' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Fed Delivered the First Rate Cut of 2025 Amid Labour Market Weakness

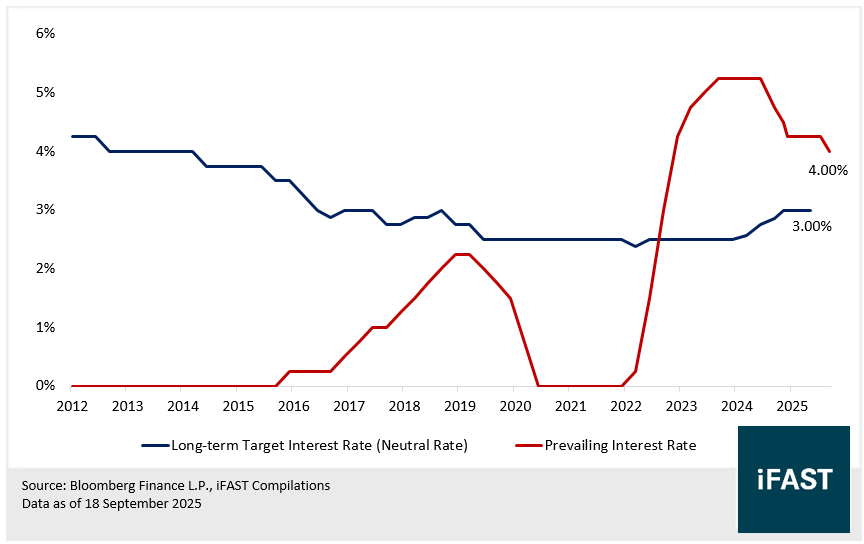

In its September 2025 FOMC meeting, the Federal Reserve lowered the federal funds rate by 25 basis points to a target range of 4.00%–4.25% (see Chart 1). The decision, widely anticipated by markets, marks the first rate cut since December 2024 and reflects growing concerns over slowing economic growth and a weakening labour market.

Chart 1: US Policy Rate (Lower Bound) vs. Estimated Neutral Rate

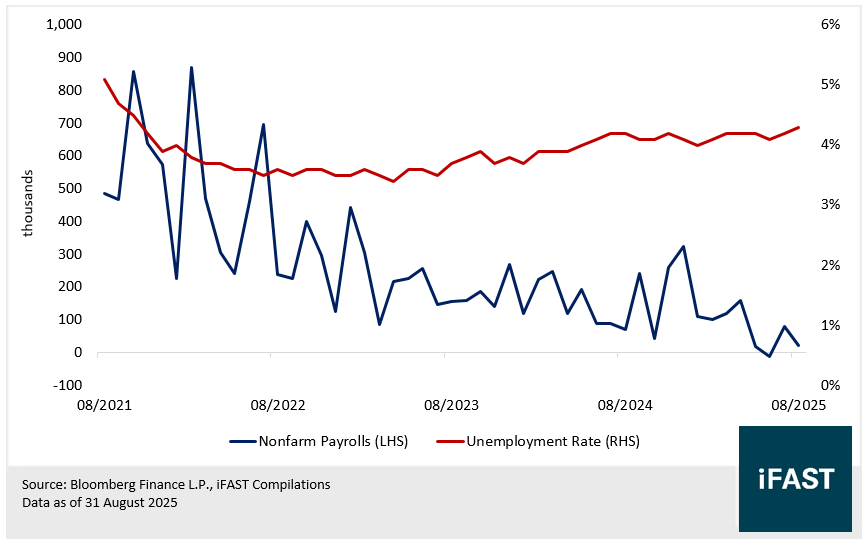

August labour data showed clear signs of softening. The unemployment rate rose to 4.3%, the highest level in nearly two years, while nonfarm payrolls increased by just 22,000—well below July’s 79,000 gain and short of market expectations (see Chart 2).

August labour data showed clear signs of softening. The unemployment rate rose to 4.3%, the highest level in nearly two years, while nonfarm payrolls increased by just 22,000—well below July’s 79,000 gain and short of market expectations (see Chart 2).

