' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

- Year to date, financial companies have been the best performers among the constituents of Japan’s Nikkei 225 Index following all-time high earnings from the Bank of Japan’s interest rate hikes.

- We believe Japan is no longer a market to overlook given improving fundamentals and economic normalisation, including sustainable inflation and strong wage growth.

- Corporate reforms promoting capital efficiency are leading to increased shareholder returns through higher dividends and a surge in share buybacks.

- We find the renaissance in Japan’s semiconductor industry encouraging. This will have positive spillovers to not just the economy, but also the stock market.

- We anticipate continued support for corporate earnings growth. Our target price for the Nikkei 225 Index is 48,000, representing a potential upside of 22%. Japan should be a strategic long-term component in portfolios.

Year to date, financial companies have been the best performers among the constituents of Japan’s Nikkei 225 Index, driven by a set of positive earnings release. With robust lending demand and higher net interest margins following the Bank of Japan’s (BOJ) interest rate hikes, the nation’s three megabanks reported all-time high earnings this year.

Figure 1: Breakdown of the Nikkei 225’s performance by sectors

Top Japanese companies also reported a strong set of results in the latest earnings season. For instance, Fast Retailing, the parent company of Uniqlo, delivered a record-high performance thanks to its robust global expansion strategy. Meanwhile, the world’s biggest supplier of chip testing equipment Advantest raised its earnings guidance on the back of robust AI-related demand.

Table 1: Top 10 constituents of the Nikkei 225

|

Name |

Sector |

Weight |

YTD Total Return |

|

Fast Retailing |

Consumer Discretionary |

11.9% |

47.4% |

|

Tokyo Electron |

Information Technology |

6.0% |

-6.2% |

|

Advantest |

Information Technology |

5.7% |

72.7% |

|

Softbank |

Communication Services |

4.6% |

42.7% |

|

Recruit Holdings |

Industrials |

2.7% |

74.7% |

|

KDDI Corp |

Communication Services |

2.6% |

13.7% |

|

TDK Corp |

Technology |

2.5% |

45.8% |

|

Shin Etsu Chemical |

Materials |

2.4% |

-4.6% |

|

Terumo Corp |

Health Care |

2.1% |

33.2% |

|

Chugai Pharmaceutical |

Health Care |

1.7% |

24.4% |

|

Total |

- |

42.2% |

- |

|

Source: Nikkei, Bloomberg Finance L.P., iFAST Compilations Data as of 30 November 2024 |

|||

Japan warrants a strategic allocation in your portfolio

The megabanks’ record results highlight how Japan is evolving beyond the shadows of the Lost Decade. Years of negative interest rates kept lending margins razor-thin, while deflation and economic stagnation stifled stock market growth. This left many foreign investors underexposed to Japanese equities, missing out on the country's long-awaited resurgence.

Today, we believe Japan deserves a long-term strategic allocation within investors’ portfolios. This is no longer a market to overlook – improving fundamentals and ongoing economic normalisation make Japan a compelling investment destination for those seeking growth and diversification.

For a start, the economy is undergoing a period of structural transformation from deflation to inflation. Core CPI has remained above the BOJ’s 2% target for over two years now, with the November inflation print rising 2.9% from a year earlier. Additionally, the inflation cycle which lagged behind the rest of the world for decades, has now caught up. In fact, inflation in Japan is already on par with other major economies like the US and the EU (Figure 2).

Figure 2: Japan’s inflation against US and EU

With inflation taking hold, companies are finally addressing the decades-long issues of sluggish wage growth. Japan’s largest labour union group Rengo has announced it will seek wage hikes of at least 5% in 2025, building on this year's hefty increase (Figure 3). Rengo is also prioritising smaller firms – where most of Japan’s workforce is employed – by targeting a wage increase of at least 6%. This will help narrow the income gap with workers at large companies. Similarly, UA Zensen – another major union group – has set its sights on a bump of 6% in overall wages.

Figure 3: Strong wage growth momentum to continue into 2025

A tight labour market, coupled with an ageing population, is paving the way for a structural rise in wages. Continued wage hikes would strengthen real wages, giving households greater purchasing power and helping to drive a virtuous cycle of rising wages and prices. These dynamics not only create a foundation for economic resilience but also lay the groundwork for growth in corporate earnings.

