' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Stewardship is generally defined as the trustworthy management of something committed to one’s charge. In the investment world, it refers to institutional investors using their influence over existing or potential investees to maximise the overall long-term value for shareowners. Since the 2008 Global Financial Crisis, new investor stewardship codes have been sprouting around the globe, reflecting the growing demand for responsible investment practices and sustainable value creation.

Several global stewardship codes exist, such as the International Corporate Governance Network’s (ICGN) Global Stewardship Principles and the OECD Stewardship Code. Equally, local stewardship codes have been published in over 20 countries. In the Asia Pacific region, Australia and New Zealand lead in terms of active stewardship and engagement. The rest of Asia is also seeing a rise in the number of PRI1 signatories. To date, 270 investors have signed up and in China alone the number of signatories has surged by 77% from 2019 to 2020.2

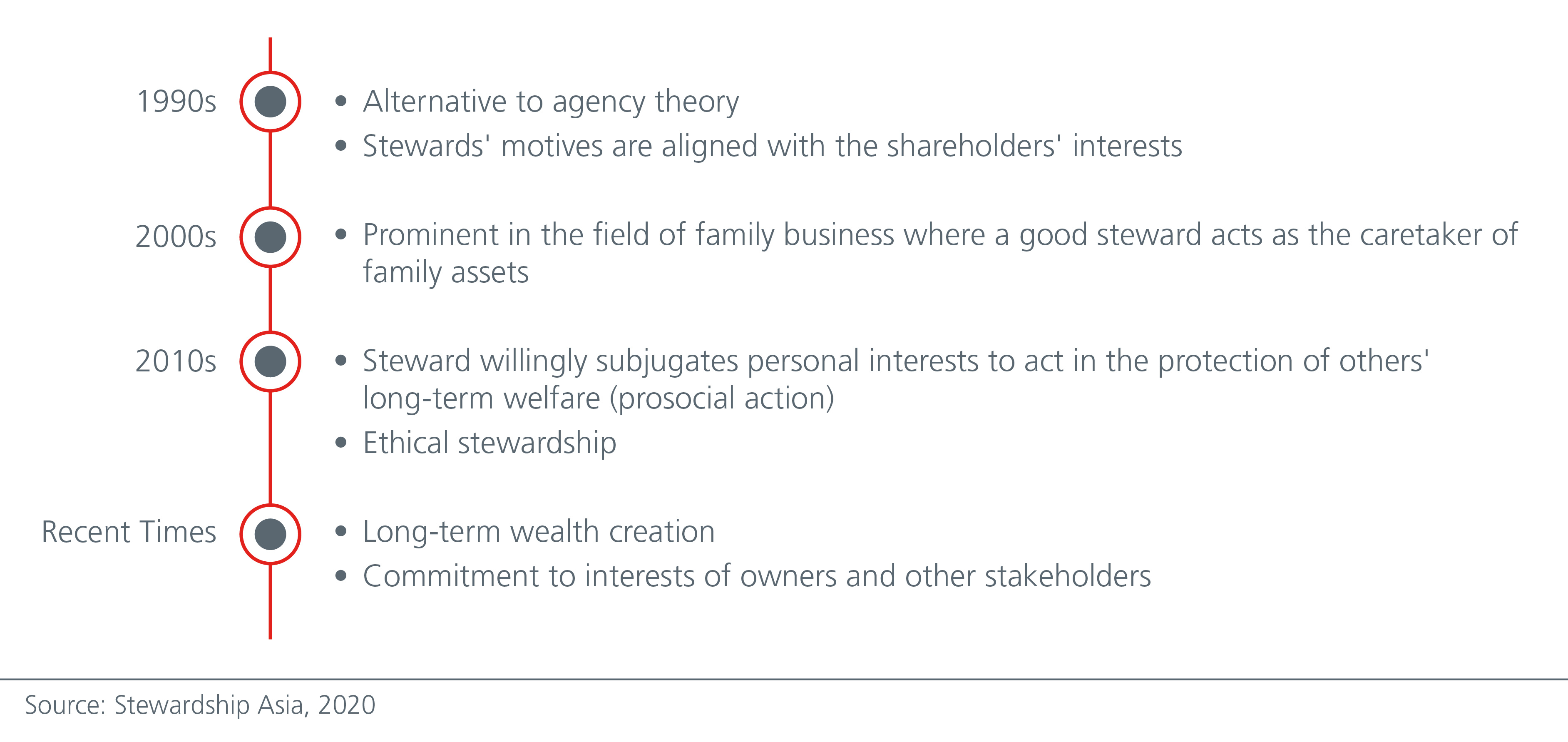

Fig 1: Evolution of concepts and theories on corporate stewardship

Common stewardship tools

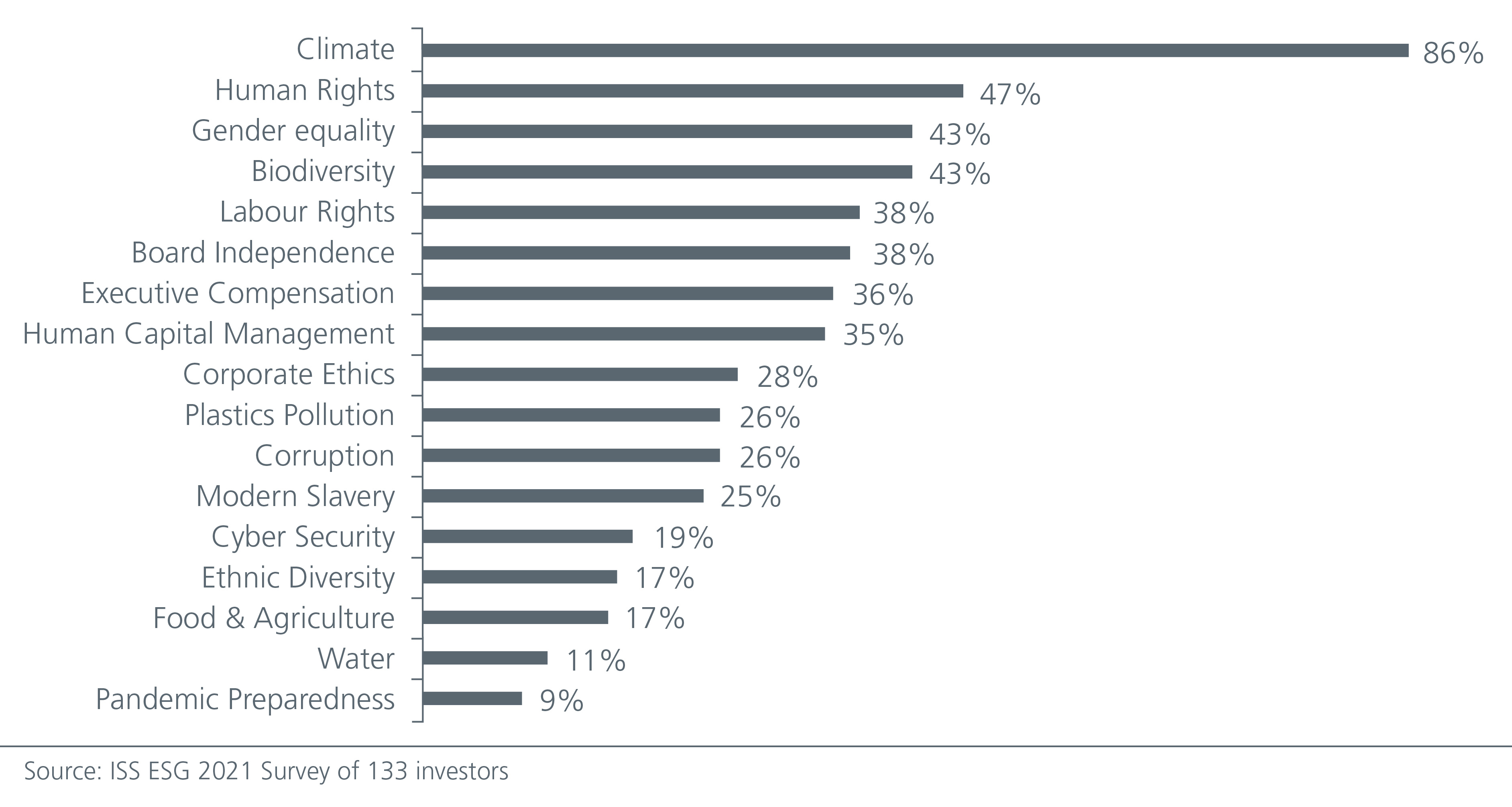

These ICGN Global Stewardship Principles3 serve as a benchmark of international reference. Of these, corporate engagements, voting and reporting on sustainable business practices are the commonly used tools for active stewardship. Investor engagement refers to an investor having regular conversations with existing or potential investee companies to improve their ESG practices, sustainability outcomes or public disclosures. In fact, ESG issues tend to be on most engagement agendas. A recent survey done by ISS ESG revealed that climate engagement is the key priority.

