' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

- We maintain our view of no Fed rate cuts in 2024 as shelter inflation stays sticky while the US economy remains resilient, supported by consumer spending.

- Anchored by the above view, we continue to favour short duration bonds as yields remain attractive. We also see poorer risk-reward from longer duration bonds currently.

- We are sticking to stronger quality bonds as high rates are likely to exert increasing pressure on high-yield issuers, which are trading at tight valuations.

If 2023 was a year filled with hurdles for bond markets, 2024 is looking to be a year of gradual recovery. In the first six months, performances across most markets were largely positive (Chart 1) after credit spreads tightened as global macro data remained resilient and illuminated a soft-landing outcome, while Fed rates appeared to have peaked. The bond market performance in 1H24 has largely supported our view that the fixed income universe has undergone a transformation, something we shared in our 2024 Global Fixed Income Outlook.

We see 2022 and 2023 as a big reset for the bond universe as markets digest the steep rate hikes and macro changes. With that largely done, bonds now offer much higher yields than before, and we believe the journey ahead should be less volatile. In this article, we share our preferences and recommendations regarding the bonds investors should chase after in 2H24.

Related articles:

Chart 1: Bond markets have rebounded in late-2023, with most markets seeing positive returns in 1H24

1. No Fed rate cuts in 2024

We maintain our view of no Fed rate cuts in 2024 which was a view we held entering 2024, outlined in our Global fixed income outlook. Back then, this was a contrarian stand as markets were pricing in multiple cuts this year, far from what we had expected. However, we have been proven right thus far and we see no need to deviate from our core view.

