' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

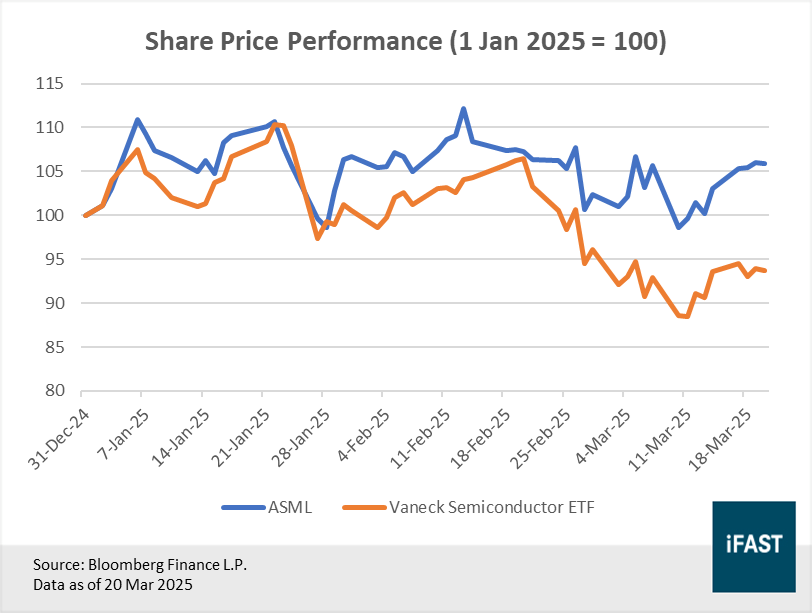

• ASML’s shares demonstrated their resilience, rising 4.8% year-to-date while the broader semiconductor industry saw a decline of more than 7% on aggregate (as of 20 Mar 2025).

• 2024 total net sales reached a record high of EUR 28.3 billion, mainly due to an increase in installed base management sales which rose 15.6% year-on-year to EUR 6.5 billion. Net system sales saw a marginal decline.

• Last year, ASML shipped the three high NA EUV systems (new EUV model) – two of which have been installed and are operational at a customer site. The company has also received purchase orders for the new model from all its existing EUV customers.

• As demand surges, supply will also have to expand accordingly to keep pace. We see rising wafer capacity and EUV exposures as two important factors behind greater lithography spending.

• We believe that ASML’s shares are still attractive, with an estimated upside potential of 60% (as of 20 Mar 2025). This represents a target price of USD 1,180.

Global equity markets stumbled into 2025, with most major US equity indices in the red. The semiconductor industry is no exception, as the VanEck Semiconductor ETF fell more than 7% year-to-date (as of 20 Mar 2025). ASML’s shares managed to buck the trend, rising 4.8% over the same period (Figure 1).

Figure 1: ASML’s shares have risen 4.8% year-to-date

Market volatility surged in the early months of the year, driven largely by uncertainty surrounding Trump’s constantly changing trade policies, leaving investors unsettled.

Over the past few weeks, the Trump administration placed tariffs on some of its largest trading partners like Canada and Mexico, only to reverse them a few days later. February’s consumer confidence reading plunged while inflation expectations surged, as investors fear a full-blown trade war could push the world’s largest economy into recession.

Earlier in January, the launch of low-cost Chinese AI model DeepSeek made waves in the AI industry, raising questions about the need for huge investments in training large language models. This development also contributed to the selloff in the share prices of western chip companies, while having the opposite effect on the Chinese chip sector.

But despite all the negativity, we believe that ASML’s recent performance has less to do with fundamentals and more to do with shifting investor sentiment. We reiterate our stance that ASML is a fundamentally strong yet undervalued company, and we urge investors to increase their position while valuations are still attractive.

Solid 4Q24 performance and full year results

ASML announced a strong set of results in late January. In 4Q24, total net sales increased by 24% year-on-year to EUR 9.3 billion. Growth was primarily driven by the installed base business and revenue recognition on the first two high NA EUV systems (ASML’s next-generation EUV machines).

