' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

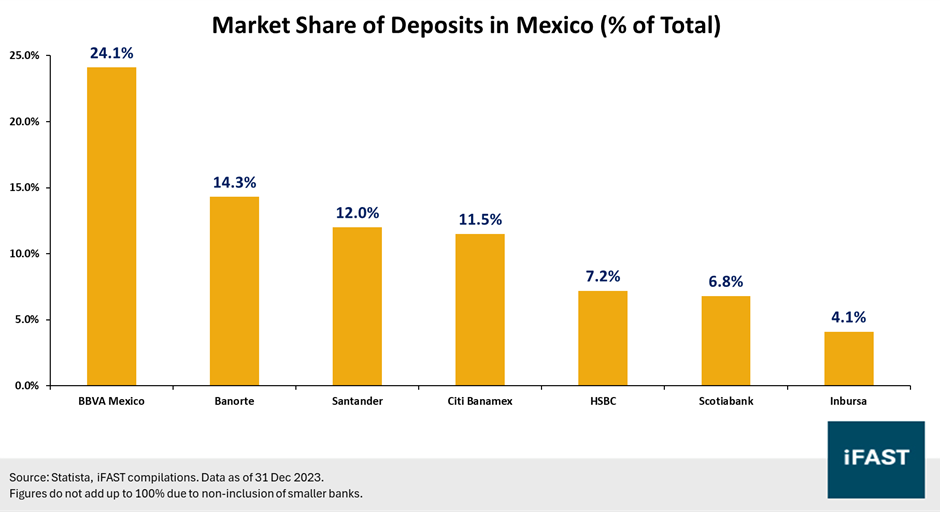

BBVA Bancomer, or BBVA Mexico, is part of the multinational BBVA Group, and is also one of the largest financial institutions in Mexico. It is the number one bank in terms of deposits (Chart 1) and is classified as a domestic systematically important bank in Mexico.

We look at the profile of BBVA Mexico and its various USD bonds, following its recently-released 3Q24 results. While these bonds are technically issued by ‘BBVA Bancomer Texas’, this entity essentially refers to BBVA Mexico. Its business operations are primarily in Mexico, and importantly, it will primarily be regulated by the CNBV in Mexico in terms of capital requirements.

Chart 1: BBVA Mexico is a market leader in Mexico’s banking sector

Operational highlights

(Unless otherwise stated: Results are in Mexican pesos [MXN]. Results are for 9-month 9M24 period from January 2024 to September 2024. Growth figures are YoY.)

BBVA Mexico generally expanded its operations over the past 12 months (Table 1). Its number of employees (+4%), branches (-3%), and ATMs (+1%) remained fairly stable, but what was more impressive was the +19% YoY increase in total financial transactions and the solid increase in its number of customers over a year (29.9m in 3Q23 to 32.3m in 3Q24). Both of these showcased the increasing digitalisation of the business, with mobile and web transactions, as well as mobile customers, both accounting for even larger majorities of the total pie over the past year.

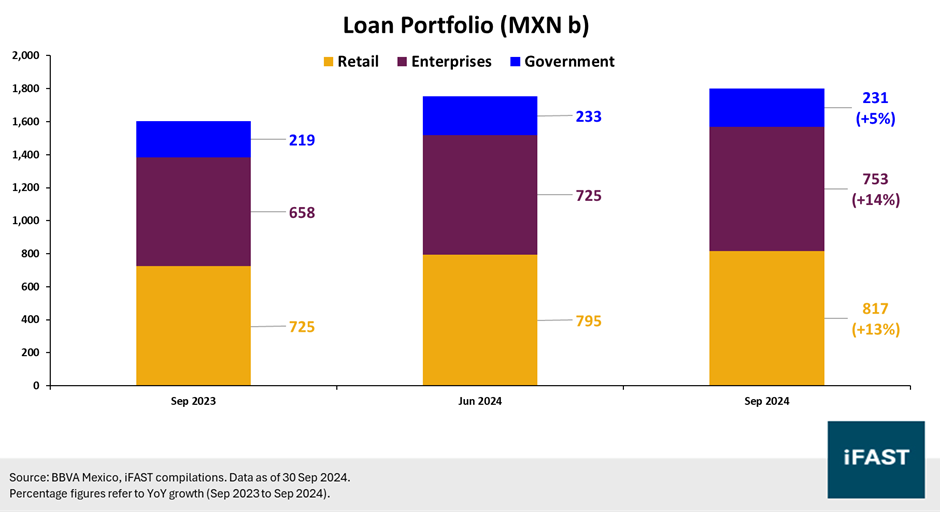

In addition, BBVA Mexico managed to grow its loan portfolio by a sizeable amount. Its loan portfolio is split into three main segments: retail (consumer and mortgage), enterprises, and government (financial entities and government entities). BBVA Mexico saw broad increases (double-digit percentage YoY) in loans across its two core retail and enterprises segments (Chart 2).

