' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

There may be the temptation by some investors to associate value investing with companies that have poor environmental, social and governance (ESG) profiles. After all, value investing globally, including Japan, has been underperforming growth investing since the Lehman crisis in 2008 despite value’s strong rally in the first half of 2021. Meanwhile, over this 12-year period, responsible investing has gained significant traction with investors.

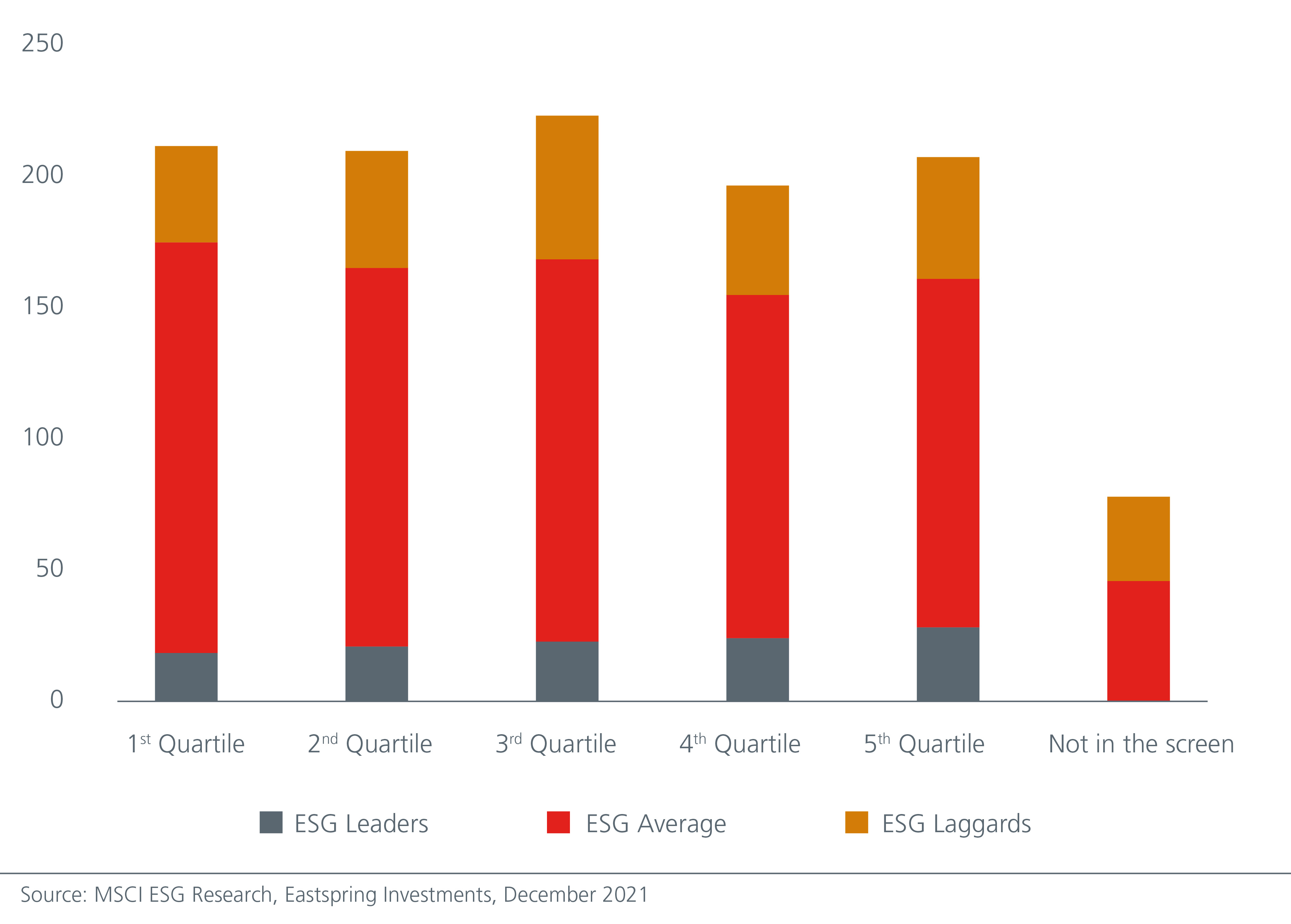

We debunk this misconception using ESG research and analysis by MSCI as well as our proprietary valuation screen. We observe that companies in Japan that are categorised as ESG leaders as well as those with average ESG ratings are evenly distributed across the valuation quintiles. See Fig. 1. Therefore, there is no evidence to suggest that cheap value stocks have poor ESG ratings or that expensive growth stocks have high ESG ratings in Japan.

