' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

How did FSM Indices (Equities & Bonds) perform in September?

September was a difficult month for both fixed income and equity markets, with the Fed pointing towards more restrictive policy and a higher-for-longer approach to interest rates. Overall, FSM Indices – All Bond outperformed FSM Indices – All Equity, returning -1.20% and -1.82% respectively (all performance figures in SGD terms), as investors adopted a risk-off approach.

Note: FSM Indices are a simple average of all unique fund strategies within the category listed on our platform. Investors can use it to compare a single fund against its peer average, or its actively managed products on our platform against the market index

Figure 1: FSM Indices Performance in September

FSM Indices – Asian High Yield Bond was the best performer for the month, returning positive returns of +1.88%. The relatively better performance was due to the gradual credit spread tightening, coming off an extremely bearish position. Furthermore, there was positive news flow coming from China, as Country Garden, one of China’s largest property developers, managed to dodge a default and extended its bond payments, which drove some optimism back into the markets.

FSM Indices – Global Property Equity was the worst performer for the month, with a -7.07% decline. The real estate sector is particularly sensitive to interest rates and the shift towards higher-for-longer rates have negatively affected investors’ sentiments especially when these properties need to refinanced at these higher rates in future. China’s real estate market continues to remain fragile, with poor consumer and investment sentiment impacting the demand for Chinese properties, and serving as a drag on the country’s economic growth.

FSM Indices – Technology Equity was another poor performer in the month of September, registering a -7.06% decline as 10-Year Treasury yields surged. With investors starting to digest the Federal Reserve’s stance to keep interest rates higher-for-longer, tech stocks which tend to be more growth-oriented have experienced a sell-down with the likes of Apple, Amazon, Nvidia down by -7.94%, -6.95%, -10.96% (in SGD terms) respectively in the month of September.

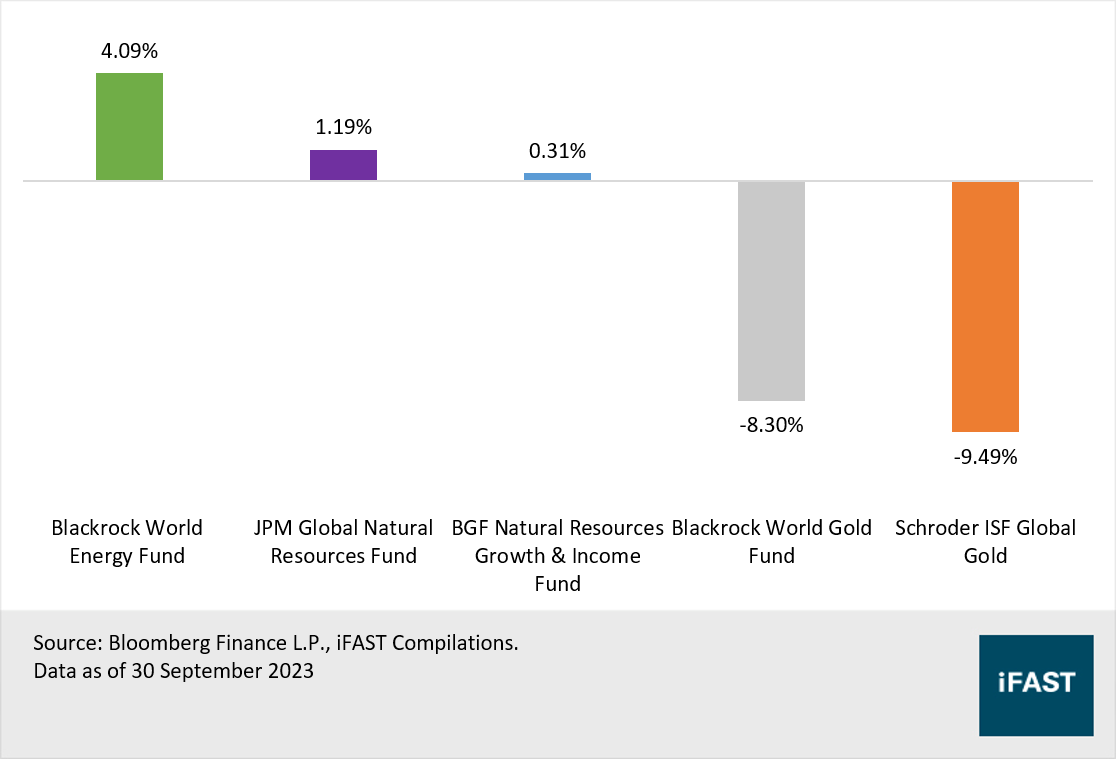

Looking at commodity and energy funds, they delivered mixed results in September (Figure 2). Energy-related funds outperformed gold-related funds, as oil prices have been creeping up on lower US crude inventories and further output cuts by OPEC+, while higher Treasury yields make holding zero-yield bullion less attractive.

