' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Key fixed income themes for 2024

- Prefer short over longer duration bonds

- Stick with higher quality, investment grade bonds

- Optimistic on Asia investment grade bonds

- Staying cautious on Asia high yield bonds

- Neutral on emerging market bonds. Prefer hard over local currency EM bonds

- Positive on short-term US/ Singapore treasury bills and medium-term Malaysian treasury notes

2023 was a year filled with hurdles for fixed income markets. The numerous inflation surprises and unyielding policy rate hikes acted as key headwinds, weighing down performance across the board. Major fixed income markets started the year on a positive note, but volatility across US treasury yields in the first half of 2023 kept market performance muted. As yields climbed higher in the second half of this year, performances for most fixed income markets softened further. Fortunately, this was short-lived as treasury yields began to descend while credit spreads compressed in November, driving a strong year-end rally across markets.

Despite a tumultuous year, major fixed income markets managed to generate positive returns (Chart 1). Global high yield bonds were the top performer, returning 9.6% year-to-date, fueled by a substantial credit compression across 2H23 as markets aggressively price in a soft landing. Conversely, global bonds were the worst performer, returning 1.5% year-to-date. The steep jump in longer-term US treasury yields across the year weighed on performance of the sector given a slightly longer aggregate duration (all returns are as of 30 November, local currency terms).

As we look back at 2023, we believe the fixed income universe is undergoing a transformation. High interest rates and inflation have resurfaced and are potentially here to stay while global policymakers have warmed up to the idea of holding rates higher for even longer. Meanwhile, global bond yields have climbed drastically, shaping forward-looking returns for bond markets. With these powerful dynamics in mind, here are our views on the global fixed income markets in 2024.

Chart 1: Performance across major fixed income markets in the year so far

1. Prefer short over long-duration bonds

Despite the climb in yields of longer-tenor bonds in 2023, the case for short-duration bonds remains compelling. First, yields of short-duration bonds remain high relative to history and longer-duration bonds following the expeditious rate hikes across major central banks over the past twelve to nineteen months. Policy rates have hit levels not seen since the Great Financial Crisis, catapulting the yields of shorter-tenor treasuries. Additionally, with an inverted yield curve, shorter-tenor treasuries continue to offer higher yields than their longer-tenor counterpart. In the US, the 2-year US treasury (“UST”) is offering a yield of 4.7% as compared to its 10-year counterpart which is yielding 4.3%.

Second, with the US economy proving more durable to higher rates and inflation remaining persistently sticky, we expect policymakers to push back against rate cuts. This sets up a backdrop for higher-for-even-longer rates in 2024, supporting short-duration bond yields for even longer. At the same time, we do not think that Fed rate cuts will come early, contrary to what markets are expecting and pricing in (Chart 2). Absent rate cuts, we see little capital upside for longer-duration bonds.

We look to turn positive on long-duration bonds when the treasury curve un-inverts and re-steepens, giving investors a premium to hold longer-duration bonds. When this happens, with yields of shorter-tenor treasuries at current levels, we believe a good point to add duration would be when 10-year UST yields hit 6%.

For investors seeking global exposure to bonds with a relatively short duration, we recommend the Allianz Global Opportunistic Bond Cl AMg Dis H2-SGD. For investors seeking a more local flavor, we recommend Nikko AM Shenton Short Term Bond SGD and United SGD Fund A Acc SGD, which are Singapore-centric bond funds with short duration.

Related articles:

Chart 2: Markets are expecting one Fed rate cut by June 2024, with almost 100bps cut being priced in for next year

2. Stick with higher quality, investment grade bonds

A higher cost of capital environment, as a result of steep rate hikes, exerts greater stress on both investment grade (“IG”) and high yield (“HY”) issuers. Nonetheless, we expect the former to remain resilient while the latter to face greater financial pressure amidst such an environment. This will be increasingly prevalent next year as a higher-for-even-longer policy rate backdrop plays out.