Fig.1. Distribution of ESG ratings by valuation quintiles1 for Japanese equities

In fact, even in traditional value industries such as steel manufacturing or cement production, we have been able to identify Japanese companies that have been addressing sustainability issues such as emissions, water usage, waste treatment etc. in their operations for a long time, with some even leading their global peers in sustainability practices.

Value and ESG are aligned

We are convinced that value investing is aligned with ESG investing.

For one, value investors, such as ourselves, seek to identify material factors that can influence a company’s long-term trend returns and valuations. This is done through rigorous due diligence of both financial and non-financial factors to identify all material risks to the sustainable earnings of the company, as well as the potential opportunities. This process naturally includes assessment of the company’s governance framework, social behaviour and environmental impact.

Next, value investing requires a long-term and patient approach. A long-term investment horizon is in line with ongoing company engagement. To encourage the best outcomes, an investor needs to stay engaged with senior management and the board of companies. In our experience with Japanese corporates, we have been able to develop constructive relationships with the senior management of our investee companies and have been encouraged by the measurable progress seen as these companies address ESG issues.

Value investors also seek to identify and exploit mispricing opportunities. The strong emphasis on environmental factors due to the heightened media coverage on the urgent task of addressing climate change risks may have created certain biases in the market. Some investors may be inclined to avoid companies that they perceive to be bad for the environment and instead gravitate towards those that are perceived to be good or at least have little negative impact on the environment. This explains the rise in thematic ESG investment solutions globally. This behavioural bias potentially provides fertile ground for value investors to identify mispriced companies through rigorous fundamental due diligence.

The ESG case for Japan

Japan’s unique geography and culture, as well as Japanese companies’ mixed ESG performance suggests that there is room for further improvements in sustainable practices, making a strong case for ESG investing.

We have observed notable improvement in sustainability practices at many Japanese companies over the recent years. For example, the number of companies that voluntarily hold media or investor briefings solely on sustainability issues has increased. There are now dedicated sections on ESG/sustainability even within regular financial results briefings. There are also more corporate disclosures on sustainability although Japanese companies on average still disclose less ESG data than their US and European counterparts.

