' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

The local banks are in the spotlight as the US Central Bank hinted that it may proceed with an interest rate cut this September.

This earnings season has seen DBS Group (SGX: D05), United Overseas Bank (SGX: U11), or UOB, and OCBC Ltd (SGX: O39) releasing strong sets of earnings as high interest rates buoy their net interest income.

Investors may be wondering which of these blue-chip banks stand the best chance of doing well should interest rates fall.

Let’s go through several attributes to compare the trio and arrive at a conclusion as to which makes the most compelling choice for your portfolio.

Financial performance

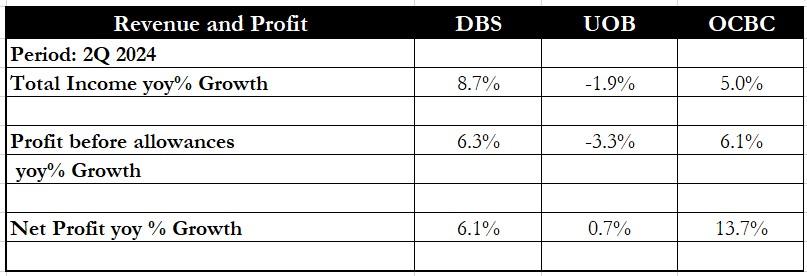

Source: DBS, UOB and OCBC Earnings Reports

With all three banks having reported their second quarter of 2024 (2Q 2024) earnings, we compare how each bank did for total income, profit before allowances, and net profit.

It was a mixed result as DBS logged the best year-on-year increase in total income with an 8.7% rise.

OCBC came in second with a 5% year-on-year increase in total income to S$3.6 billion for the quarter.

Looking at the profit before allowances, both DBS and OCBC were neck and neck with a 6%+ year-on-year increase.

OCBC came out tops when it came to net profit as the lender saw a 43% year-on-year decline in allowances.

DBS, on the other hand, recorded a general provision of S$51 million for 2Q 2024 compared to a write-back of provisions of S$42 million in the prior year.

As a result, OCBC chalked up an impressive 13.7% year-on-year increase in net profit to S$1.9 billion.

Winner: OCBC

Net interest margins and loan growth

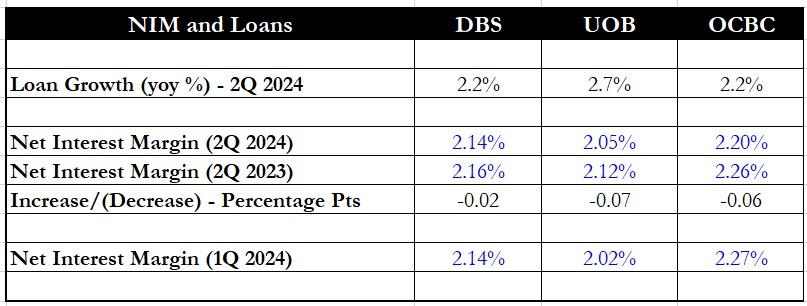

Source: DBS, UOB and OCBC Earnings Reports

Next, we move on to each bank’s net interest margin (NIM) and scrutinise the loan book.

UOB tops the list with a year-on-year increase of 2.7% for its loan book.

However, UOB has the lowest NIM of the three banks at 2.05% for 2Q 2024.

OCBC is the winner when it comes to NIM as it boasts the highest NIM for not just 2Q 2024, but also 2Q 2023 and the previous quarter (1Q 2024).

However, investors should note that DBS saw the gentlest year-on-year decline in its NIM of just 0.02 percentage points compared with its peers.

Winner: OCBC

Cost-to-income ratio (CIR)

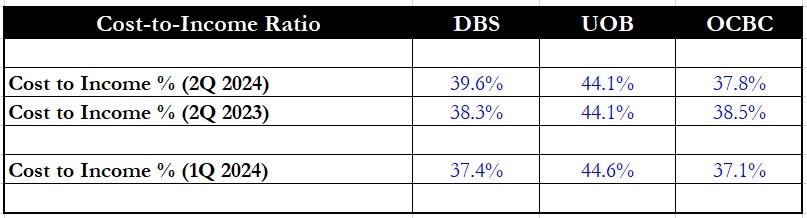

Source: DBS, UOB and OCBC Earnings Reports

The next attribute we are comparing is each bank’s cost-to-income ratio or CIR.