Furthermore, Japan's path to economic normalisation remains firmly on track, even after the Liberal Democratic Party’s (LDP) failure to secure a majority in parliament during the general elections. There is broad consensus among political parties on the necessity for Japan to pursue pro-growth and market-friendly policies. Notably, there may be more expansionary fiscal policies as opposition parties are campaigning for tax cuts aimed at bolstering household income and driving economic expansion.

Corporate reforms are enhancing shareholder value

Another factor fostering Japan’s environment conducive to growth is corporate reforms aimed at promoting capital efficiency and shareholder returns.

For years, Japanese companies faced criticism for their conservative financial practices such as hoarding cash and keeping dividend payouts low. These methods were perceived as prioritising stability over growth, often at the expense of shareholder interests.

Since the Tokyo Stock Exchange’s call for higher capital efficiency last year, companies are encouraged to use resources more effectively, whether through reinvestments, share buybacks, or higher dividend payouts. This initiative is gaining significant momentum, with 89% of companies (as of 30 November 2024) listed on the Prime section of the Tokyo Stock Exchange responding to calls to enhance capital efficiency. Meanwhile, companies that have yet to comply are publicly named and shamed.

An example of a company that has disclosed plans to improve their capital efficiency is Obayashi Corp, one of Japan’s leading construction companies. Obayashi has raised its dividend on equity (DOE) ratio target – a measurement of how much of a company’s profits are being returned to shareholders – from 3% to 5%. It is also exploring additional avenues like special dividends and share buybacks to reward investors.