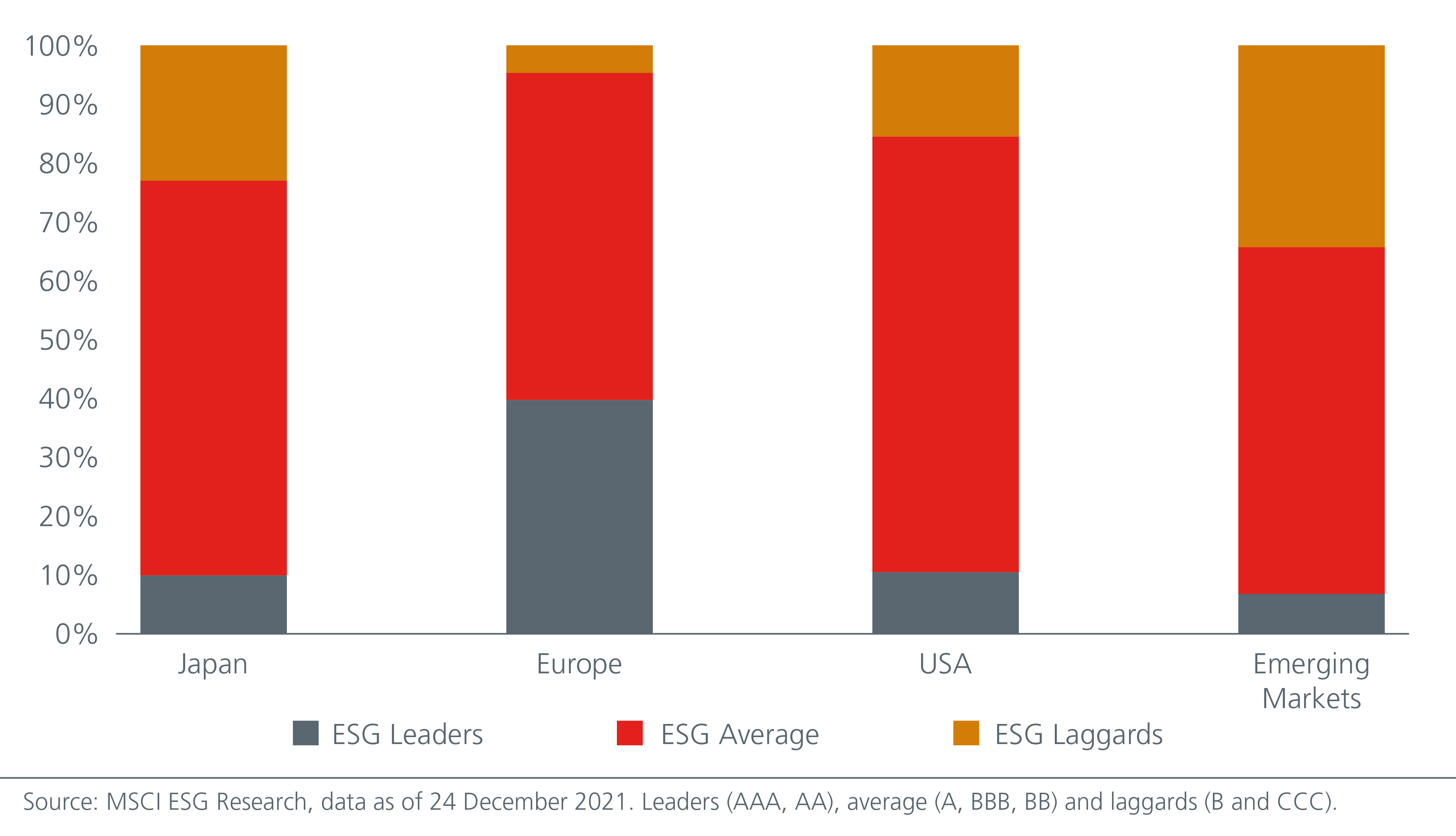

In addition, according to MSCI ESG Research, Japanese companies still lag Europe and the US in terms of sustainability performance. Only 10% of Japanese companies is assigned Leaders ratings (AAA, AA), which is similar to the US but far behind European companies. See Fig. 2