Chart 2: US Nonfarm Payroll Growth and Unemployment Rate

Recent substantial revisions to US employment data have drawn heightened market scrutiny and sparked political controversy. The Trump administration dismissed Bureau of Labour Statistics Commissioner Erika McEntarfer, citing “persistent misreporting of job figures” as damaging to government credibility—an action that quickly escalated into a broader political dispute.

Recent substantial revisions to US employment data have drawn heightened market scrutiny and sparked political controversy. The Trump administration dismissed Bureau of Labour Statistics Commissioner Erika McEntarfer, citing “persistent misreporting of job figures” as damaging to government credibility—an action that quickly escalated into a broader political dispute.

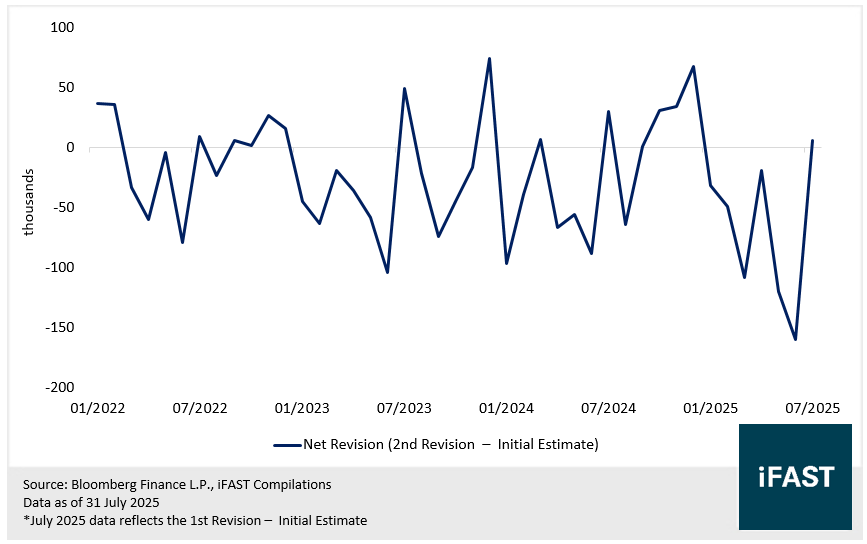

Downward revisions to nonfarm payrolls have become increasingly pronounced. In the first seven months of 2025, monthly job figures were revised down by an average of 68,900—well above historical norms (Table 1). June’s revision was particularly striking, with a downward adjustment of 160,000 jobs—the largest single-month revision since 2020 (see Chart 3), underscoring the fragility of the labour market.

Although core PCE inflation remains elevated at 2.9%, still above the Fed’s 2% target, policymakers have shifted focus toward rising employment risks. The September rate cut was therefore seen as a preemptive move to ease pressure on the economy and labour market.

Table 1: US Nonfarm Payroll Net Revision Mean (2nd Revision – Initial Estimate)

| Net Revision Mean (thousands) | |

| 2025 | -68.9 |

| 2024 | -20.1 |

| 2023 | -30 |

| 2022 | -5.5 |

| Source: Bloomberg Finance L.P., iFAST Compilations Data as of 31 July 2025 | |

Chart 3: US Nonfarm Payroll Net Revision (2nd Revision – Initial Estimate)