For the full year, total net sales reached a record high of EUR 28.3 billion. Although net system sales saw a marginal decline (-0.8%), installed base management sales rose 15.6% year-on-year to EUR 6.5 billion. This increase is due to the growing installed base of systems and higher lithography tool utilisation levels for certain customers.

Net income fell 3.4% year-on-year, partly due to the lower number of units sold and higher research and development (R&D) spending. The company has previously warned that 2024 will likely be a year of transition, as customers delay investments due to uncertainties about the economy.

Table 1: ASML’s 2024 financial highlights

|

4Q23 |

4Q24 |

% Change |

2023 |

2024 |

% Change |

|

|

Total Net Sales |

7,237 |

9,263 |

28.0% |

27,558 |

28,262 |

2.6% |

|

Net System Sales |

5,683 |

7,116 |

25.2% |

21,938 |

21,768 |

-0.8% |

|

Installed Base Management Sales |

1,555 |

2,147 |

38.1% |

5,619 |

6,494 |

15.6% |

|

Net Income |

2,048 |

2,693 |

31.5% |

7,839.0 |

7,571.6 |

-3.4% |

|

Source: Company data. Data as of 31 Dec 2024 Figures are in EUR millions unless otherwise stated. |

||||||

Across the year, ASML has returned EUR 3 billion to shareholders through a combination of dividends and share buybacks. It aims to distribute a higher dividend over time, paid on a quarterly basis.

Strong emphasis on R&D & well-developed product pipeline crucial catalysts for future growth

As it stands, ASML is still the sole producer of EUV lithography machines. On top of that, it also commands a market share of approximately 90% in the DUV space. ASML's dominance in the lithography market stems from its strong focus on R&D.

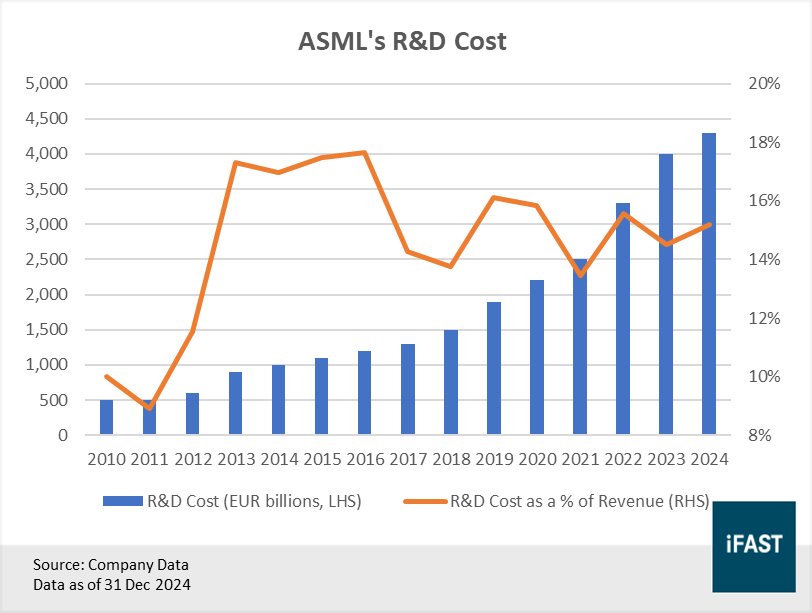

As mentioned in the previous article, more than a third of its employees work in R&D, making it the largest business unit by headcount. Demonstrating its relentless pursuit for innovation, ASML has poured EUR 4.3 billion into R&D in 2024, compared to EUR 4.0 billion the year before (Figure 2). This amount equates to roughly 15.2% of its total net sales, a slight increase compared to 2023.

Figure 2: ASML places heavy emphasis on R&D

ASML has consistently advanced its product pipeline. In 2024, the company shipped three high NA EUV systems, two of which have already been installed and are operational at a customer fab with volume production expected to commence in 2025/2026. These new machines are an evolutionary step in EUV technology. Not only do they enable higher wafer throughput than/versus previous generations, they also support greater transistor shrink, allowing chipmakers to produce sub 2nm chips.

