' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

• ASML is a leading supplier of lithography equipment. It is currently the only producer of EUV lithography machines and holds a market share of roughly 90% in the DUV space.

• ASML’s shares underperformed the broader semiconductor sector this year, posting a loss of -5.8% vs a gain of nearly 40% for the Vaneck Semiconductor ETF. Shares plummeted by -15% after the company announced third quarter earnings, where it lowered its forecast for 2024 revenue and bookings.

• We like ASML for its unchallenged leadership in lithography. Its next generation EUV machines are expected to be released in the next two years, which should provide a major boost to its revenues.

• ASML’s growing installed base increases the potential for higher installed base management sales, which is also an important source of revenue in addition to net system sales.

• At their current valuations, we believe that ASML’s shares are undervalued, with an estimated upside potential of 45% (as of 22 Nov 2024). This represents a target price USD 974.

Company overview

ASML (NASDAQ:ASML) is a leading supplier of lithography equipment, which is a critical component used in semiconductor manufacturing. The company is best known for its groundbreaking extreme ultraviolet (EUV) lithography machines, which its clients (such as TSMC and Samsung) utilise to manufacture their most high-end chips. At the time of writing, ASML is the only producer of EUV machines.

Besides EUV, the company also produces Deep Ultraviolet (DUV) lithography machines, which is essentially just a less advanced version of the EUV. But even in the DUV space, ASML holds a commanding position, with an estimated market share of nearly 90%. Two of its rivals, Japanese companies Nikon and Canon make up the majority of the remaining market.

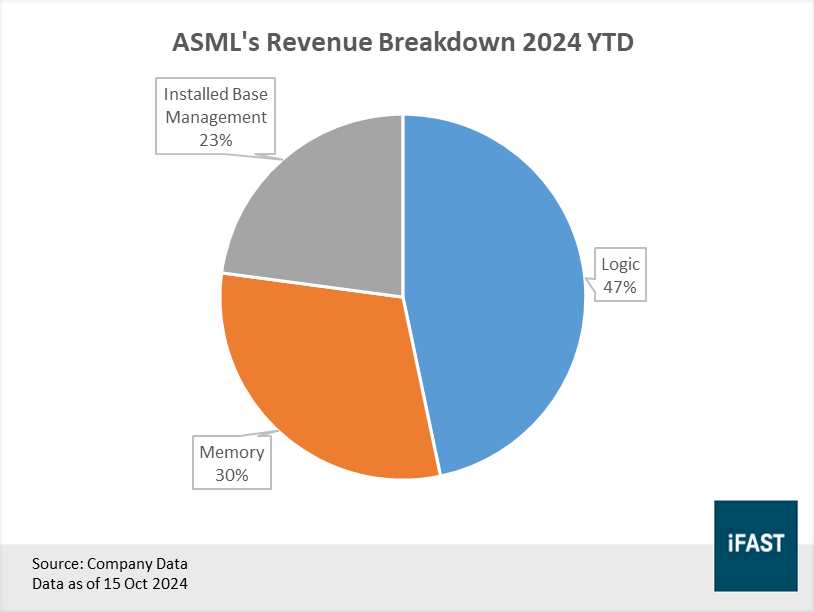

ASML has two main sources of revenue – net system sales and installed base management sales. Based on its latest quarterly earnings, net system sales accounts for approximately 77% of its total revenue, while installed base management sales makes up the remaining 23% (Figure 1). In the recent years, revenue growth for net system sales was largely driven by logic sector, mainly due to the heavy demand for AI related applications.

Figure 1: ASML derives the bulk of its revenue from net system sales

Net system sales consist of the sale of new as well as used systems. Besides selling new systems, ASML is also actively involved in the used system market, often buying back and refurbishing older systems before selling them to new customers.

Installed base management sales on the other hand, consists of net service as well as field option sales. The former refers to the revenue generated from a range of services (e.g. technical support, repairs and regular maintenance) for machines that are already deployed at customer sites to ensure optimal performance, while the latter refers to the sale of optional upgrades and enhancements for these machines.

