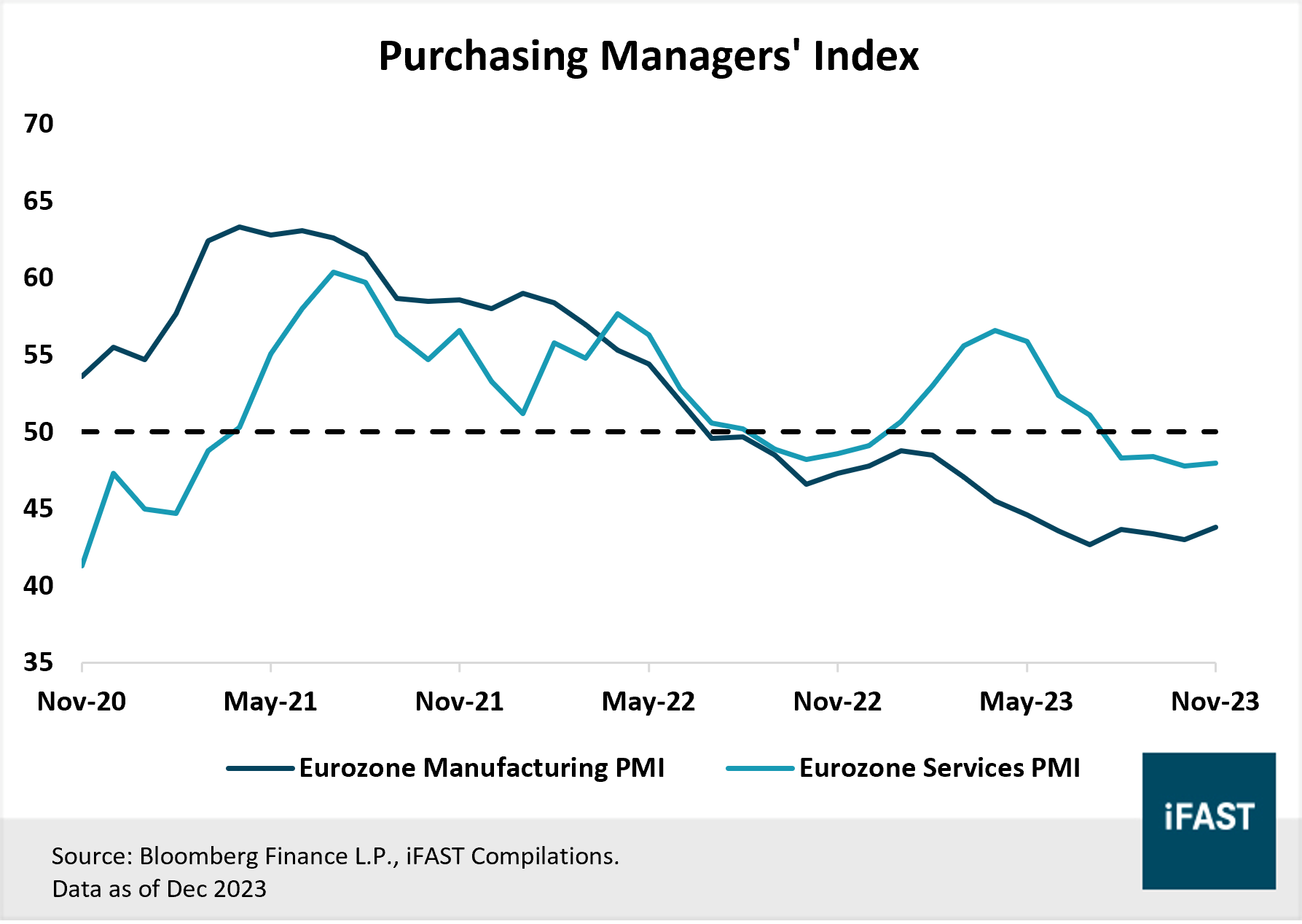

Other economic indicators are also showing signs that Europe’s economy is slowing down. If we look at the Eurozone’s manufacturing sector (accounts for a fifth of the GDP), it has been shrinking with manufacturing PMI stalling since the middle of 2022. Meanwhile, services PMI has also declined into contractionary territory in recent months, indicating that the momentum in the services sector is diminishing as well.