Dot Plot Reveals Divergence Among Fed Officials; Rate Path Remains Uncertain

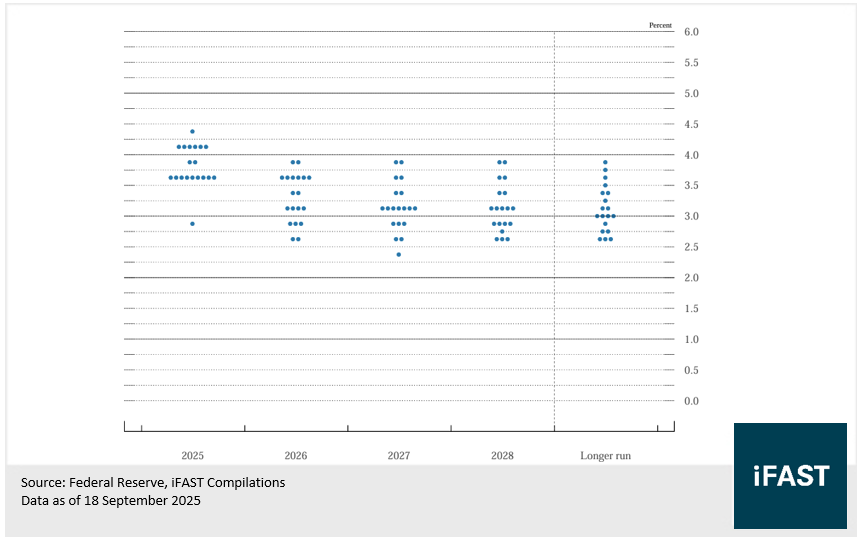

Although the Federal Reserve delivered a widely expected 25-basis-point rate cut at its September meeting, the latest dot plot and accompanying remarks from officials highlight growing divergence within the committee regarding the future path of interest rates—underscoring the high degree of policy uncertainty ahead.

According to the Fed’s updated projections, the median forecast suggests two more rate cuts in 2025, likely in October and December. However, a closer look at the distribution reveals a split view: among the 19 officials, 9 anticipate two additional cuts this year, while another 9 expect at most one more cut—or none at all. Notably, 6 officials project no further easing in 2025.

Looking ahead to year-end 2026, the dispersion is even wider. Officials’ projections range from just one additional cut to as many as six (i.e a target range between 2.50% and 2.75%). This reflects significant differences in views on inflation dynamics and the broader economic outlook (see Chart 4).

Chart 4: Federal Reserve Dot Plot

Notably, the September rate cut was passed with near-unanimous support, with only one dissenting vote from Stephen Miran—a recent appointee by the Trump administration. Miran, who holds a distinctly dovish stance, advocated for a 50-basis-point cut in September and expects as many as five rate cuts in total this year.

Notably, the September rate cut was passed with near-unanimous support, with only one dissenting vote from Stephen Miran—a recent appointee by the Trump administration. Miran, who holds a distinctly dovish stance, advocated for a 50-basis-point cut in September and expects as many as five rate cuts in total this year.

In recent months, President Trump has repeatedly criticized Fed Chair Jerome Powell for his hawkish stance and has openly considered removing him. He also attempted to dismiss Fed Governor Lisa Cook over allegations of mortgage fraud. Although neither action materialized, these developments have raised market concerns about political interference in the Fed’s independence and decision-making autonomy.

Currently, three of the seven sitting governors have been appointed by Trump. With both Powell and Cook facing political pressure, we believe the Fed’s near-term policy decisions may continue to be influenced by external political dynamics.

Market consensus now expects two more rate cuts before year-end, bringing the total to three for 2025. This would lower the federal funds rate to a target range of 3.50%–3.75%.

Powell Mentions Rate Cut as Risk Management; Inflation Pressures May Limit Further Policy Easing

At the post-meeting press conference, Powell stated that the September rate cut was a ‘risk management’ measure aimed at managing recession risks, particularly in response to signs of cooling in the labour market. He reiterated that the Fed has not committed to a preset path of rate cuts, noting that the dot plot merely reflects current expectations. Future policy decisions will remain data-dependent, with the pace of easing contingent on inflation and employment trends.

