' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

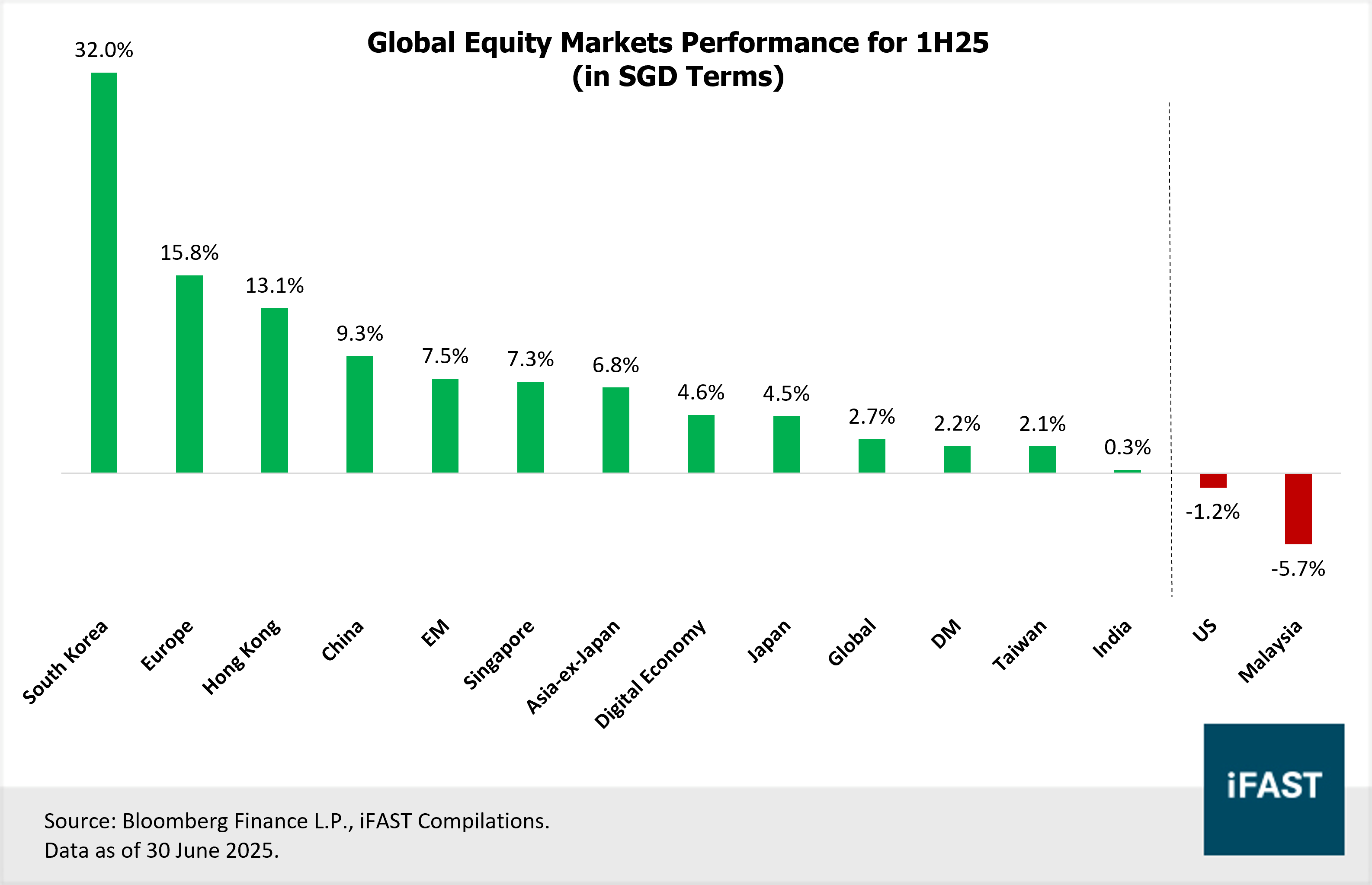

Market Recap 1H25

Most global equity markets ended the first half of 2025 in positive territory, despite the volatility triggered by US President Trump’s tariff policies. Global equities, measured by the MSCI AC World Index, rose a modest 2.7%. Notably, emerging markets outperformed developed markets—a reversal from the trend seen in 2024.