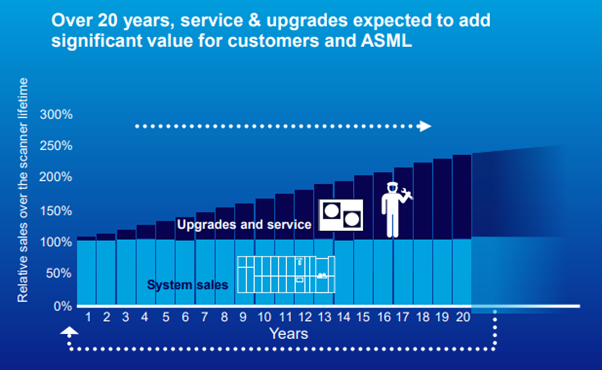

According to management, ASML has already received purchase orders for its high NA EUV system from all its existing EUV customers. This should provide a major boost to its revenues once the bookings are realised. Besides net system sales, an expanding installed base also provides ASML with plenty of opportunities to increase its net service and field option sales – a recurring source of revenue that contributes to its long-term financial stability and growth.

Based on projections by the company, the revenue generated by upgrades and services can exceed more than half the sale price of the machine by year 7/8. Typically, these machines have long lifespans of anywhere between 10 to 30 years – which increases the amount of service revenue ASML can potentially earn over its lifetime (Figure 3).

Figure 3: Net service and field option sales to be a key source of revenue as installed base grows

Source: Company Data

Structural megatrends accelerating chip & lithography demand

Besides the company’s unmatched tech leadership, the long-term outlook for semiconductors remains upbeat, backed by structural megatrends such as AI and the continued digitalisation of the global economy. As of 4Q24, the industry has experienced five consecutive quarters of positive sales growth, with the latest figure coming in at 19.7% year-on-year.

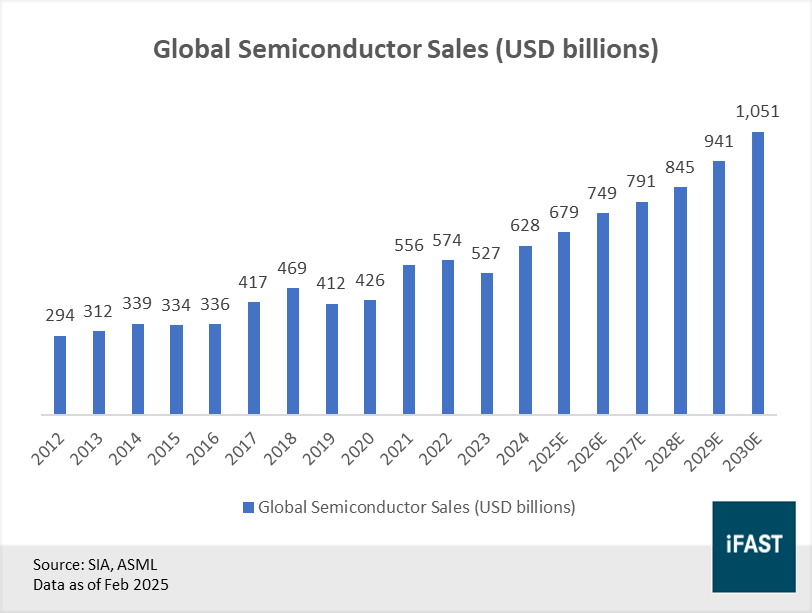

Looking ahead, semiconductor sales are projected to surpass USD 1 trillion by 2030, making this a golden decade for chipmakers (Figure 4). Among the various end markets, datacenters and automotive are widely expected to be key pillars of growth, benefiting from rising AI adoption, the shift to electric vehicles and increasing computational demands. Cutting-edge chips have higher silicon content and will require more EUV exposures, which translates to higher lithography spending—a clear tailwind for ASML.

Figure 4: Global chip sales projected to surpass USD 1 trillion by 2030

As demand surges, supply will also have to expand accordingly to keep pace. Based on estimates by the company, the number of wafer starts per month will increase by 35% over the next five years to reach 15.1 million by 2030. This supply expansion will be aided by public sector programs, such as the US and European CHIPS act. Late last year, Japanese Prime Minister Shigeru Ishiba unveiled a USD 65 billion plan to boost the country's chip and AI industries.