Figure 3: Eurozone PMI data remains in contractionary territory

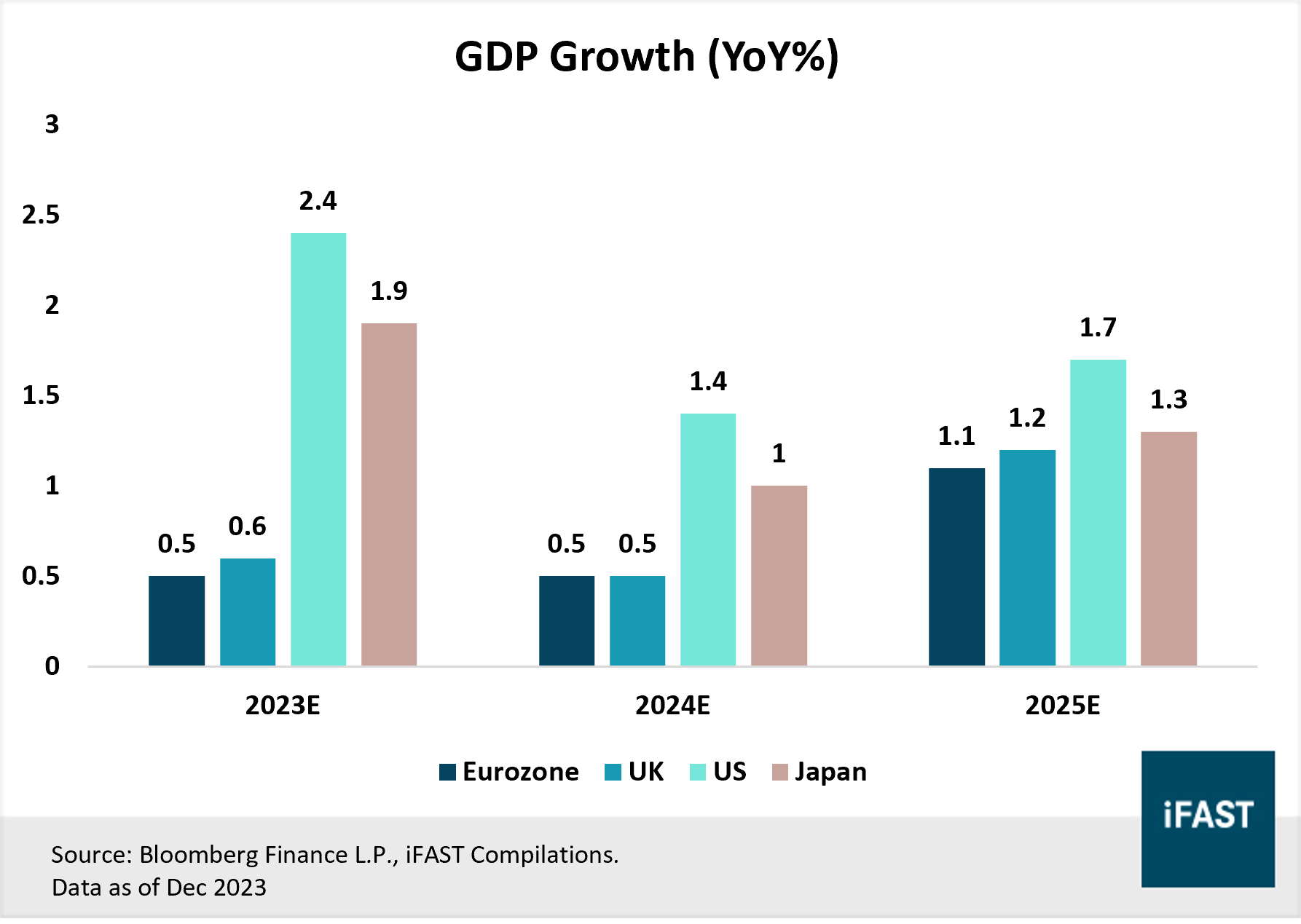

The overall slowdown in Europe stands in contrast to other developed markets (Figure 4) such as US and Japan. Therefore, we see divergence amongst the developed markets, with Europe expected to produce the weakest GDP growth in 2024, making it the most susceptible to a potential mild recession should economic conditions worsen.

Figure 4: Projected GDP growth for major developed markets

Restrictive monetary policy to impact Europe more drastically than US

While the ECB has likely reached the peak of its interest rate cycle, we do not hold the view that the ECB would cut rates early next year, due to sticky inflation as mentioned earlier. In our view, we believe a prolonged restrictive stance would be necessary to ensure that inflation moves back to its 2% target, so as to avoid a policy mistake that could reignite inflation to the upside.