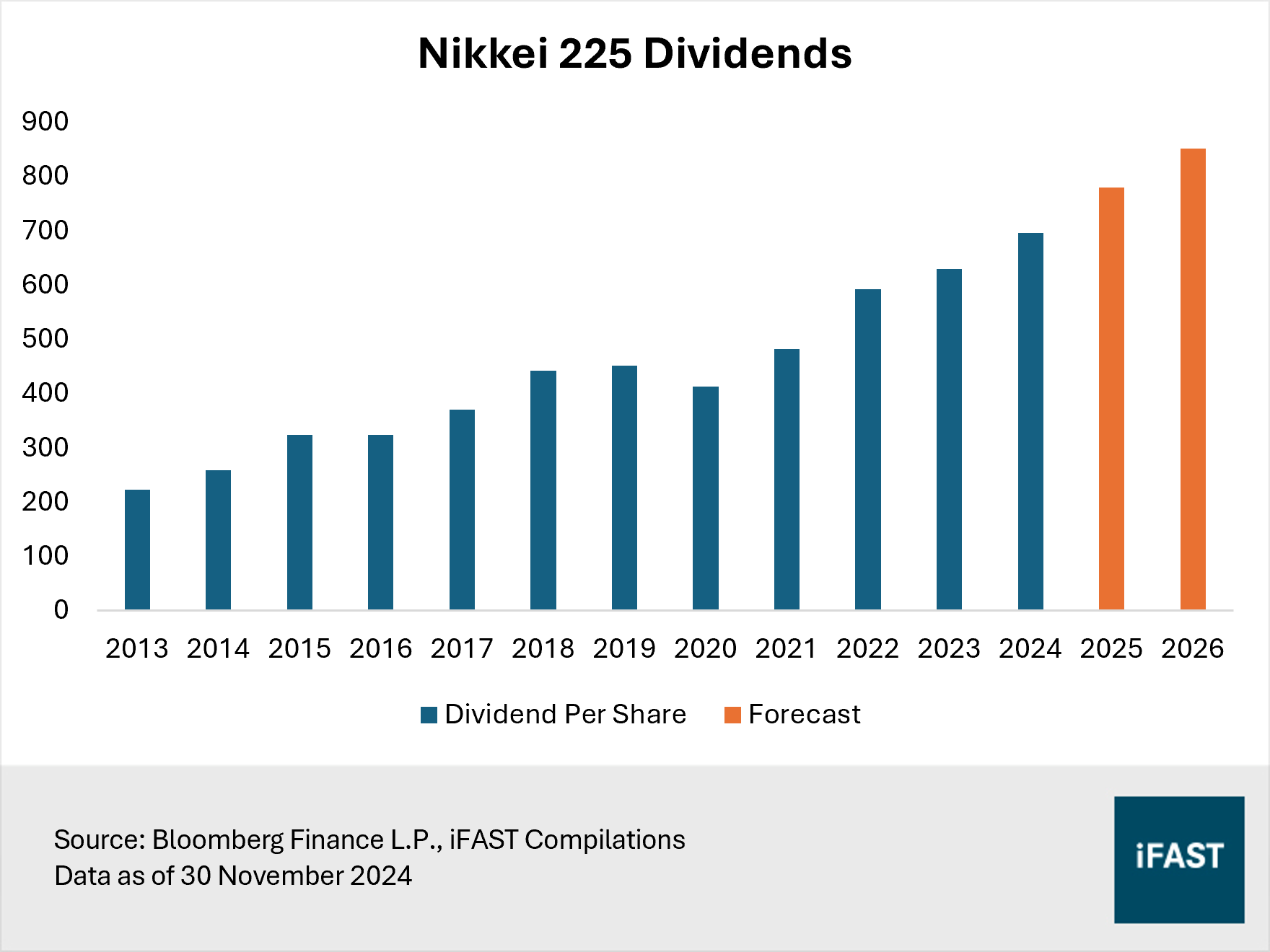

These efforts are part of a broader trend driving Japan’s equity market. Dividends handed out are climbing steadily, with an estimated payout ratio of 40% (Figure 4). Complementing dividend growth is the surge in share buybacks, which have reached record levels this year. According to data from Nikkei, Japanese listed companies allocated approximately JPY 10.65 trillion to buy back shares from April to September, including for future buybacks. This was nearly double the previous record of JPY 5.5 trillion in the same period last year. The biggest buybacks year to date have come from the likes of Toyota, Recruit Holdings, and Mitsubishi UFJ Financial Group (Figure 5).

As companies continue to prioritise capital efficiency, we expect the momentum in share buybacks and dividend growth to accelerate further, reinforcing Japan’s transformation into a market of rising shareholder returns.

Figure 4: Japanese companies are paying out higher dividends

Figure 5: Top 10 stock buybacks in Japan this year

Another notable trend is the reduction of cross shareholdings, a practice unique to Japan where companies take strategic stakes in each other to fend off hostile takeovers. To improve governance and better allocate capital, companies have been urged to reduce their stakes in one another. The results are starting to show, in the Japanese banks for example. The nation’s top three banks have raked in trillions of yen combined from selling off cross-shareholdings (Figure 6). Coupled with record earnings, the banks are now flushed with cash. Besides buybacks and higher dividends, they are seeking to deploy their excess capital in overseas expansion that could deliver the next leg of growth.

Figure 6: The megabanks have stepped up the unwinding of cross-shareholdings this year

With cross-shareholdings being sold off, companies have also been told they should give serious consideration to credible buyout offers. Seven & i Holdings' impressive share price surge of up to 38% this year following a buyout offer is a testament to the potential of these reforms to unlock significant value for investors. This kind of buyout offer, once deemed implausible years ago, is now becoming a reality. As more companies adopt a mindset of greater openness and accountability, Japan’s equity market is poised for a revitalisation.

Chip renaissance

Besides corporate governance reforms and economic normalisation, we find the renaissance in Japan’s semiconductor industry encouraging. Before Japan lost ground to competitors like Taiwan and South Korea, its semiconductor manufacturers dominated the global stage in the 1980s, contributing to over 50% of world production.

Prime Minister Ishiba has recently pledged an extra JPY 10 trillion of fresh support to the semiconductor and AI sector. This comes on top of the JPY 3.9 trillion invested since 2021, underscoring Japan’s commitment to reclaims its place as a global chip leader. Investments into chips represent about 1% of Japan’s GDP, a share that is substantially higher than other developed countries. As subsidies are handed out to companies, it has attracted top players like TSMC and Micron to manufacture chips in Japan. In particular, Japan is gunning for TSMC to build its third fab in the country that would make advanced three-nanometre chips.