Table 1: BBVA Mexico grew its customer base and continued to see more transaction activity across the past year

| Operational Metrics | Sep 2023 | Sep 2024 | YoY Change* |

| Employees | 43,894 | 45,733 | +4% |

| Branches | 1,740 | 1,693 | -3% |

| ATMs | 14,417 | 14,619 | +1% |

| Mobile / Web Transactions (m, % of total) | 1,669 (64%) | 2,137 (69%) | +468 (+5pp) |

| Total Transactions (m) | 2,596 | 3,077 | +19% |

| Mobile Customers (m, % of total) | 21.4 (72%) | 24.4 (76%) | +3.0 (+4pp) |

| Total Customers (m) | 29.9 | 32.3 | +8% |

| Source:

BBVA Mexico, iFAST compilations, iFAST estimates. Data as of 30 Sep

2024. *YoY change refers to percentage growth from Sep 2023 to Sep 2024. Exceptions for mobile transactions and customers, where we show the absolute change in customers, and the change in percentage of mobile (of total). |

|||

Chart 2: Loan portfolio saw strong broad-based growth

Profit highlights

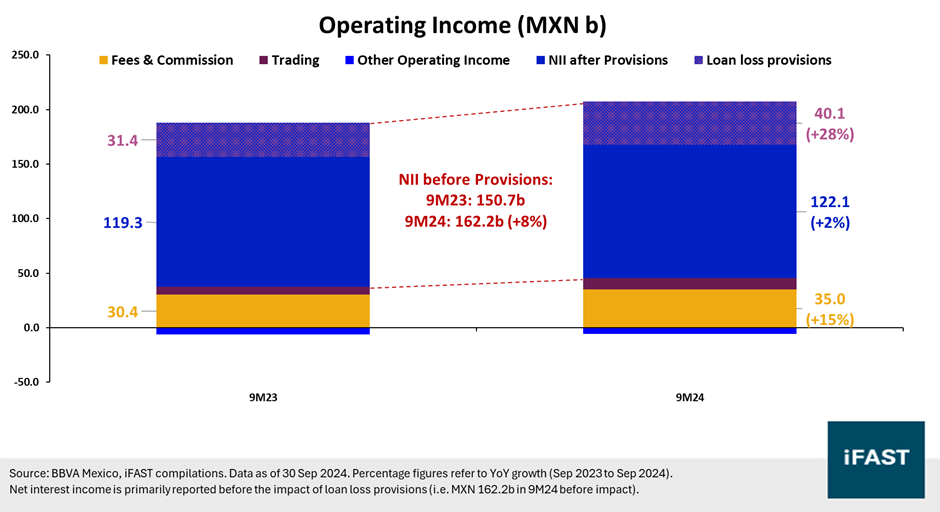

BBVA Mexico’s revenues primarily come from net interest income (NII) (Chart 3), as one of Mexico’s largest providers of loans to retail and wholesale clients. Net interest income grew by +8% from MXN 150.7b in 9M23 to MXN 162.2b in 9M24. This was primarily due to the growth in loan portfolios described above, though net interest margins (NIM) also expanded slightly in the same period.

Despite this, BBVA Mexico recorded significantly more loan-loss provisions as its loan portfolio grew: provisions were reported at MXN 40.1b in 9M24, +28% higher than the MXN 31.4b in 9M23. Management has attributed this to larger provisions required in the consumer and cards sub-segments, while they also mentioned last quarter (2Q24) that they were in the midst of ‘cleaning up’ their retail portfolio. We do not find this overly surprising – the retail segment is traditionally ‘riskier’ and requires larger provisions. Breaking down BBVA Mexico’s loan and provisions balances, we similarly observe the majority of additional provisions came from the ‘consumer’ and ‘credit card’ sub-segments. Consequently, net interest income less loan-loss provisions saw flattish growth of +2% to MXN 122.1b in 9M24.

Apart from NII, net fees & commission income was also a big growth driver, up by +15% to MXN 35.0b in 9M24. BBVA Mexico saw broad-based increases across the various segments supported by higher volumes, both in the cards (credit & debit) and investment funds sub-segments. For fees specifically, BBVA Mexico also revealed it was a market leader within the mutual funds space with a market share of 24.9% (as of September 2024), with fund balances growing by +24.1%.

With the decent growth in NII and net fees & commission income described above, total operating income for BBVA Mexico grew by a decent +7% YoY to MXN 162.0b. However, with non-interest expenses also increased increasing by a similar amount, both income before taxes (+5%) and net income (after taxes) (+5%) grew by a smaller extent, to MXN 97.0b and MXN 70.5b respectively.