For HY issuers, the amount of maturing debt is expected to climb over the next three years and a maturity wall is expected to hit as soon as 2025. The repayment of principal on maturing HY debt in a backdrop of slower revenue growth is likely to inject greater pressure on liquidity across HY issuers. Many HY issuers will also be compelled to refinance at a higher cost with rates likely staying higher-for-longer. Based on our estimates, issuers that refinance are paying coupons roughly 3% higher than before global interest rates jumped last year. Collectively, the added pressure from maturing HY debt over the coming years may also raise the risk of issuer downgrades.

From a valuation standpoint, global HY bonds (gauged by the Bloomberg Barclays Global High Yield Index) remain unattractive as compared to global IG bonds (gauged by the Bloomberg Barclays Global Aggregate Index), with credit spreads for the former being too tight relative to the latter (Chart 3). Moreover, the aggregate yield pickup for HY over IG bonds at the moment is around the historical average of 5%. Considering a higher-for-longer rates backdrop and potentially higher credit risk from HY issuers, we think an average pickup does not make HY bonds relatively more attractive.

Considering the above factors, we continue to lean towards higher quality, IG bonds entering 2024. On a top-down level, we prefer IG bonds over HY bonds. On a bottom-up level, we recommend IG bonds with relatively low remaining years to maturity. Table 1 highlights our recommended SGD IG-rated bonds with shorter tenors.

Chart 3: Valuations of global HY bonds remain unattractive as compared to that of global IG bonds

Table 1: Recommended SGD IG-rated bonds with shorter tenor

|

Bond |

Issuer |

Bond Sector |

Credit Rating (S&P/ Fitch) |

|

BNP 3.650% 09Sep2024 Corp (SGD) |

Financials |

A-/ A+ |

|

|

DB 5.000% 05Sep2026 Corp (SGD) |

Financials |

BBB-/ BBB+ |

|

|

FIRTSP 3.250% 07Apr2027 Corp (SGD) |

Real Estate Investment Trust |

AA/ N.R |

|

|

MQGAU 4.500% 18Aug2026 Corp (SGD) |

Financials |

BBB+/ A |

3. Optimistic on Asia investment grade bonds

Despite a more challenging growth backdrop, Asia IG fundamentals have been rather solid as most issuers remain profitable while net gearing ratios held steady despite higher leverage this year. This is supported by resilient growth from parts of Asia like South Korea, Singapore, and Indonesia, which altogether accounts for a sizable exposure within the Bloomberg Asia USD Investment Grade Bond Index. Thus far, we also observe that Asian IG issuers have generally seen a decent improvement in upgrade-downgrade ratios, pointing to a healthy credit profile (Chart 4).

With that being said, credit spreads for the segments remain fairly tight relative to history, trading at late-2019 ranges before the COVID-19 pandemic. On aggregate, the spread is around 106 bps as compared to a long-term average of 169 bps. We think the spread compression seen this year was a result of a large shift away from Asia HY bonds and towards the region’s IG bonds.

Despite tight valuations, the credit profiles of Asia IG issuers are broadly stable, while economic growth in Asia is expected to stay resilient next year. As such, we remain positive on Asia IG bonds and believe an active allocation can help deliver better returns and above-benchmark yields. Our primary recommendation is the Manulife Asia Pacific Investment Grade Bond A MDis SGD which has displayed a combination of good performance and solid risk management, while we also recommend the Schroder ISF Asian Local Currency Bond A Acc USD for investors specifically looking for a local-currency exposure to Asia IG bonds.

Related articles:

Chart 4: Asian IG issuers have seen an improvement in upgrade / downgrade ratios

4. Staying cautious on Asia high yield bonds

2023 was a tough year for Asia high yield bonds and we continue to expect challenges in 2024. This will likely come from issuers in China, despite the broad price rout this year. We are particularly bearish on the Chinese real estate sector.

First, key housing data for property sales, prices, and investment continue to slump and suggest a weak and likely unsustainable recovery. Second, consumer and investor confidences in the sector remain feeble and will continue to cripple property demand within China. While more policy support has emerged, these are mostly targeted towards rescuing key developers rather than reviving property demand. We believe more aggressive support for consumer demand is likely needed, but it remains unclear if Chinese policymakers, who have been unyieldingly prudent, are willing to do so. Lastly, we consistently monitor key Chinese developers and the situation remains challenging from the ground (see related article). Given these hurdles, we think credit fundamentals for China HY issuers are unlikely to see material improvements in the year ahead and default rates should remain elevated.