At the heart of Japan’s push to become a semiconductor leader also lies Rapidus – a homegrown chipmaker established by the government together with major Japanese corporations and IBM to produce two-nanometre chips used for AI by 2027. While the goal is undeniably ambitious, Japan’s expertise in advanced manufacturing, its dominance in semiconductor tools and equipment, and the global realignment of chip production could make this vision well within reach. Adding fuel to this momentum, the government has pledged an additional JPY 200 billion to Rapidus for the fiscal year starting April 2025, underscoring its commitment to achieving this milestone.

There will be positive spillovers of Japan’s semiconductor resurgence to not just the economy, but also the stock market. Established giants like Advantest, Tokyo Electron, and Disco Corp, which dominate the semiconductor equipment space, are primed to benefit. Meanwhile, Japan’s chip revival has already led to the successful listing of memory chipmaker Kioxia on the Tokyo Stock Exchange on 18 December 2024. Valued at JPY 784 billion, Kioxia’s IPO is not only one of the largest in Japan this year but will also provide the company with the resources needed to ramp up capacity and remain competitive in the capital-intensive memory chip market.

Key investment risks

Trump tariffs: A second Trump administration could pose challenges for Japanese exporters, given the president-elect’s proposed 10% to 20% tariffs on all foreign goods, including those from Japan. However, Trump’s tariff threats often serve as negotiation tactics. Japan’s foreign minister Takeshi Iwaya has expressed intention to pick up trade talks, and history suggests a trade deal, like the one struck during Trump’s previous term, could help Japan avoid additional tariffs.

Pressure to restrict chip exports to China: The US, a close ally of Japan, has consistently taken a tough stance on China’s access to advanced chips. While Japanese-made chip equipment is currently exempt from export curbs, mounting pressure to limit chip exports to China poses a potential challenge for companies like Tokyo Electron, which rely heavily on the Chinese market. However, as revenue from China gradually declines, robust global AI demand could help offset the risks associated with export restrictions.

Ageing population: Japan, with 30% of its population aged 65 or older and a record-low fertility rate, faces demographic challenges that could hinder growth. However, its highly skilled workforce, history of technological innovation, and advanced manufacturing capabilities, combined with economic reforms and opportunities from global supply chain shifts, provide a strong foundation to reclaim its status as an economic powerhouse.

2025 is the year to stay bullish on Japan

In a nutshell, we find compelling reasons to remain bullish on Japan. The shift toward sustainable inflation and solid wage growth is expected to drive economic strength, while corporate reforms unlocking investor value make Japanese equities increasingly attractive on a global scale. Coupled with Japan's potential to re-emerge as a global semiconductor powerhouse, these structural factors could set the stage for a multi-year stock rally.