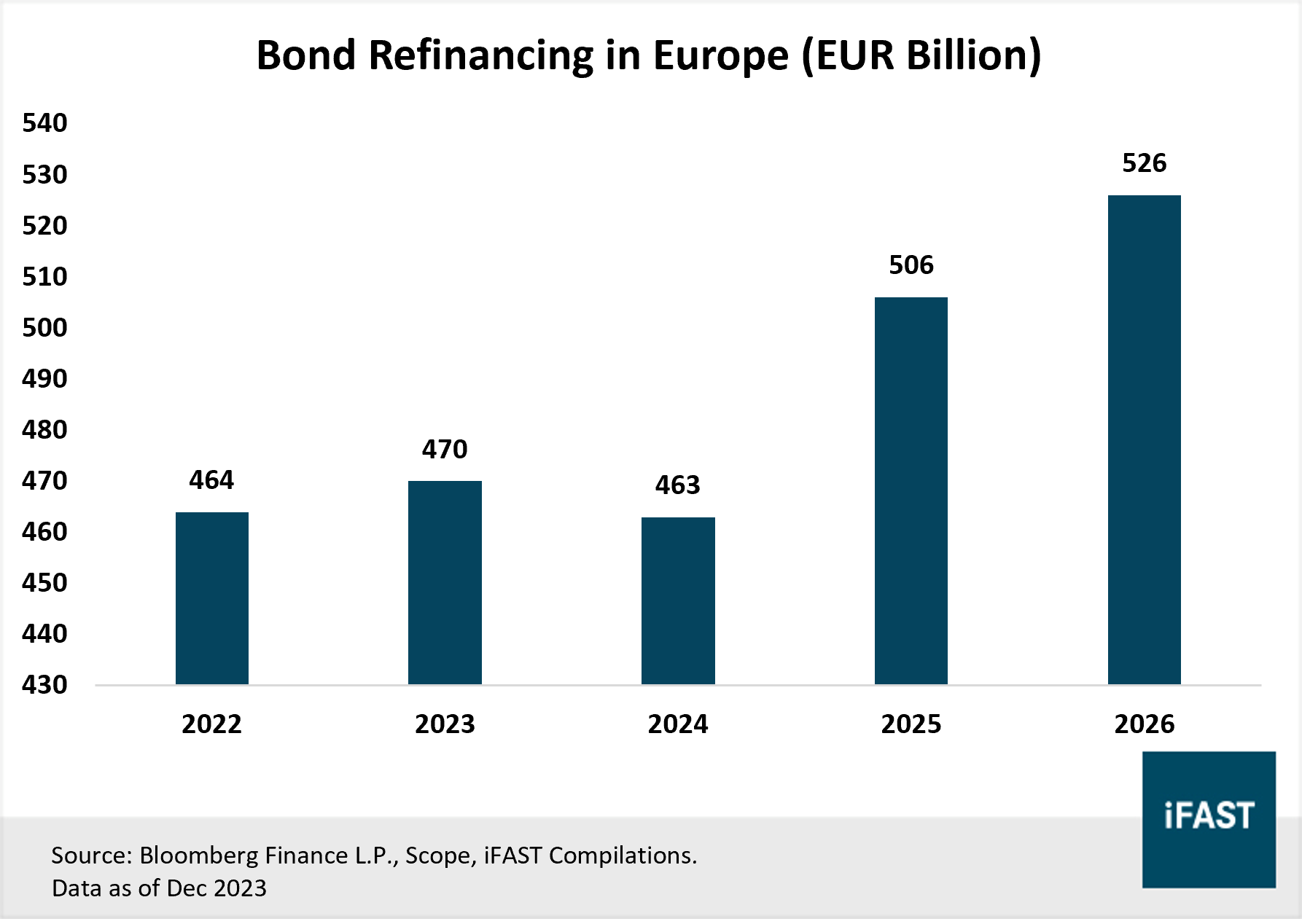

With this in mind, refinancing challenges are expected to surface in the public debt market as we progress into the next three years, as refinancing volumes for bonds issued by entities in Europe would rise from the EUR 460-470 billion in 2022 to 2024, to over EUR 500 billion in 2025 and 2026 annually as they mature (Figure 5). As these companies refinance at higher rates in the next few years, the rise in interest costs would test the resilience of corporate borrowers and cause a squeeze on their balance sheets.

Figure 5: Bond refinancing volume of Europe-based non-financial companies (as of Sep 2023)

To make matters worse, as compared to the US where over 80% of the corporate borrowings comes from public debt markets primarily at fixed rates, over 70% of corporate borrowings in Europe are sourced from banks, primarily at floating rates.

The reason behind the high percentage of corporate borrowings from banks at floating rates was because bank lending was supported by government guarantee schemes during the pandemic and the Russia-Ukraine war. Back then, interest rates from bank lending were also low, causing many firms to shift away from debt issuance from the public market.

However, in this high interest rate environment, companies which borrowed at floating rates not only face refinancing challenges, but also incur higher interest expenses and debt servicing costs. This could reduce their profit margins and potentially increase the risk of a default. Therefore, as the delayed impacts of monetary policy take effect, we foresee that Europe would be more severely impacted than the US, since the transmission of interest rates in Europe would occur more rapidly.