Fig.2. Distribution of Corporate ESG Ratings2 by MSCI

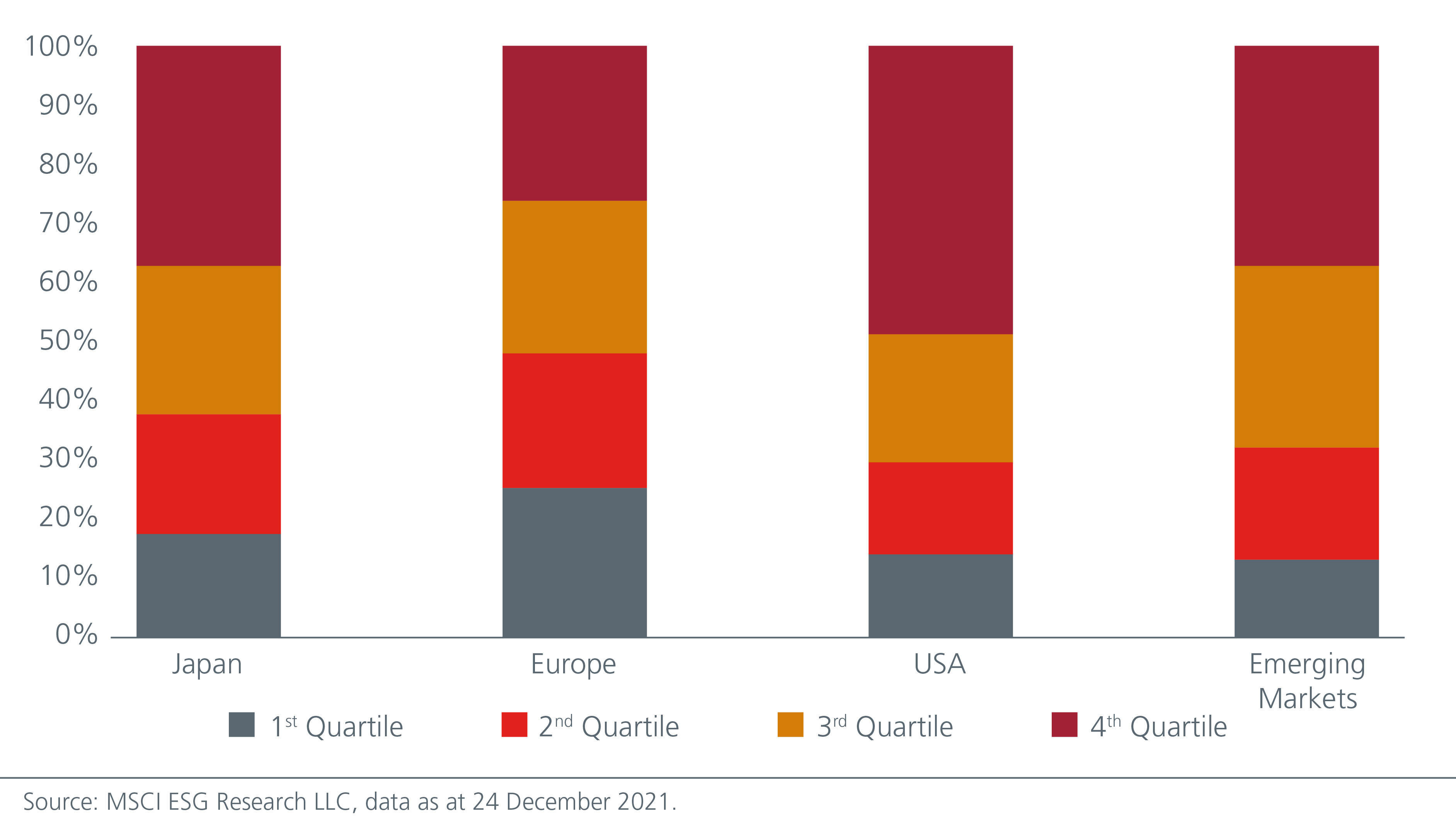

A drill down of the sustainability ratings by MSCI reveals some interesting observations. In terms of environmental practices, 38% of Japanese companies is rated in the first and second quartiles. While this is behind Europe which has 48% of the companies rated within the first and second quartiles, Japan is ahead of the US with 30% and the Emerging Markets (EM) with 32%. See Fig.3. This suggests that Japanese companies have reasonable plans and policies to address environmental concerns despite Japan being the fifth largest emitter of greenhouse gases. Japan had switched its energy sources from nuclear power to fossil fuel in the aftermath of the Great Tohoku earthquake in March 2011 which caused majority of its nuclear power reactors to be shut down.