As such, we think credit spreads for Asia HY bonds are likely to stay elevated next year. While spreads have compressed in recent months (Chart 5), we think they are still too optimistic and discount the risk of a deteriorating China property sector and further slowdown in the nation's economic growth next year, in line with our bearish macro view.

Overall, we continue to stay cautious on Asia high yield bonds entering 2024. Investors who wish to retain exposure to Asia HY bonds should be very selective with their choice of issuer(s) - on this front, we provide regular updates and monitoring on major Chinese developers (see related article).

Alternatively, investors may also consider our recommended fund, Blackrock Asian High Yield Bond A8 SGD-H. The fund remains defensively positioned against near-term risks within the China Real Estate sector. Meanwhile, its remaining positions are towards developers with relatively low near-term redemption pressures, strong access to funding, and small off-balance-sheet obligations.

Chart 5: Credit spreads have compressed significantly since late 2022

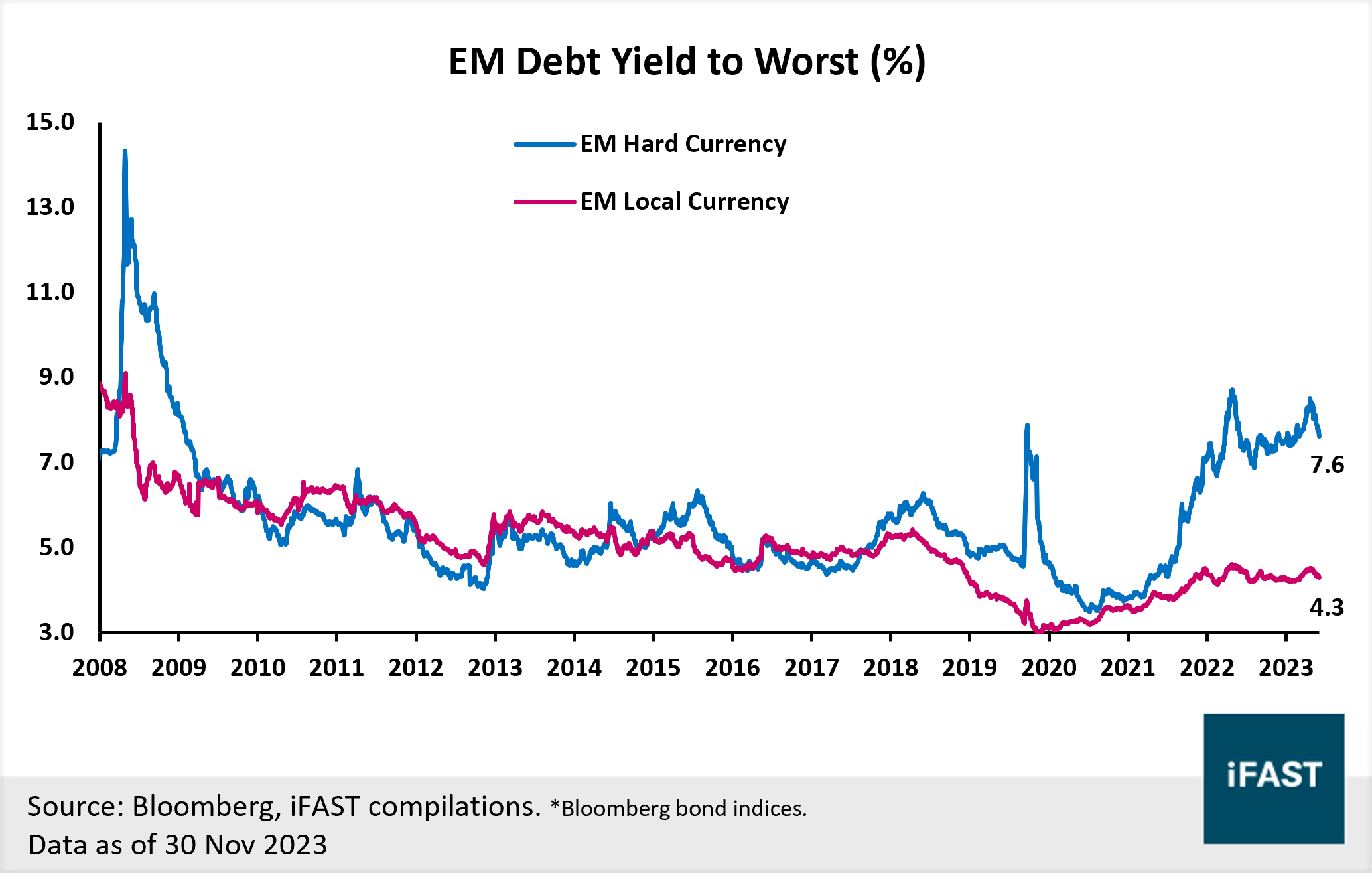

5. Neutral on emerging market bonds. Prefer hard over local currency EM bonds

We find valuations unappealing for EM hard and local currency bonds after much credit spread compression, leaving them slightly below historical average levels. As such, we believe any hiccups in EM economic growth or additional financial stress from a higher-for-longer rates environment in 2024 may widen spreads. This may translate to some bond price volatility and downside.