South Korea led market performance among our coverage, with the KOSPI Index surging 32.0% in the first half of the year. The rally was driven by renewed investor optimism following the inauguration of President Lee Jae-myung, whose leadership helped restore political stability and raised expectations for economic stimulus and corporate reform. European equities followed with a strong 15.8% gain. The rally was supported by robust corporate earnings, interest rate cuts by the European Central Bank (ECB), and increased fiscal spending, particularly in defence. China and Hong Kong markets also posted solid returns, rising 9.3% and 13.1% respectively. Sentiment was lifted by the government’s ongoing efforts to revitalise the private sector, with investor interest particularly strong in technology-related names.

In contrast, Malaysia was the worst-performing market in our coverage, declining by 5.7%. The market was weighed down by weaker-than-expected corporate earnings and mounting global trade uncertainties, which dampened investor sentiment. Additionally, US equities declined by 1.2% in the first half of the year. Investor confidence was dented by unpredictable policy decisions under President Trump, with lingering concerns over elevated inflation risks and their broader implications for US economic growth. The weaker US dollar against the Singapore dollar further dragged on returns (all performance figures are in SGD terms, unless otherwise stated).

Figure 1: Performances of major markets ranked for 1H25

Top Performing Equity Funds of 1H25

Among the top-performing equity funds in the first half of 2025, gold funds led the charge, claiming five of the top ten spots. The yellow metal, long regarded as a safe-haven asset, saw surging demand amid escalating global trade tensions, geopolitical instability in the Middle East, and a downgrade of the US credit rating. These factors weakened the appeal of the US dollar and spurred a flight to tangible hedges such as gold. A standout performer was the Schroder ISF Global Gold A Acc EUR-H, which delivered a remarkable return of 64.9%. The fund’s strong performance was further boosted by its currency-hedged EUR share class, which benefited from the significant appreciation of the euro against the US dollar during the period. The euro’s gain against the Singapore dollar also supported returns when measured in SGD terms.

Korean equity funds also posted exceptional results in 1H25. The LionGlobal Korea Fund SGD returned 43.3%, while the JPMorgan Funds – Korea Equity A (acc) USD gained 35.4%. Both funds benefited from concentrated exposure to leading semiconductor names such as SK Hynix and Samsung Electronics, which rose 74.0% and 14.0%, respectively. LionGlobal’s outperformance was further bolstered by its sizable allocation to the industrials sector, particularly Hanwha Aerospace, which soared 139.7% on the back of surging defence equipment exports to the Middle East and Europe.

Another notable outperformer was the BNY Mellon Global Infrastructure Income J Inc SGD-H, which returned 29.0% in the first half of 2025. The infrastructure sector’s domestic orientation and relatively low economic sensitivity, combined with structural demand for electricity, driven largely by the rapid expansion of data centres, helped the fund outperform. One of the fund’s key holdings, French energy company Engie, saw its share price surge by 50.2%, while other utility companies such as Enel SpA and Fortum Oyj also posted strong gains of 27.8% and 37.0%, respectively (all performance figures are in SGD terms, unless otherwise stated).

Table 1: Top Performing Equity Funds of 1H25

|

Fund name |

1H25 (%) |

Segment |

|

Schroder ISF Global Gold A Acc EUR-H |

64.9 |

Gold & Precious Metals Equity |

|

FTIF - Franklin Gold and Precious Metals A (acc) USD |

53.1 |

Gold & Precious Metals Equity |

|

Blackrock World Gold Fund A2 SGD-H |

47.9 |

Gold & Precious Metals Equity |

|

Ninety One Global Strategy Fund - Global Gold A Acc SGD |

44.9 |

Gold & Precious Metals Equity |

|

LionGlobal Korea Fund SGD |

43.3 |

Korea Equity |

|

JPMorgan Funds - Korea Equity A (acc) USD |

35.4 |

Korea Equity |

|

United Gold and General A Acc SGD |

34.4 |

Gold & Precious Metals Equity |

|

Blackrock Latin American A2 SGD-H |

33.5 |

Latin America Equity |

|

Fidelity Italy A-EUR |

29.5 |

Italy Equity |

|

BNY Mellon Global Infrastructure Income J Inc SGD-H |

29.0 |

Global Infrastructure Equity |

|

Total returns basis in SGD terms. Source: iFAST Compilations. Data as of 30 June 2025. |

||

Bottom Performing Equity Funds of 1H25

Despite the overall resilience in emerging markets, ASEAN equity funds underperformed, with Thailand funds faring the worst. The abrdn Thailand Equity SGD posted the steepest loss of 23.1%. The Thai market was weighed down by escalating political tensions, including a dispute with Cambodia and a leaked phone call suggesting that the Pheu Thai leadership prioritised personal affiliations with Cambodia over national interests, eroding investor confidence in the government. Weak economic momentum, particularly in the tourism sector, added to the pressure. Key tourism-related stocks such as Minor International and Airports of Thailand fell sharply, by 10.9% and 49.9% respectively.