Slowing growth in China to weigh on Europe’s economic activity

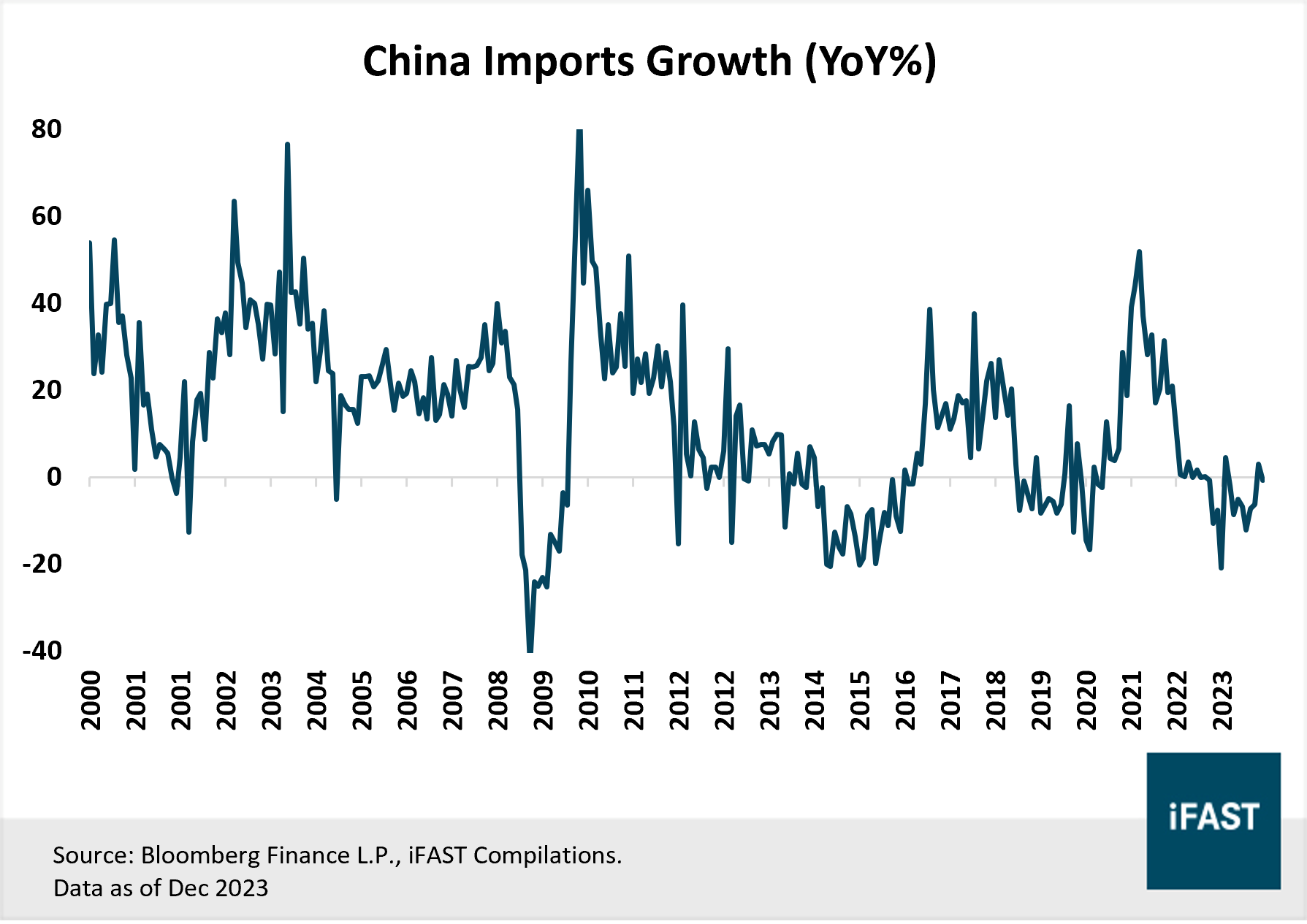

China’s lingering economic challenges would also have a significant impact on Europe’s economic growth. For instance, China’s imports have remained weak (Figure 6), and this would negatively impact Europe via reduced exports to China. After all, China is Europe's third-largest export partner, representing around 9% of EU exports.