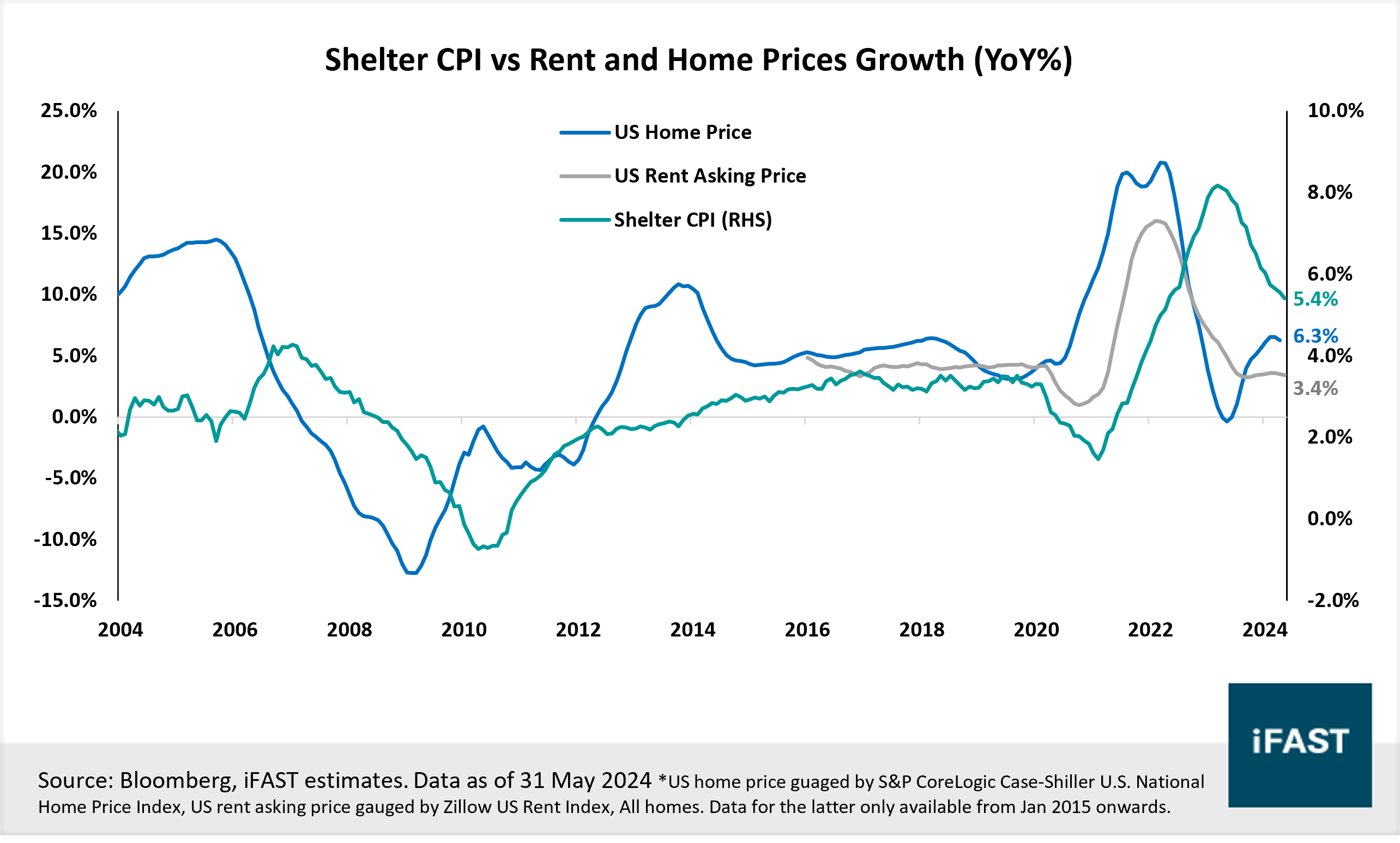

While US inflation has moderated, we do not think it encourages a rate cut this year. Shelter inflation (approximately 36% and 16% of the CPI and PCE basket respectively) remains sticky and was still running hot in May, with an annual rate of 5.4% YoY. Recent housing market indicators have ticked higher despite elevated mortgage rates. Considering a lag in shelter inflation to the broad housing indicators, shelter inflation is likely to remain elevated this year (Chart 2), contributing to a slower-than-expected decline towards the Fed’s 2% core PCE target. In addition, we think the potential turbulence in commodity prices and election uncertainties can inject volatility into the descent of inflation, adding further deterrence to rate cuts this year (Chart 3).

At the same time, the US economy continues to motor on at an unexpectedly brisk pace. The labour market remains resilient, demonstrating sustained momentum in job creation and stable unemployment rates as hiring surged after the pandemic. A healthy US job market has supported disposable personal income growth, bolstering spending despite elevated inflation. Despite some normalisation of consumer spending in 1Q24, we think it will remain resilient this year given the wealth effect from rising asset prices and a risk of post-election stimulus. On balance, we expect consumer spending to support US economic growth in 2024, keeping the drag from high policy rates at bay and providing assurance for the Fed to hold rates.

Related articles:

Chart 2: Growth in home and rent price remains resilient, suggesting that shelter inflation may take longer to subside

Chart 3: US inflation has eased but remains elevated. Core PCE remains firmly above policymaker’s 2% target.