Fig. 3. Distribution of Environmental Pillar Score by Quartile

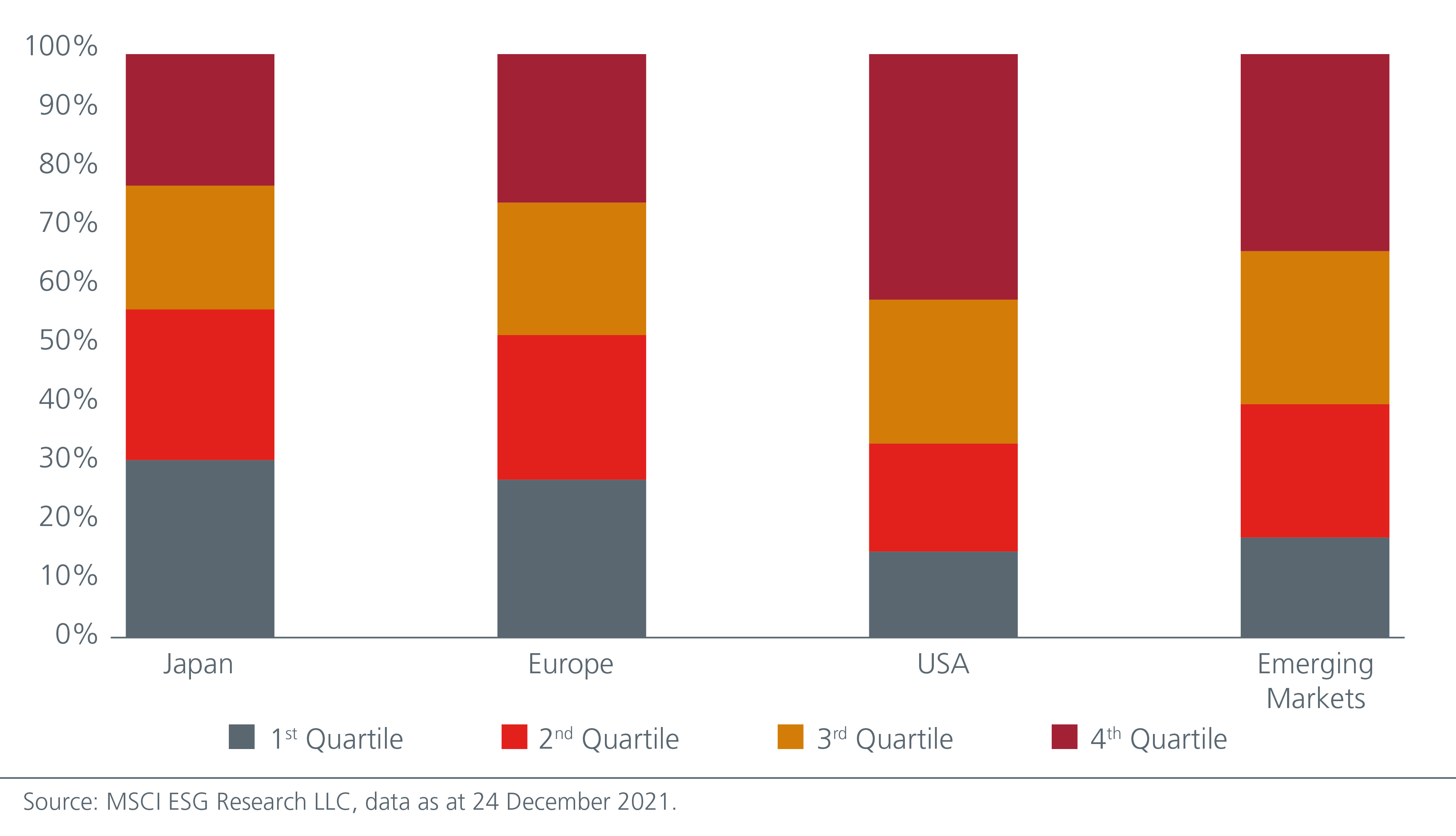

On social issues, Japanese companies seem to lead global peers with 56% of Japanese companies in the first and second quartiles beating 52% for Europe, 33% for the US and 40% for the EM. See Fig. 4. We believe that Japanese companies’ better performance on social issues has roots in Japan’s unique culture of prioritising the interests of other stakeholders and communities. Scholars and consultants have often cited the old code of ethics (shuchu kiyaku) by Japanese merchants in the 1500s as a general guideline that trade should not only be carried out for one’s own profit but also for the benefit of others. Ryuzaburo Kaku, Chairman of Canon from 1989 to 1997, further explained this practice as kyōsei or “the spirit of a corporation” where individuals and organizations live and work together for a common good3. As a result, the good practices of taking care of employees and communities have a long tradition amongst Japanese companies.