Fig 2: Most important engagement topics

Voting is another area that has gained traction. Proxy voting is increasingly used by institutional investors to vote on specific matters -- such as director elections, executive remuneration, and resolutions -- that are proposed by a company at its annual general meeting. This tool enables shareholders to exert influence over a company’s operations, environmental, social, and corporate governance policies and forces the company’s board to improve accountability. Letter writing is also used to register displeasure or lobby for change in a company’s corporate governance practices.

Stewardship strengthens our ESG integration

We view stewardship as a strategy that complements the incorporation of environmental, social and governance (ESG) factors in our investment processes. The best responsible practices are ones that include dialogues with the companies we are analysing, as the perspectives offered by these companies allow us to shape our thinking and enhance our investment and decision-making process.

For example, Eastspring Investment’s Core Equities team has adopted an “AEM: Analyse, Engage, Monitor” approach in integrating ESG into our investment process. We consider environmental, social, and governance issues as they impact a company’s profitability, cash flows, and business sustainability, and we apply the Sustainability Accounting Standards Board (SASB) framework while utilising both internal and external resources in our analysis.

This approach promotes increased long-term shareholder value creation and sustainable business practices by companies, as we engage with companies in which we invest to make sure we communicate and understand the issues. We also believe that an active and informed voting policy is an integral part of our stewardship responsibilities and investment process, and as voting should never be divorced from the underlying investment activity, we vote proxies on all resolutions, except where it is not in our client’s best interests. This systematic process also involves thorough documentation to enable effective engagement and monitoring of the firm’s sustainability goals.

Our work has been incorporated into company-specific ESG tear sheets which summarise our findings around the SASB framework. The team also works with an internal Responsible Investments Specialist team that is responsible for oversight and the implementation of the firm’s stewardship and ESG Policy. This internal group helps to frame the Policy and serve as conduits to our wider group of investment professionals and engages other active members of collaborative organisations in the region and globally that are aligned to these initiatives.

Current limitations

In the 2020 Asian Corporate Governance Watch report, the investors’ rating category, which considers factors such as the implementation of stewardship codes and the will and capacity to engage with investees amongst others, scored the lowest. This should not come as a surprise given the number of limitations.

Key amongst these limitations is the lack of enforcement and oversight by a regulatory body. This is a major challenge given that most of the codes are under a voluntary or comply-or-explain regime. Investors that adhere strictly to the code stand to distinguish themselves from peers. Nonetheless many would-be aspirants are also questioning the benefits of adopting and implementing stewardship codes. In fact, the impact of stewardship codes on improving corporates’ ESG performance is even more difficult amidst the ongoing debate on how best to measure and quantify the ESG impact. Given that the value creation for beneficiaries remains uncertain, there is a lack of will to commit resources behind stewardship.