That said, we expect a potential spread widening for EM bonds to be milder than high yield bonds as EM economic growth has swiftly rebounded after the pandemic and many countries enjoyed progress on fiscal consolidation as well as improved debt metrics. On aggregate, EM hard and local currency bonds hold a credit rating of BBB- and BBB+ respectively (gauged by the JPM EMBI index and the JPM GBI-EM Global Diversified Index), stronger than high yield bonds.

EM hard currency bonds continue to offer high all-in yields relative to history. At 7.6%, the yield is close to the highest level since 2009. The segment, which has an IG rating, also offers a strong yield pickup of 3.3% over US treasury (“UST”) of similar duration.

Against tight valuations and potential spread widening but high all-in yields, we are neutral on EM bonds entering 2024. We prefer EM hard currency bonds over the local currency counterpart for two reasons. First, EM hard currency bonds offer a generous pickup over EM local currency bonds (Chart 6). Second, FX gains are a dominant driver of return for the latter and we expect continued FX volatility and downward pressure on many EM currencies.

For investors seeking exposure to EM hard currency bonds, we recommend the PIMCO Emerging Markets Bond Fund Cl E Acc SGD-H. We like the fund for its disciplined risk management, consistent outperformance against peer funds, as well as the scale and expertise of PIMCO’s EM research team.

Chart 6: EM Hard Currency bonds are offering attractive yield and a generous pickup over its local currency counterpart