Figure 6: China imports remain sluggish

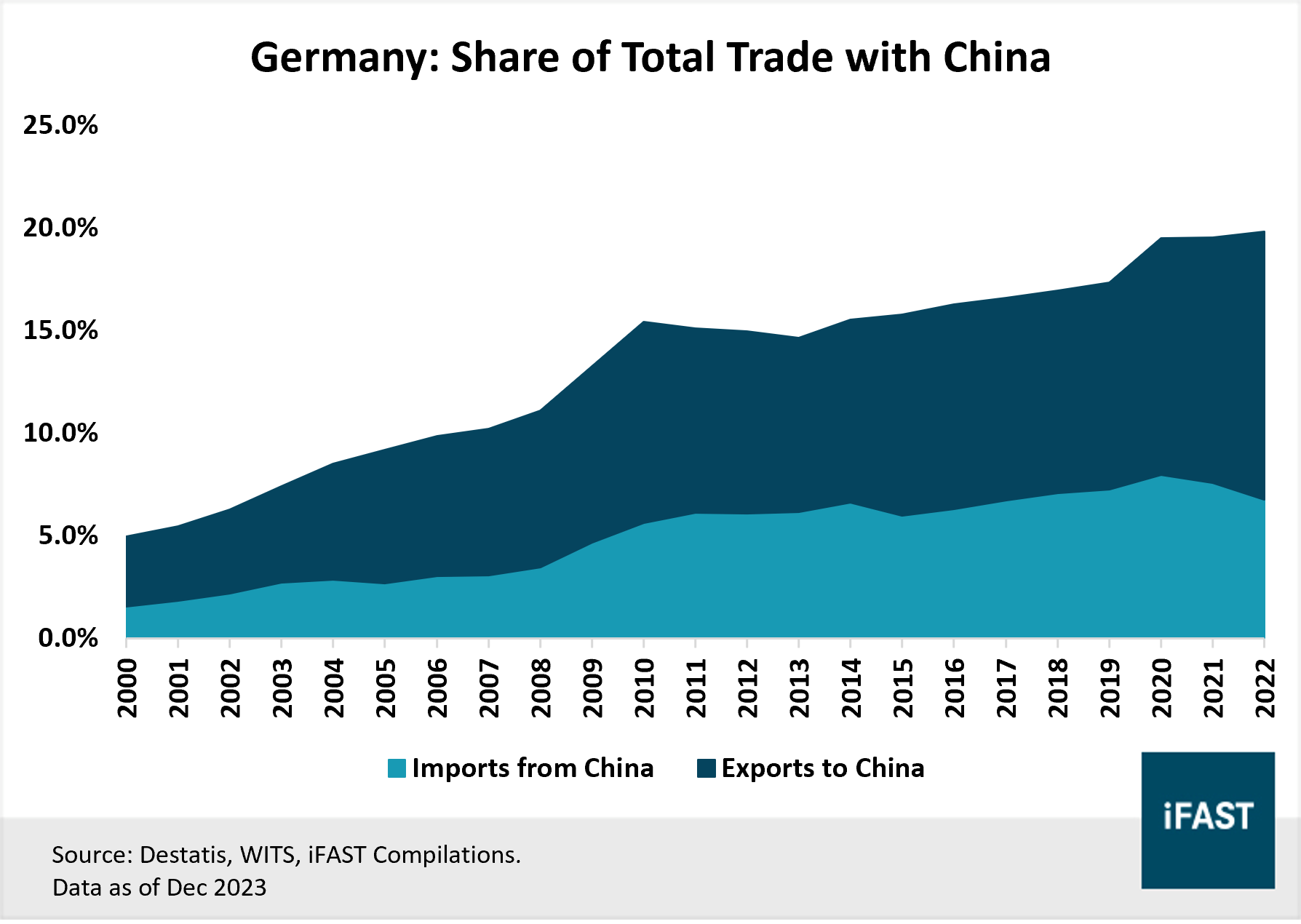

Germany, which is by far the largest economy in Europe would especially be impacted by China’s import slump. China accounts for about 20% of total German trade (Figure 7), with major German companies being the most exposed to a slowing Chinese economy as they rely on China’s massive market for the demand of their goods. This dependence on China would drastically affect the growth of large German corporates and in turn, cause a drag on Germany’s economic growth.

Figure 7: Germany’s increasing dependence on China for foreign trade

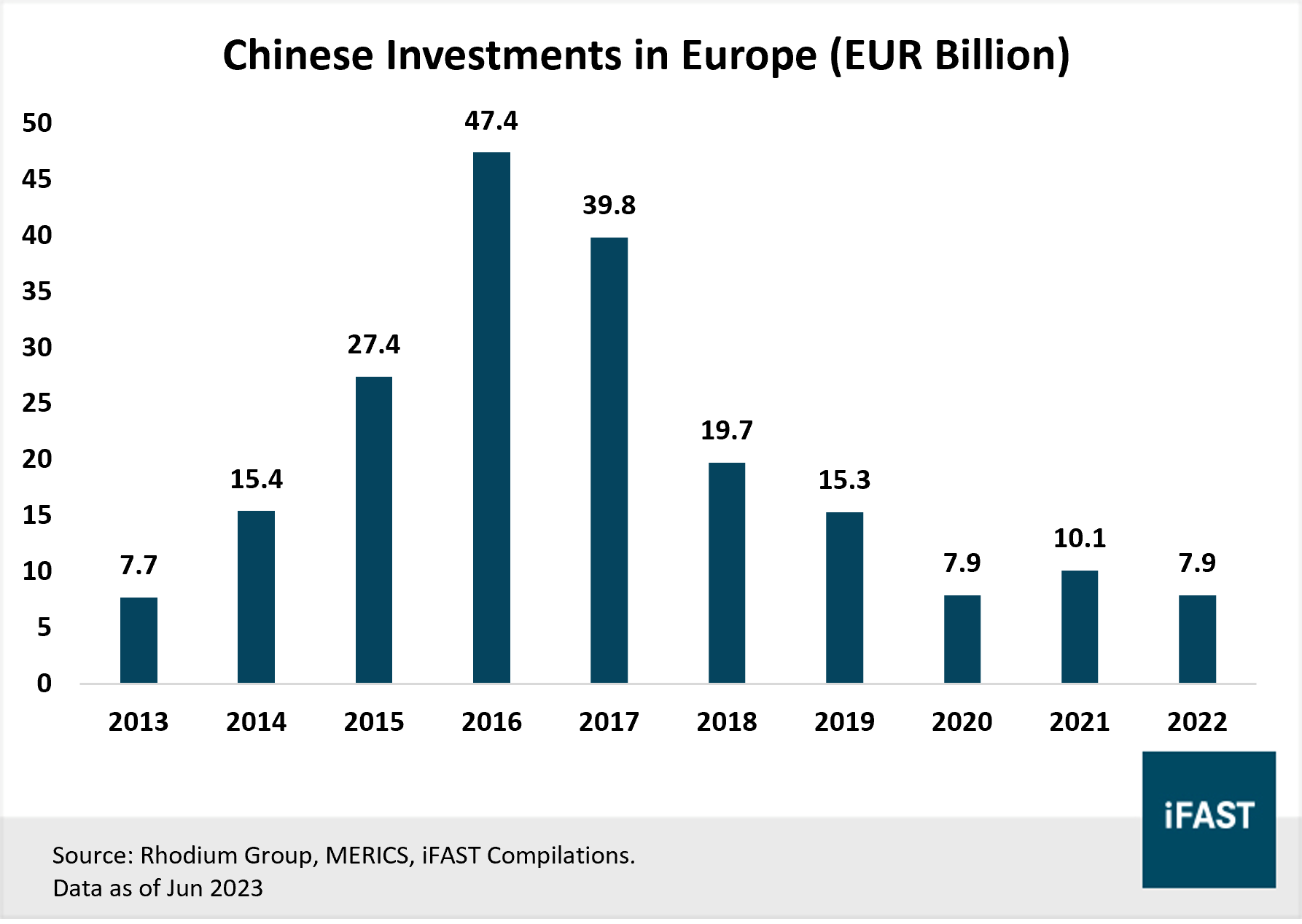

Meanwhile, China's faltering economic recovery and prioritisation of cultivating local companies to secure technology self-sufficiency have also led to a decline in investments in Europe (Figure 8). In 2022, China's foreign direct investments (FDI) in Europe has hit one of its lowest points in the past ten years, amounting to approximately EUR 7.9 billion. Over time, if we continue to see a decline in investments from abroad, it could result in a slowdown in technological advancements and decrease the competitiveness of European workers and firms, ultimately affecting economic growth as Europe loses its appeal as an innovation hub.