2. Sticking with short duration bonds

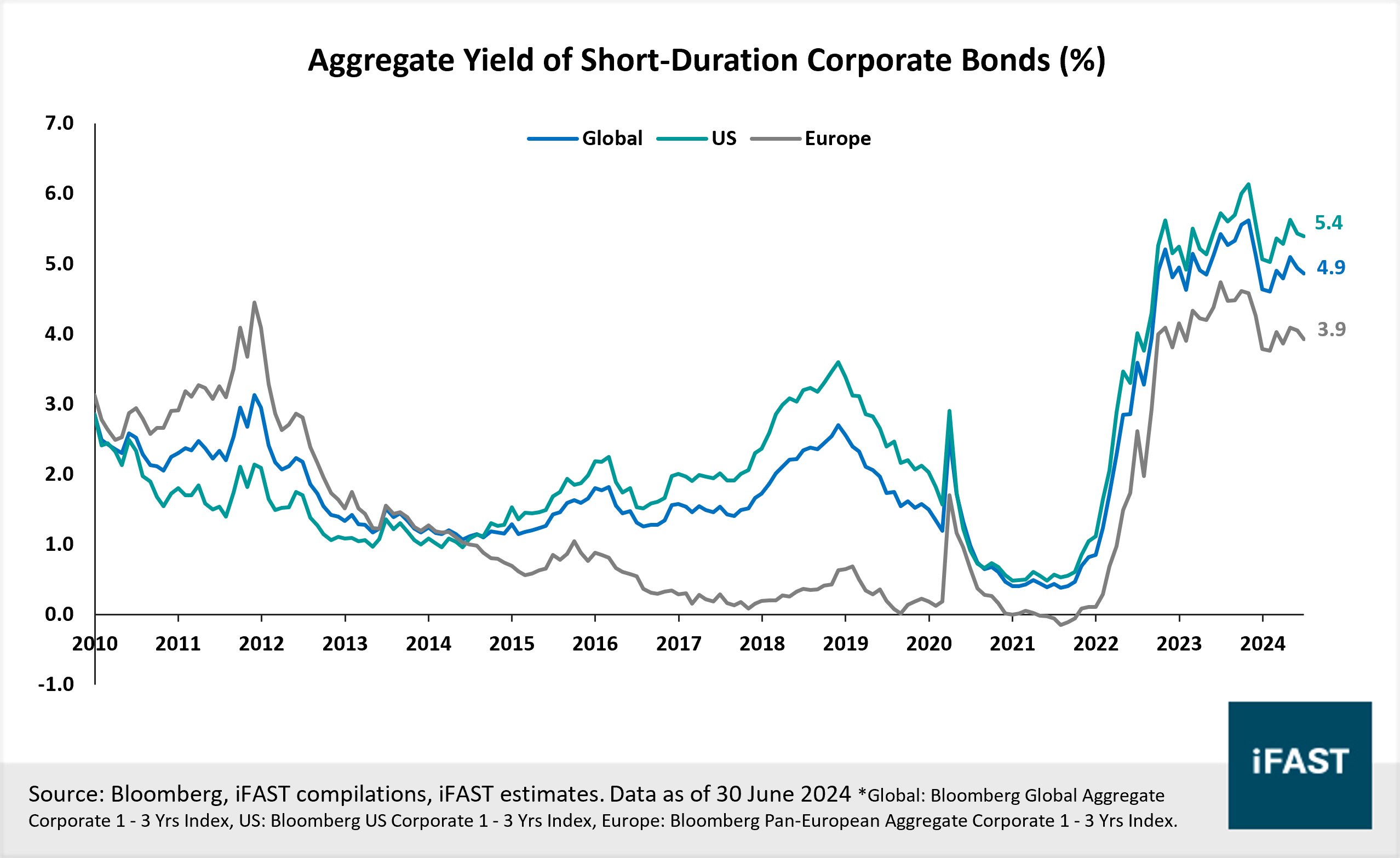

We continue to favour short duration bonds as the investment case remains compelling. Yields of short-duration bonds continue to remain attractive at near-decade highs (Chart 4), supporting forward returns. Absent any Fed rate cuts in 2H24, we think the US treasury curve should remain inverted, keeping short-term yields high. Major central banks - like the ECB - which have cut rates continue to be data-dependent and cautious, as signalled by policymakers. Even as these central banks begin their rate cut cycle, we expect the speed and frequency of future cuts to be gradual and thus, short-term yields could remain elevated in 2H24.

We believe longer duration bonds offer a poorer risk-reward at the moment. First, we see little potential for capital upside without a Fed rate cut in 2H24 as longer-end yields are unlikely to move down substantially amidst resilient economic growth. Second, we think the potential for price volatility is not over for longer duration bonds. Markets are currently pricing in 1 - 2 rate cuts by end-2024 (Chart 5) and, as cuts for this year get pushed back, we expect upward pressure on longer-end treasury yields. This may translate to sub-par performance for longer duration bonds as seen in early 2024.

Generally, we think finding the right window to time the Fed rate cut is a tricky affair given a probable bumpy descent and unpredictability in US inflation data. For investors, extending duration too early may invite unwanted price volatility if markets keep re-pricing the timeline of rate cuts. Investors may also lose out on potentially higher yield pickup from short-term bonds of similar credit quality.