Fig. 4. Distribution of Social Pillar Score by Quartile

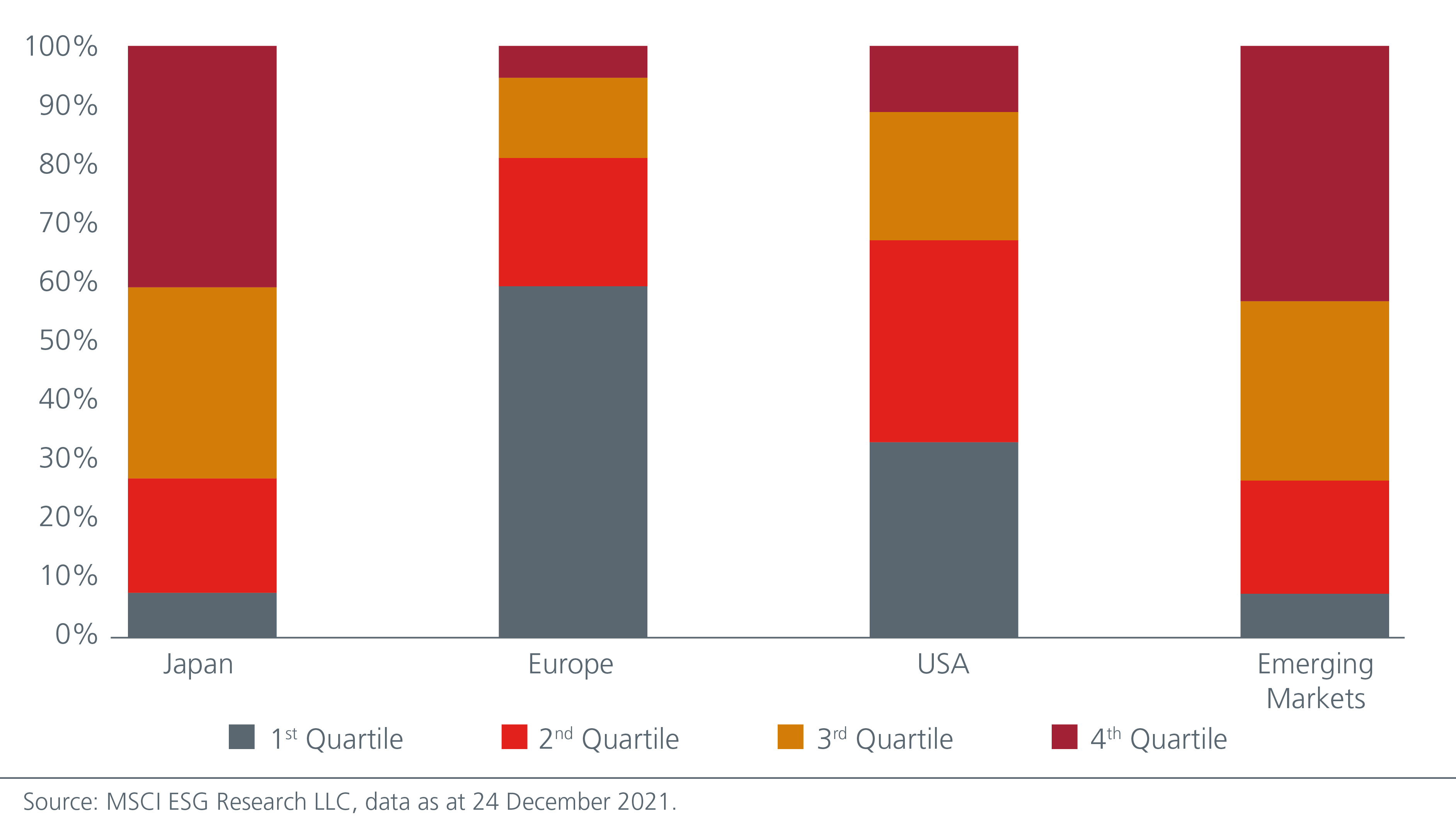

On governance metrics, Japan and EM ranked the lowest with 27% of companies in the first and second quartiles versus 82% for Europe and 67% for the US. See Fig. 5. The history of zaibatsu4 and keiretsu5 pre and post-World War II (WWII) strengthened the cross-shareholding framework that has existed in Japan’s corporate sector for a long time.

Fig. 5. Distribution of Governance Pillar Score by Quartile

While this inter-dependent relationship facilitated Japan’s rapid industrialisation after WWII, it also created significant agency challenges. Under the “three-arrows” strategy launched in 2012 by the Abe administration, corporate governance reform was seen as one of the key avenues to spur economic growth. The Japan Stewardship Code which was issued by the Financial Services Agency in 2013, and the Japan Corporate Governance Code that came into effect in June 2015, both of which were subsequently revised and enhanced to date, have played important roles in improving corporate governance in Japan and unlocking corporate as well as shareholder value.

Adding value

We believe that value investing is aligned with ESG investing. As long-term value investors, ESG considerations are an integral part of our investment process.

At the same time, we believe there is no single approach to ESG investing. We do not avoid investing in a company simply because it has a poor sustainability risk profile or practices. We may still consider investing if we believe that we are more than compensated by the valuation support and that we can improve the company’s sustainability practices through active engagement with the management and the board.

In Japan, where there is still little consistency on what ESG data sets companies must disclose and what ESG information is useful for investors, regulators and other stakeholders, robust due diligence is important to supplement third party ESG data. This, together with a highly disciplined investment process and experience can help investors achieve long-term returns in a responsible manner.

This article was originally published on Eastspring website.

Click here for more related insights from Eastspring.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")