Figure 2: Returns of Commodity and Energy Funds in September

Here are some noteworthy funds we’ll like you to check out

Manulife Asia-Pacific Investment Grade Bond Fund: A strategic way to navigate the Asian IG landscape

For investors who are looking to actively navigate the diverse Asian Investment Grade (IG) Bond landscape, the Manulife Asia Pacific Investment Grade Bond Fund is our top pick. We believe the Asian IG bond segment remains an important part of the fixed income universe, and an active allocation combining both top-down and bottom-up research will be important for investors.

The fund expects to generate returns from a combination of three sources: (i) interest rate strategies (interest rate duration and yield curve); (ii) credit positioning (sector allocation and name selection); and (iii) active FX management. The investment process comprises top-down fundamental research of each market, as well as bottom-up credit research of each issuer.

The fund is also well diversified, be it the type of issuer (corporate/sovereign), geography or sector. Geographically, the fund has a slight underweight to China against its benchmark, as the fund managers expect an uneven path to recovery in China given recent lukewarm economic data and have expressed caution on the magnitude and effect of broader demand-side stimulus so far. This is in line with our view as we continue to adopt a cautious approach towards China.

Lastly, within the Asian Fixed Income Fund space, the Manulife Asia Pacific Investment Grade Bond Fund stands out for its strong historical performance and downside risk management relative to its peers.

JP Morgan Brazil Equity Fund: Look to Brazil for a compelling investment opportunity

Next up, we highlight the JP Morgan Brazil Equity Fund, as we believe there is a compelling case for investing in Brazil, with improving macroeconomic conditions and monetary easing creating a supportive backdrop for equities.

The fund is managed primarily from a fundamental, bottom-up perspective using ideas generated by both the portfolio manager and a team of emerging markets investment professionals. More specifically, the fund focuses on investing in high quality businesses that compound earnings sustainably over the long-term, with in-depth fundamental analysis focusing on the Economics (e.g. sustainable return of capital, cash flow generation), Duration (e.g. industry structure & growth, resilience of the business), and Governance (e.g. shareholder focus, management competence).

Overall, it runs a concentrated portfolio of approximately 25-50 securities (currently has 37 holdings as of 31 July 2023). The fund also stands out for its strong performance, having managed to outperform its peers, while exhibiting a lower maximum drawdown in the last five years.

Finally, our top fund pick for the month!

Our top fund pick for the month of September is the Fidelity American Growth Fund A-USD!

The Fidelity American Growth Fund seeks to deliver long-term capital growth by investing in equities of companies that are headquartered or do most of their business in the US. Although the fund has a flexible investment style as it takes into account the prevailing and expected macroeconomic conditions, its core investment approach is to identify companies that are most likely to benefit from secular growth trends.

The fund is also benchmark agnostic and has no restrictions to invest in any comparative market index sector/holdings. As a result of this unconstrained approach, the fund’s exposure may differ substantially from the benchmark. The fund holds a high conviction portfolio of between 60-80 stocks at any time.

Consistent with the current environment of slowing growth and elevated inflation, the fund is defensively positioned, with sizeable overweights to traditionally defensive sectors such as healthcare and consumer staples. Some of the top holdings include the likes of Astrazeneca, Horizon Therapeutics and Johnson & Johnson.

Moreover, over a five-year period, the fund has experienced a lower maximum drawdown as compared to its peers, while also having a stronger performance than its peers. This is a testament to the portfolio managers’ stock picking skills and their quality focused investment philosophy.

Final Thoughts

The US economy continues to remain resilient, powered by the strength of US consumers. Moreover, the labour market also continues to show strength, with US employment having increased the most in eight months in September as hiring rose broadly. Persistent labour market strength could give the Fed ammunition to continue hiking rates, or hold it at elevated levels for a prolonged period of time. Market participants may be finally starting to price in the fact that we are in a new economic regime, where structural forces would keep inflation elevated as compared to the past decade.

Looking across equities, we have a preference for US big tech stocks, given their strong moats, pricing power and global business models. Beyond which, they can also venture into the Japanese equity market, which would continue to benefit from several tailwinds. Last but not least, investors can also consider the Asian Tigers, such as Singapore and South Korea due to more attractive valuations.

Related articles:

Why these technology stocks are better than the rest

Don’t miss out on our top investment ideas following Japan’s latest policy tweak

The Shifting Geopolitics and The New Asian Tigers

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")