Chipmakers have responded positively, with the likes of TSMC and SK Hynix among the many targeting higher spending this year. TSMC in particular, is seeking to increase its capex by as much as 41% in 2025 to USD 42 billion. Close to 70% of this amount will be spent on advanced technologies, which will likely entail significant investments in EUV lithography machines.

More than 60% potential upside for ASML

Turning our attention back to the fundamentals, we note that ASML is in a strong financial position, underpinned by substantial revenue growth and profitability. The company also boasts a robust balance sheet, with cash and cash equivalents far outweighing total debt, resulting in a net debt to equity ratio of -36.3 as of end 2024. This strengthens ASML's ability to weather downturns. A significant portion of its cash is parked in highly liquid, short-term investments, such as money market funds, which should deliver solid returns given the current interest rate environment.

In terms of valuations, little has changed since our previous update. ASML is still expected to deliver strong double-digit earnings growth over the next three years. The company is trading slightly under 20X (based on its 2027 earnings estimates), well below our assigned fair multiple of 32X. This translates to an upside potential of around 60% (as of 20 Mar 2025) and a target price of USD 1,180.

Altogether, we believe that ASML remains a fundamentally strong yet undervalued company, backed by its (i) unassailable lead in EUV technology, (ii) immense potential for greater revenue growth and higher profitability, and (iii) robust balance sheet. These factors make ASML (NASDAQ:ASML) a compelling long-term investment. Investors with a long-term horizon may consider building a position while valuations remain attractive.

Table 2: ASML expected to see strong earnings growth in the coming years

|

2024 |

2025E |

2026E |

2027E |

|

|

EPS (EUR) |

21.23 |

24.21 |

29.38 |

33.70 |

|

EPS growth |

3.01% |

14.04% |

21.35% |

14.70% |

|

PE Ratio |

32.43 |

27.78 |

22.89 |

19.96 |

|

Upside Potential (based on 32X multiple) |

- |

- |

- |

60.36% |

|

Target Price |

- |

- |

- |

USD 1,180 |

|

Source: Bloomberg Finance L.P. Data as of 20 Mar 2025 |

||||

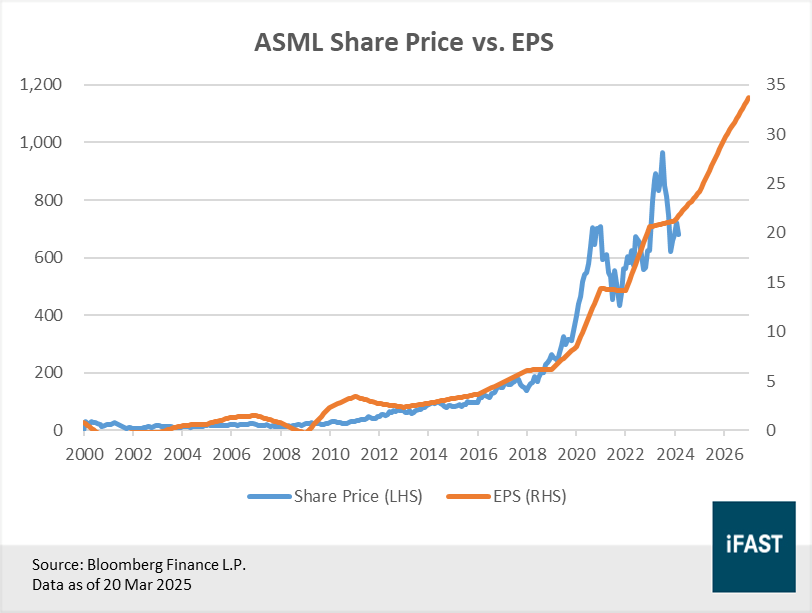

Figure 5: Share prices are driven by earnings in the long run

Related Article: ASML: Crash in share price is a window of opportunity for long-term investors.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in ASML.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")