6. Positive on short-term US/ Singapore treasury bills and medium-term Malaysian treasury notes

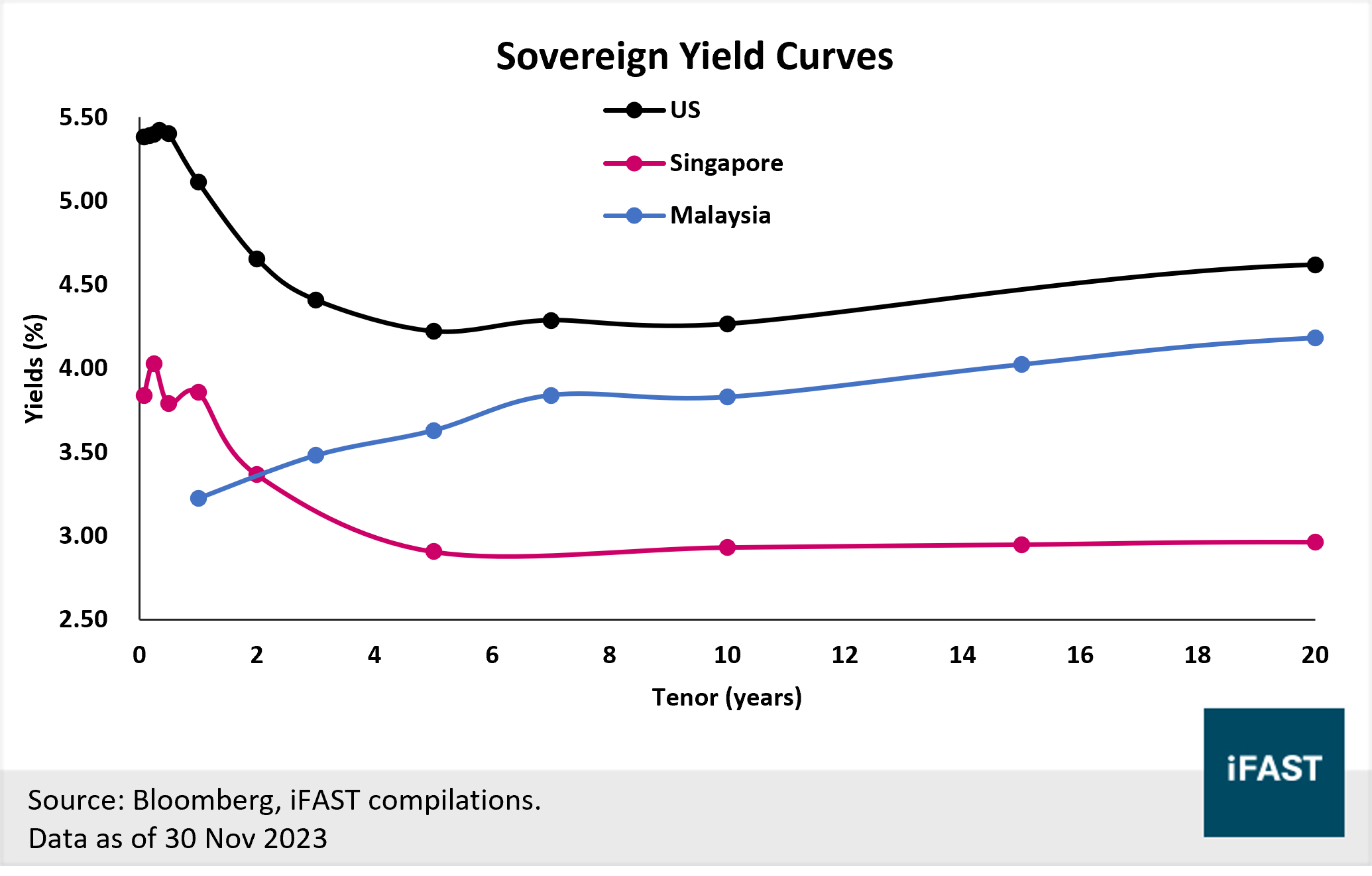

Since global central banks started hiking rates expeditiously, government treasuries have become an increasingly attractive investment tool. The surge in policy rates has catapulted treasury yields of major developed markets to levels not seen since the Great Financial Crisis. As the global rate hike cycle winds down and market’s expectation of a rate pause grows, we continue to find certain segments of government treasuries attractive.

For US and Singapore government securities, we like shorter-term treasury bills, in line with our preference for shorter-duration bonds. The US and Singapore yield curve remains inverted (Chart 7), supporting the attractiveness of short-dated treasuries relative to long-dated ones as yields of the former remain higher. At the same time, we think yields from long-dated treasuries are too low and do not offer investors enough premium considering the risk of inflation and hawkish policy surprise. Lastly, our view of higher-for-even-longer policy rates in 2024 also meant that investors have a longer runway to lock in attractive yields.

For Malaysian government securities, we like medium-term treasury notes. Our preference deviates from our short-duration call for several reasons. First, Malaysia’s yield curve remains upward-sloping where yields of longer-term treasuries are generally higher than shorter-term ones (Chart 7). Second, we expect Malaysia’s inflation to remain stable in 2024 and the central bank to hold OPR rates at 3%. Thus, we see lower duration risk for longer-term treasuries.

We find the sweet spot for investors to be medium-term treasury notes (between 5 to 7 years) as yields of between 3.6% to 3.8% are attractive. At the same time, we also find the yield pickup of treasuries with even longer tenor to be insufficient in compensating for the extra duration risk.

Chart 7: UST and SGS curve remains inverted while MGB curve is upward-sloping

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a position in FIRTSP 3.250% 07Apr2027 Corp (SGD), FIRTSP 4.9817% Perpetual Corp (SGD), and the analyst who produced this report holds a NIL position in securities mentioned in this article.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")