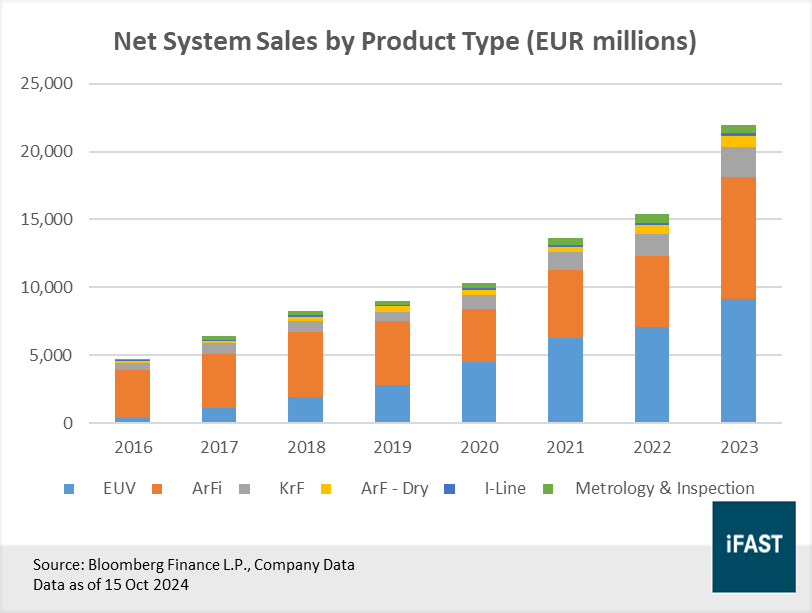

In terms of geographical exposure, ASML generates a significant portion of its revenue from Asia, where two of its biggest clients – TSMC and Samsung are based. Since EUV machines were first made commercially available by ASML in 2016, it has grown to become one of the most vital products in their lineup, contributing to roughly 41% of the company’s net system sales in 2023 (Figure 2).

Figure 2: ASML’s revenue broken down by product type

Shares down as investors disappointed by third quarter results

In mid-October, ASML released its third quarter results. Total net sales came in above guidance at EUR 7.5 billion, marking a 12% year-on-year increase. Of the total, net system sales made up EUR 5.9 billion, while installed base management sales made up the remainder. Net income exhibited a similar trend, rising 9.7% over the same period (Table 1).

Table 1: Key financial highlights

|

3Q23 |

3Q24 |

% Change (YoY) |

|

|

Total Net Sales |

6.67 |

7.47 |

11.99% |

|

Net Income |

1.89 |

2.08 |

10.05% |

|

Net Bookings |

2.60 |

2.63 |

1.15% |

|

Source: Company Data Data as of 15 Oct 2024. All figures are in EUR billions unless otherwise stated |

|||

Net system bookings for the quarter came in at EUR 2.6 billion, significantly below analysts’ estimates. The company also adjusted its guidance for 2025 total sales to the lower end of its initial estimate (now EUR 30-35 billion) citing headwinds in other market segments outside of AI. ASML’s CEO said that the sector’s recovery is more gradual than previously expected, which is leading to customer cautiousness and the delayed timing of its top end EUV machines. The prospect of tighter export restrictions was also a factor.

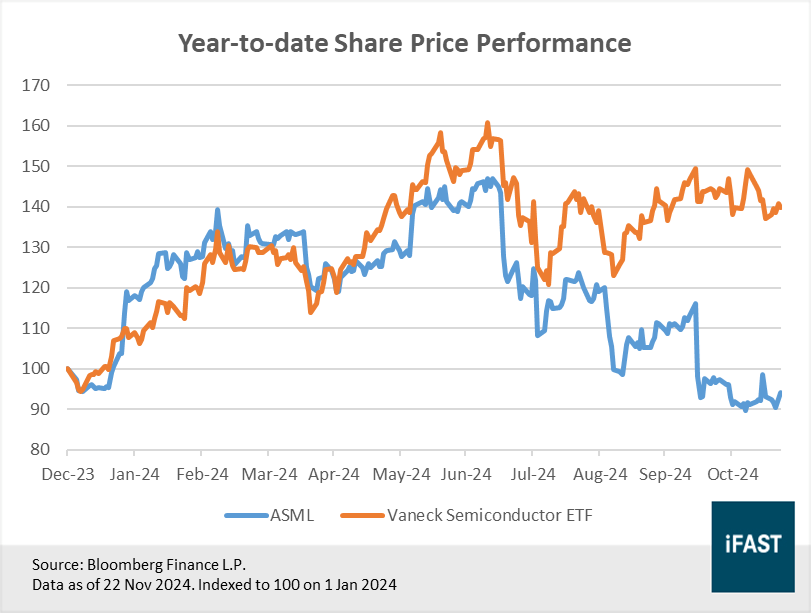

Investors reacted to the news negatively, sending the company’s shares -15% lower immediately after results were announced. ASML’s shares have now fallen nearly -40% since its peak in July. On a year-to-date basis, ASML has also underperformed the broader semiconductor sector, posting a loss of -5.8% vs a gain of nearly 40% for the Vaneck Semiconductor ETF (Figure 3).

We believe that the market’s short-sightedness has driven investors to overreact, thus creating an opportunity for long-term investors. In the following paragraphs, we will outline why ASML is well-positioned for success.

Figure 3: ASML’s shares have underperformed the broader sector year-to-date

Why we believe ASML is well-positioned for success

There are many reasons to like ASML, but the most compelling one has to be its unchallenged leadership in lithography. As mentioned in the beginning, ASML is currently the sole supplier of EUV lithography machines. In addition, it even has a market share of approximately 90% in the DUV space. At this juncture neither Canon nor Nikon have plans to develop their own EUV technology, which effectively makes ASML a monopoly.

Chipmakers who wish to produce sub 10 nm chips will only have one option, and that is to purchase their equipment from ASML.

The company’s heavy emphasis on Research & Development (R&D) over the past 40 years has allowed it to establish itself as the undisputed leader in lithography. On average ASML spends roughly 10-15% of its revenue on R&D each year. In 2023 the company spent a total of EUR 4 billion, an increase of 22.3% over the previous year. Of that amount, ASML has dedicated 10% to pure explorative research, focused on fuelling future innovation.