Figure 8: China’s FDI in Europe continues on its downward trajectory

With the combination of lower trade volumes and investments with China, Europe’s economic growth would be greatly impacted as we head into the next year.

Longer term structural problems facing Europe

Finally, Europe faces longer term structural problems, which would continue to weigh on its overall economy overtime.

Lack of energy self-sufficiency

Although Europe has made progress in weaning itself off Russian and imported energy by investing heavily in their own infrastructure, this pro¬cess will take years to scale up before they can gain self-sufficiency. Given that energy-intensive industries (EII’s) are at the core of European industries and encompass steel, paper or food industry, among others, the high energy import dependency of Europe is an issue of energy security. Europe is thus vulnerable to disruptions in its energy supply, which could prevent the country from operating properly, thereby inhibiting economic growth and triggering job losses.

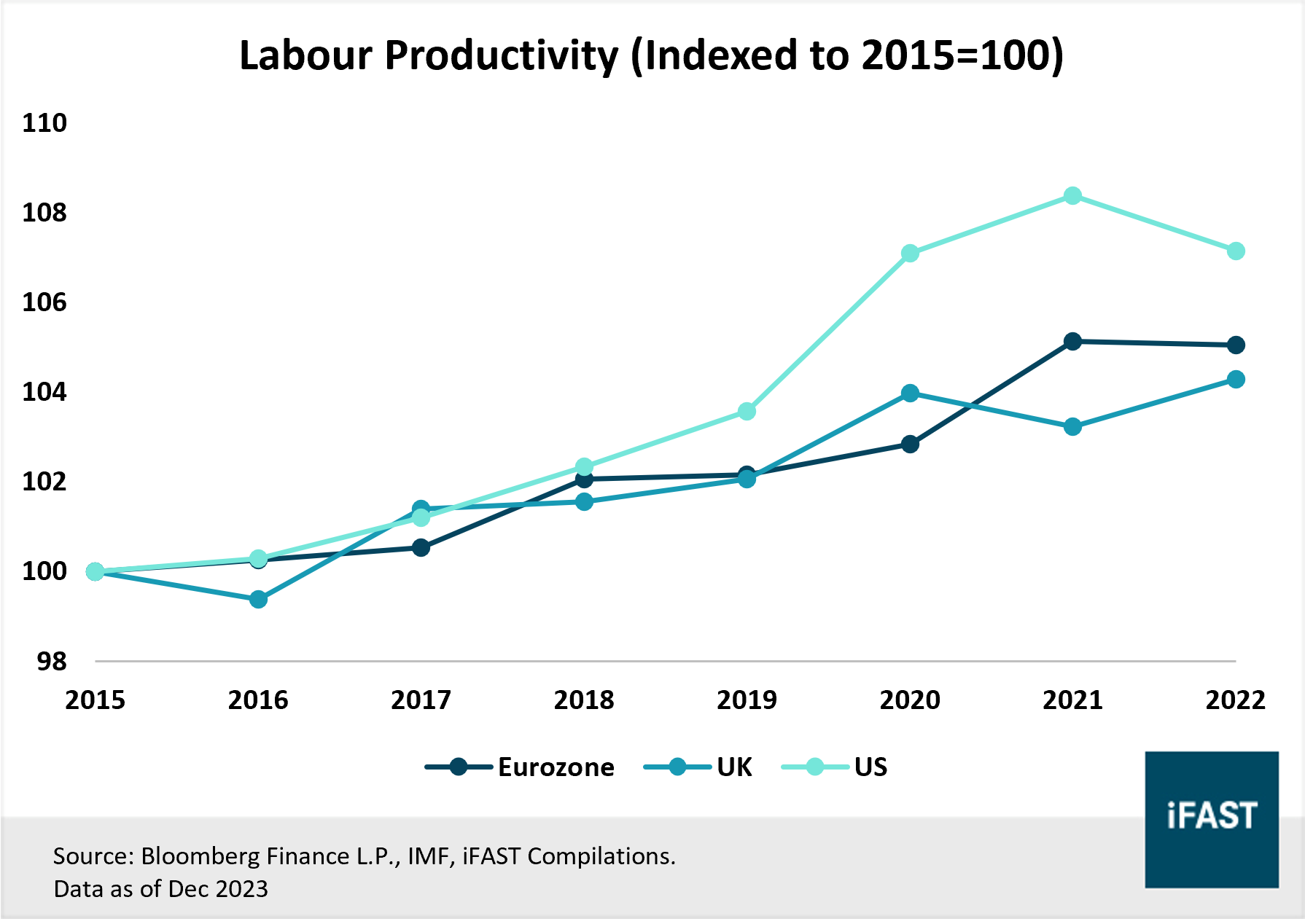

Low productivity growth

Europe is faced with weakening productivity growth, making its economy less competitive on the global stage. A growing preference for flexibility and working less due to change in mindsets limits labour supply, and also exacerbates inflation by keeping the labour market tight. Lastly, demographic pressures caused by an ageing population also reduces potential labour supply and productivity further, while adding to fiscal costs.