A lower CIR implies that the bank is more efficient at running its business as its expenses are a lower proportion of its total income.

Again, OCBC is the winner with a CIR of just 37.8% for 2Q 2024. OCBC continued to maintain a low CIR quarter-on-quarter with CIR rising by just 0.07 percentage points.

Although DBS had a fairly low CIR in 1Q 2024, Singapore’s largest bank saw its CIR jump by 2.2 percentage points to 39.6% in the current quarter.

Winner: OCBC

Non-performing loans (NPL) ratio

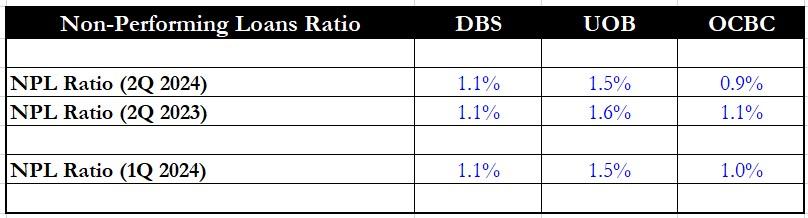

Source: DBS, UOB and OCBC Earnings Reports

We move on to the non-performing loans (NPL) ratio next.

OCBC has not only the lowest NPL ratio of the three banks at 0.9% but also saw a year-on-year improvement of 0.2 percentage points, making it the clear winner.

Winner: OCBC

Dividend yield

Source: DBS, UOB and OCBC Earnings Reports

This next attribute, dividend yield, should be a favourite with income investors.

With all three banks declaring a dividend for the first half of 2024, we compared each lender’s trailing 12-month dividend yield.

Both DBS and OCBC are tied for this attribute with a 6% trailing dividend yield.

However, investors should note that DBS pays out a quarterly dividend compared to half-yearly for the other two banks.

At the current rate of S$0.54 per share, the annualised dividend for DBS is S$2.16, which gives the bank a forward dividend yield of 6.4%.

Winner: DBS

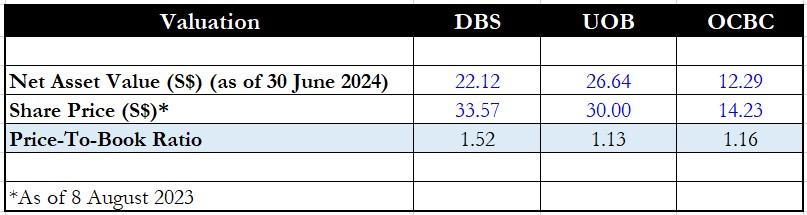

Valuation

Source: DBS, UOB and OCBC Earnings Reports

Finally, we look at each bank’s valuation to determine which offers the most value.

UOB has the lowest valuation of the three banks with OCBC coming in at a close second, based on each bank’s latest price-to-book ratio.

DBS is the most expensive of the trio with a price-to-book ratio of more than 1.5 times.

Winner: UOB

Get Smart: OCBC wins hands down

OCBC wins by ticking off most of the attributes listed here.

Not only did the lender chalk up the best year-on-year profit increase, but it also boasted the highest NIM and the lowest CIR.

Investors can also enjoy a 6% trailing dividend yield if they purchase shares of OCBC and its valuation remains undemanding at just 1.16 times price-to-book.

However, income investors who prefer to receive quarterly dividends should look favourably on DBS as it is the only bank out of the three to pay dividends every three months.

If you’re looking to buy the next S$100 billion stock in SGX, pay attention to our newest FREE report. We dug deep and uncovered which SGX companies have the potential for massive growth. Even if the numbers look great, things aren’t always what they seem. We let the numbers tell us the full story. Download for free now!

Disclosure: Royston Yang owns shares of DBS Group.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")