' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

What is CareShield Life?

CareShield Life is a long-term care insurance scheme that seeks to provide basic financial support for all Singaporeans should they become severely disabled. This is defined as the inability to perform at least 3 out of 6 Activities of Daily Living (ADLs).

This national scheme has replaced the previous ElderShield scheme and Singaporeans and Permanent Residents (PRs) who are born in 1980 or later will be automatically enrolled into CareShield Life on their 30th birthday. Premiums will be payable from the age you join until age 67.

(Read more: Our honest opinions about CareShield Life and its supplements)

Commonly asked questions about CareShield Life

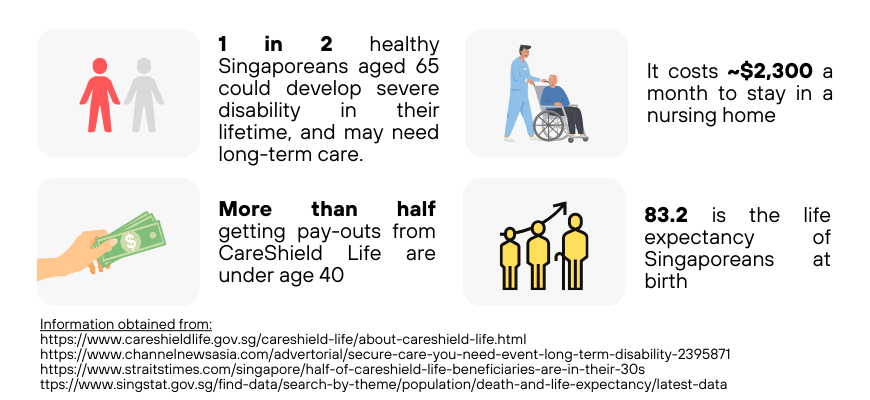

Q: Disability insurance is only applicable to the older age group.

A: Did you know that more than half of those getting pay-outs from CareShield Life are under 40 years old? With claimants having a median age of 39, this shows that a disability may strike at any age, and disability insurance may be applicable to all.1

Q: Are CareShield Life monthly disability benefits enough?

A: CareShield Life monthly disability benefit started at $600 in 2020 and is currently set at $649 in 2024. This monthly benefit is set to increase at 2% per year from 2020 to 2025. Beyond this, any further increases in payouts and necessary adjustments to premiums will be subject to the recommendations made by CareShield Life Council.4

Year |

CareShield Life monthly disability benefit |

2023 |

$637 |

2024 |

$649 |

2025 |

$662 |

If you feel that the monthly disability benefit from CareShield Life is insufficient, you may wish to opt for a CareShield Life supplement to enhance your coverage. This will allow you to receive higher monthly disability benefits, and you could also choose to have your monthly disability benefit commence from the inability to perform one or two ADLs.

Q: Can I enhance my CareShield Life coverage?

A: Yes, you may enhance your CareShield Life with a supplement. This is available from 3 insurers: Singlife, Income and Great Eastern.

CareShield Life supplements available on FSMOne:

Singlife CareShield Standard or Plus |

Income Care Secure |

|

|

|

|

Administered by |

Singlife |

Income |

Monthly disability benefit |

Choice from $200 to $5,000 in increments of $100. Benefit is given on top of CareShield Life pay-outs. |

Choice from $1,200 to $5,000 in increments of $100. Benefit given includes pay-outs from CareShield Life. |

Type of monthly disability benefit given |

Choice of level or escalating monthly benefit |

Level monthly benefit |

Monthly benefits payable for |

Lifetime |

Lifetime |

Pay-outs start from |

Inability to perform 2 out of 6 ADLs (Singlife CareShield Plus), or 3 out of 6 ADLs (Singlife CareShield Standard). |

Inability to perform 2 out of 6 ADLs. |

Initial lump sum benefit |

3 times the first monthly benefit |

3 times the monthly benefit (at least 2 out of 6 ADLs), or 6 times the monthly benefit (at least 3 out of 6 ADLs) |

Entry age (Age Last Birthday basis) |

Age 30 to 64 |

Age 30 to 64 |

Source: https://www.careshieldlife.gov.sg/content/dam/cshl/pdf/COMPARISON%20OF%20CARESHIELD%20LIFE%20SUPPLEMENTS%20(03%20Oct%202023).pdf

Q: Can I purchase multiple CareShield Life supplements if I want higher coverage?

A: Yes, this is possible. You may purchase more than 1 CareShield Life supplement if desired.

Q: Can I pay for my CareShield Life supplements with MediSave?

A: You may pay for your premiums using your MediSave for up to $600 per insured person per calendar year. Premiums exceeding this limit will have to be paid in cash.

Q: What is the difference between CareShield Life and ElderShield?