To build up its R&D expertise, ASML collaborates closely with universities, research institutions and even its customers. As of end 2023, ASML has over 15,600 full time employees working in R&D, representing 36.7% of its entire workforce - the largest share among all business functions, underscoring ASML’s commitment to R&D as a top priority. Though it has taken the company nearly a decade to bring the first EUV prototype into high volume manufacturing, the next generation EUV machines (EXE platform) will be ready in just three years.

ASML expects the new machines to start supporting high-volume manufacturing in 2025/2026. The company has also received purchase orders from all existing EUV customers for the newer model, which should provide a major boost to its revenues when the bookings are realised.

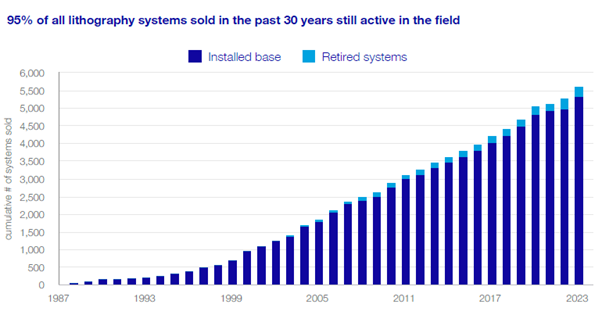

Beyond selling these high-cost machines, over the years ASML has also developed a sustainable and growing business model focused on servicing and maintaining them, which is a source of recurring revenue. ASML’s machines have a very long lifespan. The company estimates that 95% of all lithography systems sold in the past 30 years are still active in the field (Figure 4).

Figure 4: With a growing installed base, ASML has plenty of opportunities to increase its services revenue

Source: Company DataData as of end 2023

As these machines get older, they will have to be serviced regularly to ensure that they can continue to operate effectively. ASML also provides numerous field upgrade options, designed to improve machine capabilities without the need to replace the entire system – for its customers meet new production standards or to increase output.

The main point here is that with a growing installed base, the company has plenty of opportunities to increase its services revenue. ASM projects that its installed base management sales will double by 2030, which equates to a CAGR of 13% from today.

Last but not least, ASML is in a strong financial position, underpinned by substantial revenue growth and profitability. The company also has a healthy balance sheet, with minimal debt and a net cash position, putting it in a good position to navigate the higher for longer interest rate environment.

Key investment risks

While there are many positive things to say about ASML. Investors should also be aware of the potential risks this company faces.

Geopolitical risk: The relationship between US and China has been rocky in the recent years and is unlikely to thaw with Donald Trump taking office again in January 2025. As tensions between US and China escalate, export controls are becoming more common. However, these restrictions mainly apply to the most advanced chipmaking equipment, which Chinese foundries do not utilise for now. Demand from ASML’s major clients outside of China is also robust enough to offset losses from the Chinese market.

Customer concentration risk: The chipmaking industry is highly concentrated, with only a handful of companies that possess the ability to manufacture the most advanced chips. In 2023, two of ASML’s largest clients accounted for more than half its revenue. If something untoward happens to either of them, ASML will no doubt be affected.

Innovation & tech leadership: ASML’s lead in the lithography space is built on its technological edge, particularly in EUV technology. However, maintaining this technological edge requires continuous investment in R&D. If ASML fails to keep pace with technological advancements, it could lose market share. However, the risk is relatively low at this point, considering that its competitors do not have plans to develop their own EUV technology.

ASML’s shares are undervalued following the selloff

Following the selloff, valuations for ASML have become much more attractive than before. The company is currently trading at just 21X 2026 estimated earnings, way below its historical average of 33X over the past 10 years. We see this as a rare window of opportunity for investors to buy into this historically expensive stock.

We assign a fair PE multiple of 32X for ASML, which is in line with its 10-year average but well below the level its shares have been trading at over the past five years. This translates to an upside potential of around 45% (as of 22 Nov 2024) for ASML. This represents a target price of USD 974.

Although the company has projected for a measured recovery in 2025, we expect to see a strong multi-year growth trajectory for ASML moving forward, powered by its next generation EUV machines and larger installed base, which increases the potential for services revenue to grow consistently over time, alongside net system sales.

In our opinion, the market’s pessimism over its latest forecast has resulted in ASML’s shares becoming unfairly valued, presenting a compelling opportunity for longer term investors to capitalise on. Those seeking a high growth yet attractively priced stock should pay close attention to ASML (NASDAQ:ASML).

Table 2: ASML expected to see strong earnings growth in the coming years

|

2023 |

2024E |

2025E |

2026E |

|

|

EPS (EUR) |

19.89 |

19.43 |

24.38 |

30.40 |

|

EPS growth |

40.81% |

-2.31% |

25.48% |

24.69% |

|

PE Ratio |

38.06 |

34.63 |

27.60 |

22.13 |

|

Upside Potential |

- |

- |

- |

44.57% |

|

Source: Bloomberg Finance L.P. Data as of 22 Nov 2024 |

||||

Figure 5: Earnings are the key driver of share prices in the long term

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position ASML.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")