Figure 9: Labour productivity in Europe has been lagging behind

Beyond which, Europe has also fallen behind in terms of technological innovation, as seen from the number of world class patents in cutting-edge technologies, which are dominated by US, China and Japan. It would be crucial for European countries to invest heavily into the area of research and development to increase productivity growth over the long-run, or risk losing out to other countries.

Structural reasons warrant a fair P/E downgrade, maintain 2.5 Stars “Neutral” for European equities

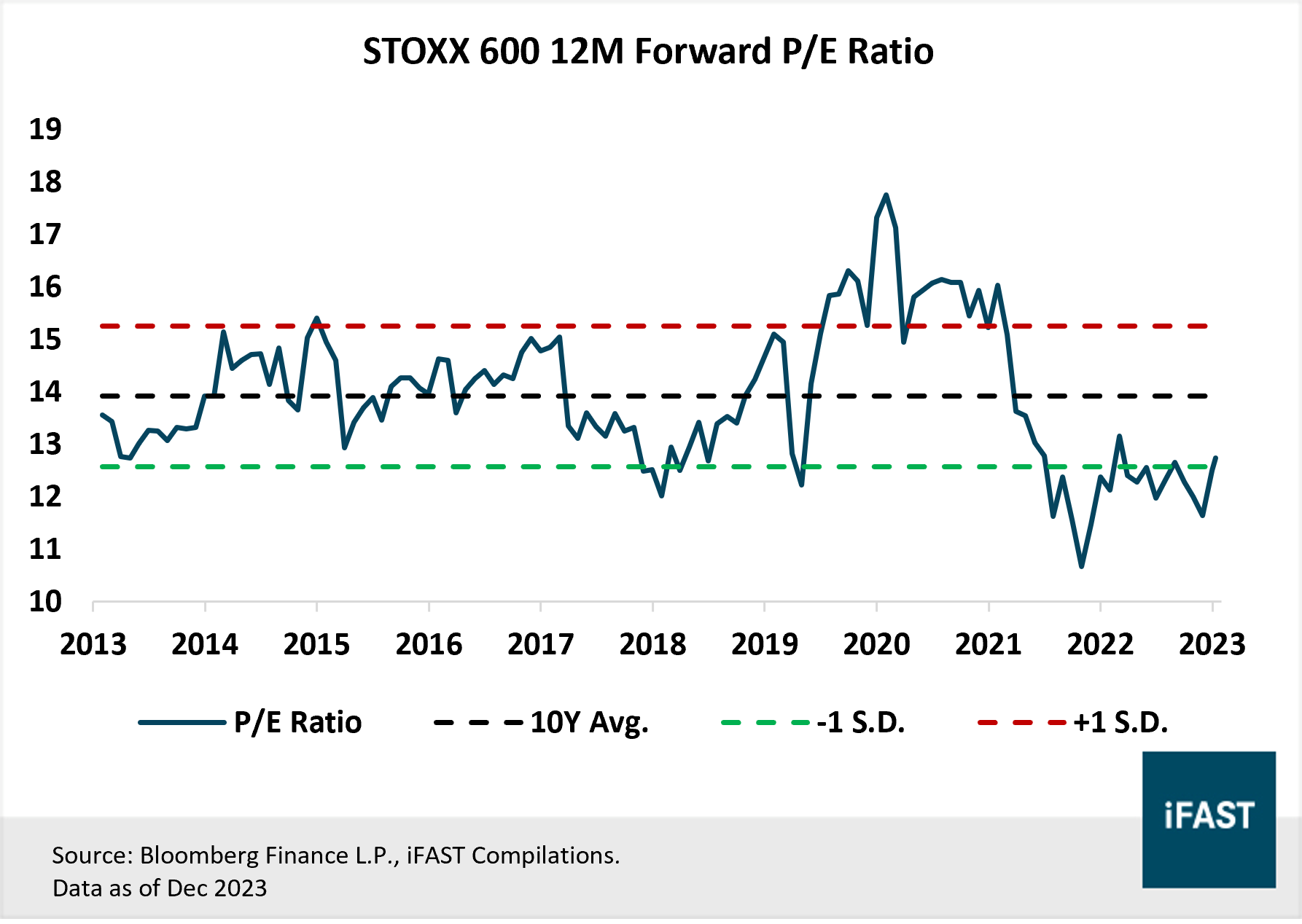

Although valuations are currently trading at a discount to its 10-year historical average (Figure 10), we believe a combination of sticky inflation, restrictive monetary policy, and slowing growth in China paints a gloomy picture for Europe. Moreover, longer-term structural issues make European equities look less attractive compared to its developed market peers.

Figure 10: STOXX 600 is trading at a discount to its historical P/E

With these long-term structural challenges in mind, we believe there is a valid justification to downgrade the fair P/E rating for the STOXX 600 Index from the current 16.5X to 14X. Based on our revised fair P/E ratio of 14X, we project a target price of EUR 553 for the STOXX 600 Index, translating to an upside potential of 15.9% by the end of 2025 (Table 1). We maintain the Star Rating for Europe at 2.5 Stars “Neutral”.

Nevertheless, if investors still wish to seek exposure to European equities, they may consider the Eastspring Investments Unit Trusts - Pan European SGD. They may also consider the Fidelity European Smaller Companies A-EUR, if they wish to seek exposure to small and mid-cap European equities. Alternatively, they can consider a passive ETF such as the Vanguard FTSE Europe ETF (NYSE:VGK).