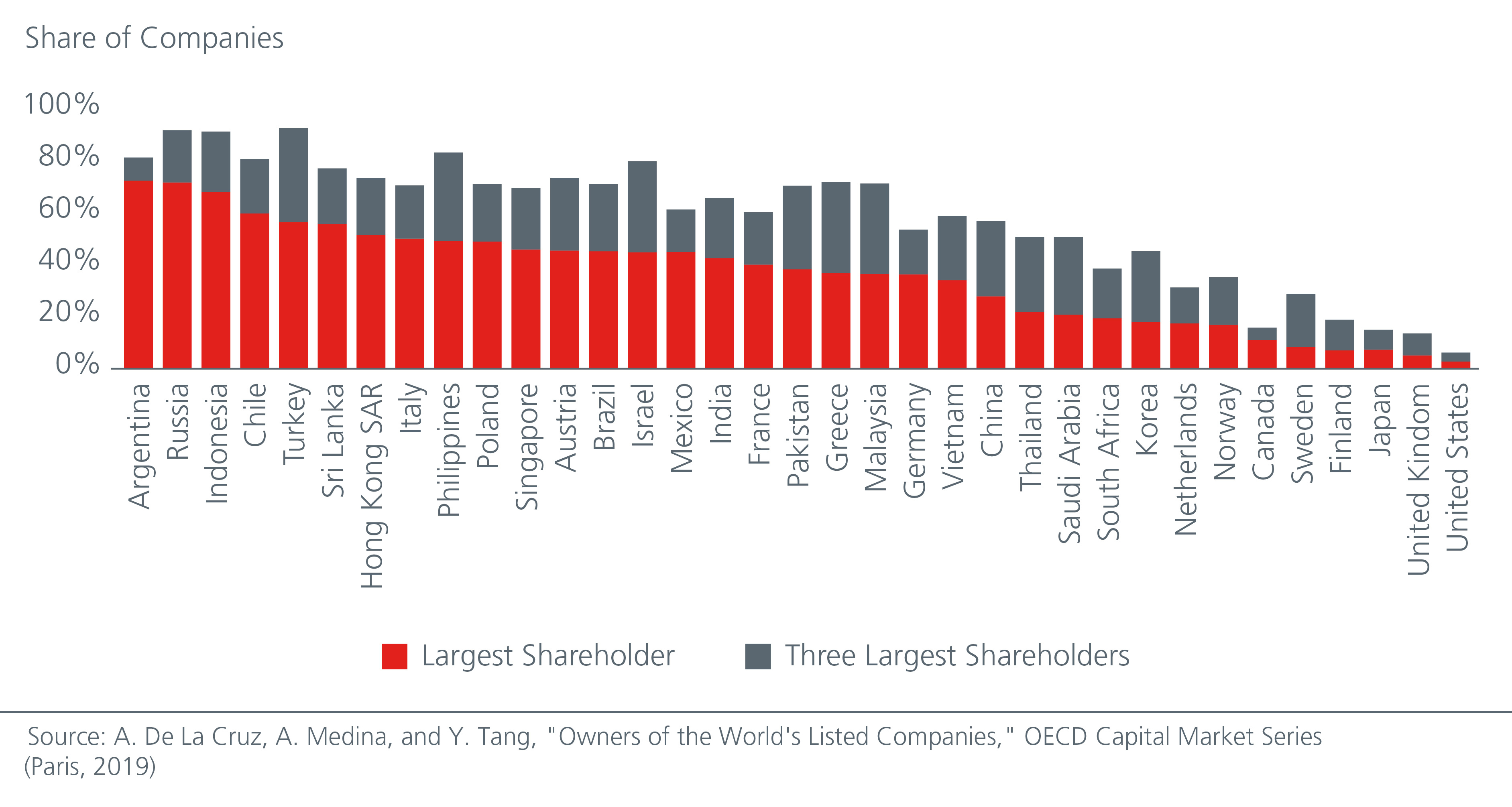

Another major issue is the ownership structure. In Asia, most of the controlling shareholders of listed companies are often families, the state or other corporations that have actual or de facto control over the corporate’s governance practices through their voting rights. The concentrated ownership structures imply these shareholders have the power to influence decisions and hence limit the effectiveness of stewardship activities.

Fig 3: Ownership concentration by country

The level of institutional ownership matters as well. Compared to the high levels of 80% in the US and 68% in the UK, Asia Pacific markets have levels that are less than half of these numbers.4 Furthermore, if the government happens to be the controlling shareholder, an institutional investor may be disinclined to vote against it. Effective stewardship may therefore be a challenge across countries in Asia Pacific.

Becoming a fundamental process

Although there are limitations to implement stewardship codes effectively, we think investment stewardship will eventually become a fundamental process for asset managers. Asset owners across the globe increasingly desire to see their asset managers engage actively with investee companies with ESG engagement leading the way.

In fact, one of ICGN’s core policy priorities focuses on making successful stewardship a reality. For this to happen, it is necessary to quantify the value of stewardship and develop criteria to help differentiate firms based on stewardship. As such, expect stewardship models for asset managers to evolve over time and address both company-specific and portfolio-level systemic risks.

This article was originally published on Eastspring website.

Click here for more related insights from Eastspring.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")