A: There are three main differences between the two schemes, namely:

CareShield Life offers a monthly disability benefit that is expected to increase over time until age 67 or when a successful claim is made, whichever is earlier. Once activated, this monthly disability benefit will remain fixed and be payable for the duration of the severe disability. ElderShield however, offers a fixed monthly benefit of $300 or $400, and this will only be payable for 60 or 72 months, dependent on the plan chosen.2

While ElderShield excludes coverage for individuals who have pre-existing disabilities, CareShield Life will cover all Singaporeans and Permanent Residents (born in 1980 or later) regardless of their pre-existing disability or illness.3

Singaporeans who are born in 1980 or later are automatically enrolled into CareShield Life on their 30th birthday and will not be able to opt out from this scheme. This is unlike ElderShield which was an optional scheme and can be opted out of.

CareShield Life |

ElderShield |

|

Entry Age |

Age 30 |

Age 40 |

Is enrollment compulsory? |

Yes, from age 30 onwards. |

No. Enrollment can be opted out of. |

Monthly disability benefit |

Starting pay-out of $649 in 2024, and is expected to increase over time until age 67 or when a successful claim is made, whichever is earlier |

$300 (ElderShield 300) or $400 (ElderShield 400) |

Duration of pay-outs |

For duration of severe disability |

For up to 60 (ElderShield 300) or 72 months (ElderShield 400) |

Premiums |

Premiums is expected to increase over time until age 67. |

Premiums are determined at age of entry and will not increase with age. |

Eligibility for coverage |

Includes individuals (born in 1980 or later) with pre-existing disabilities. |

Excludes individuals with pre-existing disabilities. |

Q: I am currently on ElderShield, can I enhance my coverage with CareShield Life supplements?

A: Yes, you can choose to enhance your ElderShield coverage with a CareShield Life supplement. Enhancing with CareShield Life supplement will offer you with a more comprehensive coverage for your long-term care needs.

Plans available for such arrangements are: Singlife CareShield Standard and Singlife CareShield Plus plan.

*Terms and Conditions: 20% PREMIUM DISCOUNT PROMOTION FOR SINGLIFE CARESHIELD STANDARD AND SINGLIFE CARESHIELD PLUS

If you are a Singapore Citizen or Permanent Resident born between 1970 and 1979, covered under the ElderShield 400 scheme and did not develop severe disability at the point of auto-enrolment, you would have been auto-enrolled into CareShield Life from 1 December 2021.

For those born before 1970, or are still currently on the ElderShield scheme, you may also wish to consider switching to join the CareShield Life scheme instead.

(Read more: Should I switch from Eldershield to CareShield Life?)

Save more when you insure with FSMOne

Enjoy up to 45% commission rebates when you apply through us

Available Products on FSMOne Insurance |

Term Life, Whole Life, Critical Illness, Annuity, Health, Endowment, General Insurance (Personal and Commercial) from AIG, Allianz, Cigna, Chubb, Etiqa Insurance, FWD Insurance, Great Eastern, Henner, Income, Manulife, MSIG, Raffles Health Insurance, Singlife, Sompo, Tokio Marine, and QBE. *Please check with our team if the product you want is available on FSMOne Insurance |

Information obtained from:

1Source: https://www.straitstimes.com/singapore/half-of-careshield-life-beneficiaries-are-in-their-30s

2Source: https://www.careshieldlife.gov.sg/faqs/eldershield.html#:~:text=Depending%20on%20the%20plan%20you,(under%20ElderShield%20400%20plan).

3Source: https://www.careshieldlife.gov.sg/faqs/careshield-life.html

4Source: https://www.careshieldlife.gov.sg/careshield-life/benefits.html

Disclaimer:

All materials and content found in this article are strictly for information purposes only and should not be considered as an offer or solicitation to transact in any product.

This article is not a contract of insurance.

Insurance products are underwritten by the respective insurance partners and distributed by iFAST Financial Pte Ltd (“iFAST”). You are advised to read the precise terms, conditions and exclusions specified in the relevant policy contract.

This comparison does not include information on all similar products. iFAST does not guarantee that all aspects of the products have been illustrated. You may wish to conduct your own comparison for products that are listed in www.comparefirst.sg

You are advised to read the key product documents, including (but not limited to) the product summary, before deciding whether the product is suitable for you. You should consider carefully if the products you are purchasing are suitable for your financial objectives, experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of a product, please seek advice from a financial adviser before making a decision to purchase the product.

As buying a life insurance policy is a long term-commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid.

While iFAST and/or any of its third-party providers has/have tried to provide accurate and timely information, there may be inadvertent omissions, inaccuracies, and typographical errors. Opinions expressed herein are subjected to change without notice. This advertisement has not been reviewed by Monetary Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")