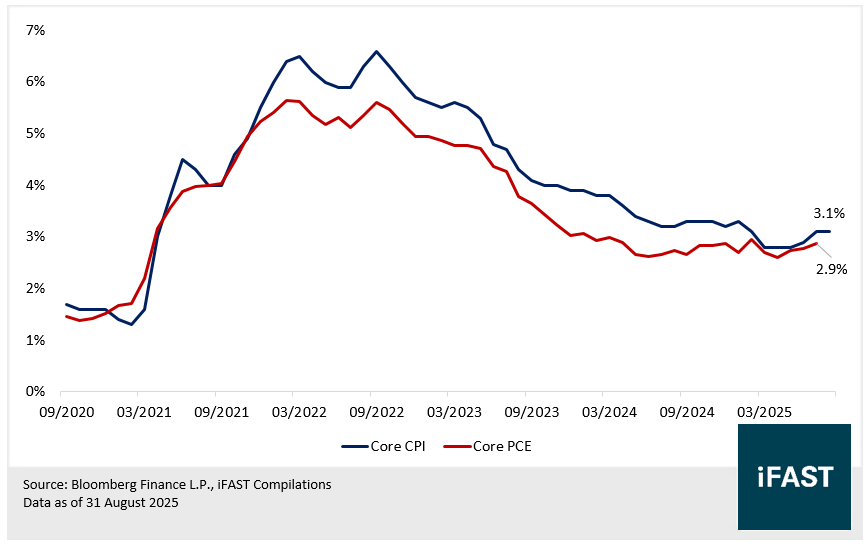

Given that inflation remains the primary driver of long-term policy rates, we believe price dynamics will continue to be the key variable shaping future decisions. According to the latest data, core PCE inflation held steady at 2.9% year-on-year in July—still notably above the Fed’s 2% target ( Chart 5).

Chart 5: US Core CPI and Core PCE Inflation

With new tariffs now in effect and corporate inventory destocking nearing completion, goods prices may once again come under upward pressure, raising the risk of a resurgence in inflation.

With new tariffs now in effect and corporate inventory destocking nearing completion, goods prices may once again come under upward pressure, raising the risk of a resurgence in inflation.

Given the lagged impact of tariffs on actual inflation, and with current price data yet to show clear signs of cooling, we believe the Fed has limited room for aggressive rate cuts. As such, we expect at most one to two additional cuts this year, each by 25 basis points. Unless the employment situation deteriorates significantly, the likelihood of a one-off 50-basis-point cut in either of the remaining two meetings is low.

Our take and recommendations

We continue to prefer short tenor US treasuries. While the ultra-long-end portion (10-year onwards) of the US treasury curve has steepened in recent months, we still see little incentive to extend duration significantly.

Apart from US Treasuries, investors can consider various Unit Trusts depending on their investment styles and duration preferences (Table 2). For instance, there are money market and ultra-short-duration bond funds, typically with 0.5 years duration or less – their underlying holdings tend to be on the front-end, where yields tend to be among the highest due to the current inverted curve.

There are also short-duration bond funds (closer to about 1 to 2 years duration) that are comfortable with a little more duration risk. Funds here typically have the flexibility to invest in bonds of different duration profiles (both short and long) as long as the average duration remains in the pre-specified target range, and the best managers can generate consistent alpha through said duration management and credit selection.

Finally, we also recommend several global bond funds. While these usually come with more duration risks than the average money market fund, managers here may have the flexibility to invest in many different markets and credits, allowing them to display their skill in credit selection. The funds we chose below have durations closer to around 3 or 5 years, longer than the other funds listed below, but nonetheless not too excessive (e.g. not yet approaching 10 years).

Table 2: Fund recommendations (short and medium-duration funds)

| Type of Product | Product |

| Money Market Fund (USD) | Amundi Funds Cash USD |

| Ultra Short-Duration Bond Fund | HGIF - Ultra Short Duration Bond Fund |

| Short-Duration Bond Fund | Amova Short Term Bond Fund |

| Short-Duration Bond Fund | United SGD Fund |

| Global Bond Fund | PIMCO Income Fund |

| Global Bond Fund (Alternative) | T. Rowe Price Funds SICAV - Diversified Income Bond |

| Source: iFAST compilations. | |

Declaration:

For specific disclosure, at the time of publication of this report, the analyst who produced this report holds a NIL position in the abovementioned securities. IFPL (via its connected and associated entities) holds positions in T 4.250% 31Dec2025 Govt (USD), T 0.375% 31Jan2026 Govt (USD), T 4.000% 15Feb2026 Govt (USD), T 2.125% 31May2026 Govt (USD), and T 1.500% 15Aug2026 Govt (USD).

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")