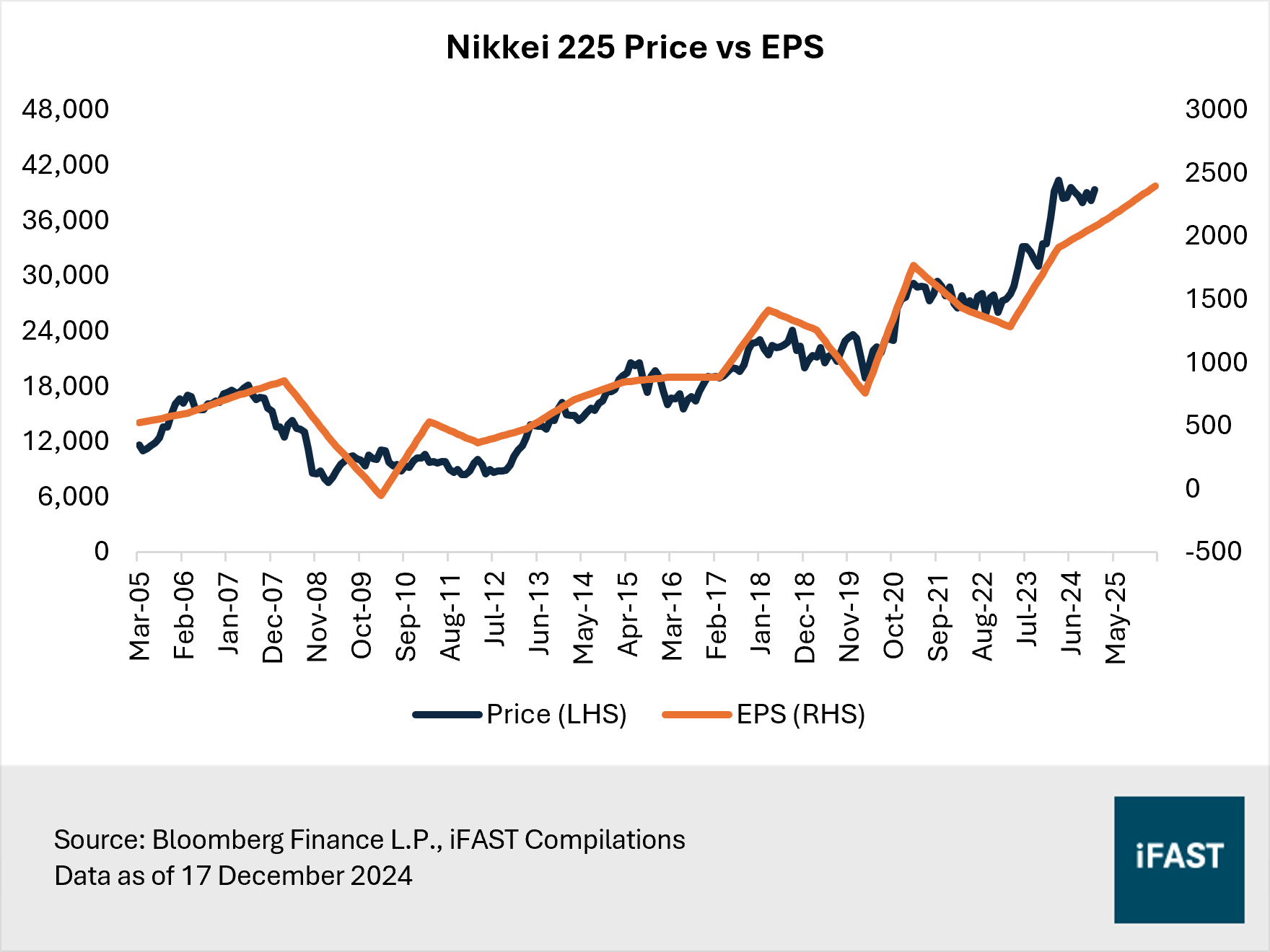

While the Japanese yen could potentially strengthen, we anticipate corporate earnings of export-oriented companies to remain well-supported by their global competitiveness and alignment with key megatrends like digitalisation. In particular, the IT sector – the largest in the Nikkei 225 – is positioned to lead earnings growth, driven by leading semiconductor firms like Tokyo Electron and Advantest which are riding on the tailwinds of AI.

We maintain our target price of 48,000 for the Nikkei 225 Index which translates into an upside potential of 22% as of 17 December 2024. The aftermath of the Lost Decades may have left many foreign investors to be underexposed to Japanese equities. However, Japan's structural story is changing for the better. This is the time to consider increasing strategic long-term allocations to Japan.

Our recommended products to gain access to Japan’s equity market are the Xtrackers Nikkei 225 UCITS ETF 1D (LSE:XDJP) and the Eastspring Investments - Japan Dynamic AS SGD.

(Related article: Why we’re staying bullish on the Japanese Yen in 2025)

Table 2: Projections for Nikkei 225 Index

|

Nikkei 225 Index |

FY2023 |

FY2024 |

FY2025 |

FY2026 |

|

Earnings Per Share |

1,287 |

1,914 |

2,135 |

2,400 |

|

Earnings Growth YoY |

-11.6% |

48.7% |

11.5% |

12.4% |

|

PE Ratio |

21.8 |

21.1 |

18.4 |

16.4 |

|

Upside Potential (based on a fair PE ratio of 20X) |

22% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 17 December 2024 |

||||

Figure 7: Share price vs EPS chart for the Nikkei 225 Index

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")