At present, we are comfortable holding on to shorter duration bonds which provide attractive yields, while waiting for signals to extend duration. We look to turn positive on long-duration bonds when the treasury curve un-inverts and re-steepens, giving investors a premium to hold longer-duration bonds. We see room for longer-term treasury yields to rise, primarily from the pushback on rate cuts this year and higher long-term inflation expectations from the current economic resilience. When that happens, assuming short-term yields remain anchored, we think a 10-year UST yield of 6% will be a good reference point to add duration.

For investors seeking exposure to short duration bonds, we recommend Nikko AM Shenton Short Term Bond SGD and United SGD Fund Cl A Acc SGD, which are Singapore-centric bond funds with short duration exposures. We also recommend the Fullerton SGD Cash Fund A SGD and Amundi Funds Cash USD A2 (C) USD as money-market fund options for investors who prefer an even shorter duration.

Related articles:

Chart 4: Short duration corporate bond yields have risen significantly and remain high relative to history

Chart 5: Rate cut expectations have been greatly tempered over the past six months

3. Climb the quality ladder

Sticking with the theme of climbing the quality ladder, which we advocated in our 2024 outlook, we continue to favour stronger quality, investment grade (“IG”) bonds. Since the steep global rate hikes, the cost of borrowing for companies has risen significantly which has exerted greater financial stress on both investment grade and high yield (“HY”) issuer. However, as rates stay higher for longer, we expect HY issuers to exhibit greater vulnerabilities and sensitivity given weaker fundamentals and credit metrics.

For HY issuers, the amount of maturing debt is also expected to climb over the next two years (Chart 6). With a maturity wall hitting as soon as 2025, we see risks of financial stress when the principal repayment on HY debt draws near, and when issuers refinance likely at a much higher cost than before. S&P Global has estimated that 'BB' rated US issuers may see a 2.4% increase in yields for bonds maturing in 2024, up from a median coupon of 4.4%. 'BB' rated European issuers face a larger 3.4% increase, up from the median coupon of 3%. Already, a default cycle for global HY bonds is underway as the trailing 12-month default rates have risen from a low of 1.4% (pre-rate hikes) to around 3.9%, above the 10-year average of 2.7% (Chart 7).

To be clear, we are not expecting a huge wave of default events given the supportive global economic backdrop and resilient corporate earnings. We are, however, expecting increasing pockets of risk for HY issuers moving forward. This is a concern for us as credit spreads for HY bonds have compressed drastically, trading around 387 bps which is below the historical average of 530 bps. From a valuation standpoint, we think high-yield bonds, on aggregate, are expensive and see this as a sign of heightened market optimism, which we think is overdone considering the underlying risks.

On the other hand, global IG bonds remain cheaper than their high yield counterpart. While spreads for global IG bonds have tightened too, the tightening has been less drastic than HY bonds. Often, tight spreads mean that yields are lower but now, global IG corporate bonds offer attractive yields of around 5.0%, which is at the 77th percentile relative to history.

For investors seeking global exposure to investment grade bonds, we recommend the Allianz Global Opportunistic Bond Cl AMg Dis H2-SGD which has a strong average investment-grade rating of AA-.

Chart 6: HY debt might face a maturity wall as soon as 2025

Chart 7: A global default cycle is underway

Looking for individual bond picks?

For investors looking for individual bond picks, table 1 highlights our recommended SGD bonds which have shorter tenors. While many SGD bonds tend to be unrated in general, these picks have a healthy credit quality based on our assessment. Bonds from OUE and Deutsche Bank have investment grade ratings from S&P Global.

Related articles:

Table 1: Recommended SGD corporates

|

Issues |

Ask Price |

Years to Maturity/ call |

Yield to Maturity/ call |

|

98.40 |

1.63 |

5.04% |

|

|

100.58 |

2.84 |

5.03% |

|

|

99.62 |

0.56 |

4.76% |

|

|

100.10 |

0.64 |

4.92% |

|

|

99.45 |

1.82 |

4.42% |

|

|

99.10 |

1.31 |

4.47% |

|

|

99.90 |

1.90 |

4.00% |

|

|

99.97 |

0.68 |

4.03% |

|

|

100.55 |

2.16/ 1.16 |

4.95%/ 4.50% |

|

|

Sources:

Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. |

|||

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")