Indonesia was another notable underperformer, both within ASEAN and on the global stage. The abrdn Indonesia Equity SGD and Fidelity Indonesia A-USD declined 14.0% and 12.8%, respectively, in the first half of the year. Markets reacted negatively to President Prabowo’s fiscal policies, which raised concerns over budget sustainability and central bank independence, casting doubt over the country’s economic outlook. The Indonesian rupiah also depreciated to record low, further eroding fund returns in SGD terms.

Outside of ASEAN, a notable underperformer was the FTGF Royce US Smaller Companies A Acc USD, which declined 13.3%. US equities lagged global peers, with small-cap stocks underperforming large caps amid rising concerns over potential slowing growth and persistent inflationary pressures. The fund’s performance was further weighed down by its heavy exposure to industrials and healthcare sectors that are particularly vulnerable to renewed tariff pressures and disruptions of supply chains (all performance figures are in SGD terms, unless otherwise stated).

Table 2: Bottom Performing Equity Funds of 1H25

|

Fund name |

1H25 (%) |

Segment |

|

abrdn Thailand Equity SGD |

-23.1 |

Thailand Equity |

|

Fidelity Thailand A-USD |

-19.4 |

Thailand Equity |

|

LionGlobal Thailand SGD |

-17.3 |

Thailand Equity |

|

CPR Invest - Global Silver Age A2 Acc USD-H |

-15.5 |

Global Equity |

|

CPR Invest - Global Disruptive Opportunities A2 Acc USD-H |

-14.6 |

Global Technology Equity |

|

HGIF - Turkey Equity Fund CL AD SGD |

-14.1 |

Turkey Equity |

|

abrdn Indonesia Equity SGD |

-14.0 |

Indonesia Equity |

|

FTGF Royce US Smaller Companies A Acc USD |

-13.3 |

US Small to Medium Companies Equity |

|

Fidelity Indonesia A-USD |

-12.8 |

Indonesia Equity |

|

United Vietnam Equity A1 Acc USD |

-12.4 |

Vietnam Equity |

|

Total returns basis in SGD terms. Source: iFAST Compilations. Data as of 30 June 2025. |

||

Final thoughts

As we enter the second half of 2025, investors continue to navigate a highly uncertain landscape. Over the past three months, President Trump has concluded just three trade deals and is now preparing to reimpose tariffs on all trading partners effective 1 August 2025. In addition, a 50% levy on copper has already been enacted, with potential new measures targeting the semiconductor and pharmaceutical sectors.

The outlook for 2H25 is increasingly fraught with growing risks that the economic fallout from these trade actions will begin to materialise more meaningfully. While US equities remain a core component of our asset allocation, their relative appeal has diminished. Should tariffs be fully reinstated, the risk of stagflation could significantly impact corporate margins and economic momentum.

Against this backdrop, we advocate a selective approach within US markets, focusing on high-quality companies, particularly in the digital economy and semiconductor sectors, which are better positioned to withstand volatility and continue delivering structural growth.

At the same time, diversification is becoming increasingly critical. The strong performance of non-US markets in 1H25 reinforces our view that global opportunities should not be overlooked in the second half of the year.

Japanese equities deserve a long-term strategic allocation, supported by the country’s shift toward monetary policy normalisation, a renewed focus on reclaiming leadership in semiconductors, and ongoing structural reforms aimed at enhancing capital efficiency and shareholder returns.

Chinese equities are also gaining traction, underpinned by sustained policy support for the private sector. Economic indicators point to a gradually improving outlook, with rising consumer sentiment and accelerating growth momentum. We believe technology stocks will lead the next leg of China’s recovery, driven by both the AI revolution and the country’s transition toward a consumption-led economy.

Meanwhile, European equities are becoming more attractive, particularly in the defence and infrastructure sectors. ECB rate cuts and a large-scale fiscal stimulus package from Germany are expected to provide a strong tailwind for corporate earnings and overall market performance.

Related article:

A new world order is here. Is your portfolio ready?

US exceptionalism under pressure, but far from over

Upgrade China to 3.0 Stars 'Attractive' Rating Amid Private Sector Resurgence

European defence stocks rally amid growing transatlantic divide: A paradigm shift?

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")