Beyond Europe, we believe there are more attractive opportunities to be found elsewhere such as Japan and the Asian Tigers. On a sectoral basis over in the US, we prefer high quality companies, Big Tech and the semiconductor sector.

Related articles:

The resurgence of Japan: A new era of multi-year tailwinds with upside potential of 30% by 2025

Chip sales to top 40% year-on-year by 2Q25. Here’s how you can capitalise on this opportunity

The earnings recession is over. Big Tech is set to lead the next phase of growth.

Looking for an ETF to hold for a lifetime? This is it!

The most promising sectors and markets to invest in 2024

Table 1: Projections for STOXX 600 Index

|

Europe (STOXX 600 Index) |

2022 |

2023E |

2024E |

2025E |

|

PE Ratio (X) |

13.6 |

13.1 |

12.7 |

12.1 |

|

Projected Earnings Growth (YoY %) |

29.6% |

4.1% |

3.1% |

5.2% |

|

Projected Earnings Per Share (EPS) |

35.0 |

36.4 |

37.5 |

39.5 |

|

Target Fair Price (Based on a fair PE ratio of 14X) |

- |

- |

- |

553 |

|

Potential Upside (%) |

- |

- |

- |

15.9% |

|

Source: Bloomberg Finance L.P., iFAST Estimates |

||||

Table 2: Recommended products for Europe

|

Unit Trust |

ETF |

|

|

Europe |

||

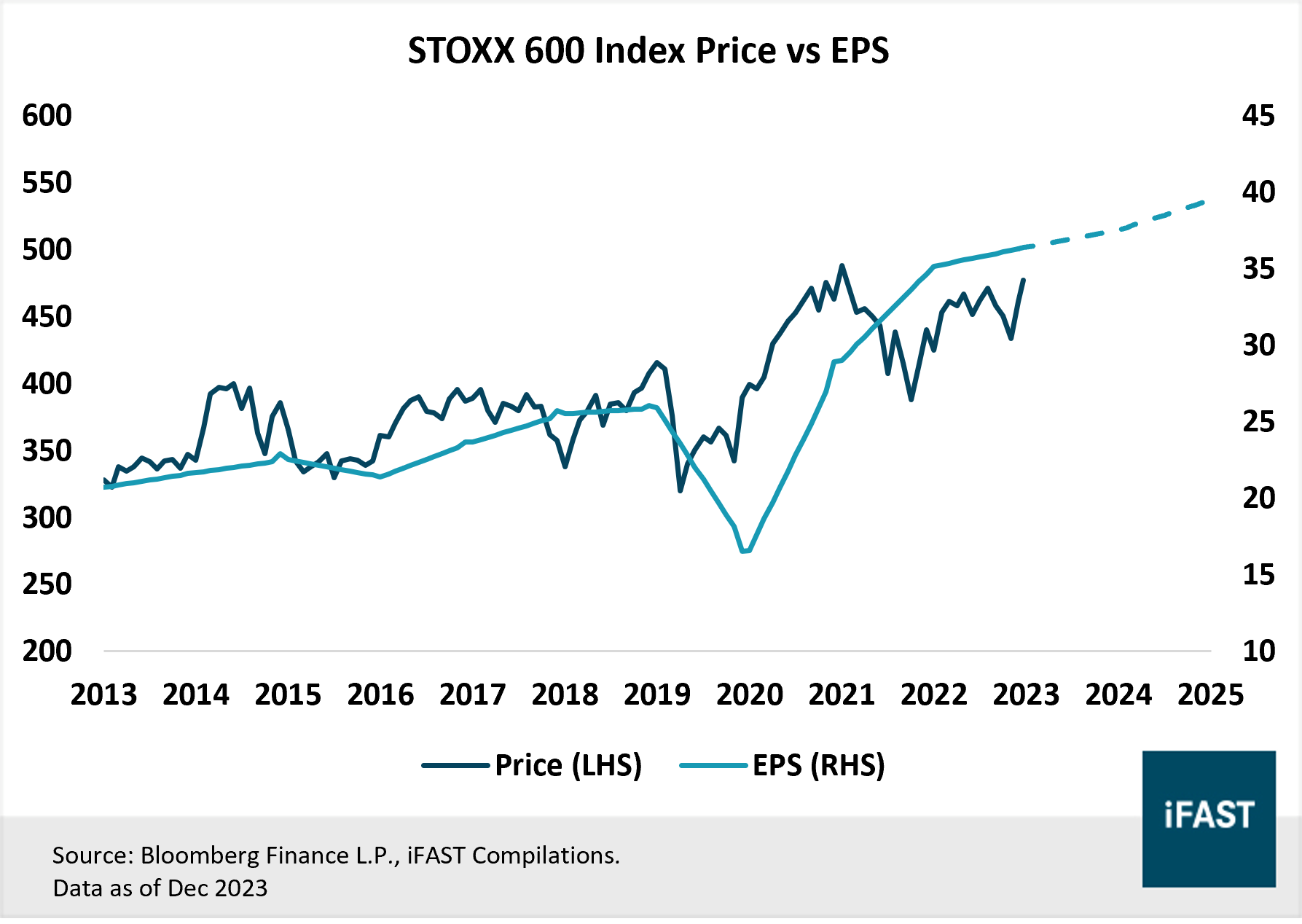

Figure 11: STOXX 600 Index Price vs EPS

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")