To summarise, we think BBVA Mexico’s profits remained resilient in 9M24. While there were clear headwinds such as NIM pressures and higher loan loss provisions, these remain within our expectations, and we do not see any red flags for now.

Chart 3: Fees & commission income and net interest income were two main drivers of operating income

Outlook (and risks)

(Unless otherwise stated: Guidance is provided by BBVA Group [the listed entity], but will refer to the Group’s Mexico segment [i.e. BBVA Mexico] unless otherwise stated.)

BBVA has provided guidance on interest sensitivity: a +100bps parallel shift in yields is expected to have an approximately +2.5% impact on NII and vice versa, of which +1.6% will arise from higher Mexico rates and the remaining +0.9% from higher USD rates. However, the negative impact described above (arising from NIM pressures) is expected to be offset by higher loan volumes: BBVA has previously guided for double-digit loan book growth, which is something they have delivered so far in 9M24.

Officially, BBVA expects high single-digit percentage NII growth (‘close to 10%’), a piece of guidance they have reiterated in 3Q24. We think this NII growth guidance (single-digit percentage) is a realistic target for BBVA Mexico. Market expectations for FY24 indicate about 90bps worth of cuts priced in in the US, and about 125bps worth of cuts in Mexico (including those that have already occurred). Based on the +2.5% figure from the sensitivity analysis above, we think that if BBVA Mexico can maintain its double-digit growth in its loan book, then it remains on track to hit its NII growth target.

In terms of loan loss provisions, we highlighted above that the YoY increase observed in 9M24 was primarily driven by retail segments like ‘consumer’ and ‘credit card’. These tend to be higher-risk but also higher-yielding segments for BBVA Mexico. We think the increase in provisions is expected as BBVA Mexico grows its loan book; looking ahead, we expect provisions to continue increasing even into 2025 and beyond, though likely at a slower rate than the recent +28% figure once management is done with its loan book ‘clean up’.

Apart from interest rates, we think it is also important to look at Mexico’s growth outlook, considering the cyclicality of BBVA Mexico’s business (loans). BBVA has guided (latest data as of 2Q24) that on GDP sensitivity: a -100bps shock to GDP growth would lead to higher expected credit losses of EUR 100m, or approximately MXN 2.2b (based on spot rate as of 12 November). In addition, a slowdown in economic growth could have other impacts like loan portfolio growth (which has been an important driver of NII recently).

We acknowledge near-term growth uncertainties from still-restrictive monetary policy and external factors like the US elections; however, we note that forecasts from Banxico and IMF point towards continued positive GDP growth in 2024 and 2025. Mexico also remains a key beneficiary of tailwinds related to nearshoring which could support the Mexican economy. Management has highlighted nearshoring as a longer-term tailwind for the country and they expect this trend to continue under the new President (sworn in in October). Consequently, we think that on balance, we do not expect the growth backdrop in Mexico to have a severe negative impact on BBVA Mexico’s profitability, particularly in the longer term.

To summarise, we think BBVA Mexico’s profit outlook remains decent. While there are potential headwinds arising from falling rates and various macro uncertainties, we think that BBVA Mexico can remain resilient given its strong market position. We also think the issuer remains on track to hit its FY24 NII guidance (single-digit percentage growth), and it should be able to remain profitable in the coming years (even if profit levels technically fall from FY23).

Credit highlights

BBVA Mexico’s asset quality remained decent. Its non-performing loans (Stage 3 loans, or NPL) ratio came in at 1.7% in 3Q24, remaining fairly stable compared to the previous quarter (2Q24: 1.6%) or a year before (3Q23: 1.6%). Its coverage ratio (i.e. allowances for loan losses divided by NPLs) fell slightly but remained healthy at 192% (2Q24: 199%).

BBVA Mexico also provided a detailed breakdown of its (performing) loans portfolio and provisions, with risk levels ranging from A1 to E. 77% of the BBVA Mexico’s loan balance was classified under the lowest risk category A1 (2Q24: 76%) and 6% was classified under category A2 (2Q24: 5%). It was in the higher-risk categories (e.g. B2 to C1), where the percentage of total loans fell slightly. To us, these indicate that the average risk level of its performing loans appears stable over the past quarter.

We highlight that its loan-to-deposit ratio has crept up over the past year to 104% (101% in 3Q23, and 105% in 2Q24) suggesting slightly higher risks, but think this remains manageable with BBVA Mexico still retaining healthy access to funding through traditional deposits given its market position, as well as through wholesale funding as evidenced from the various issuances across the past year. Its net stable funding ratio was reported at 125%, slightly lower than 129% in 2Q24.

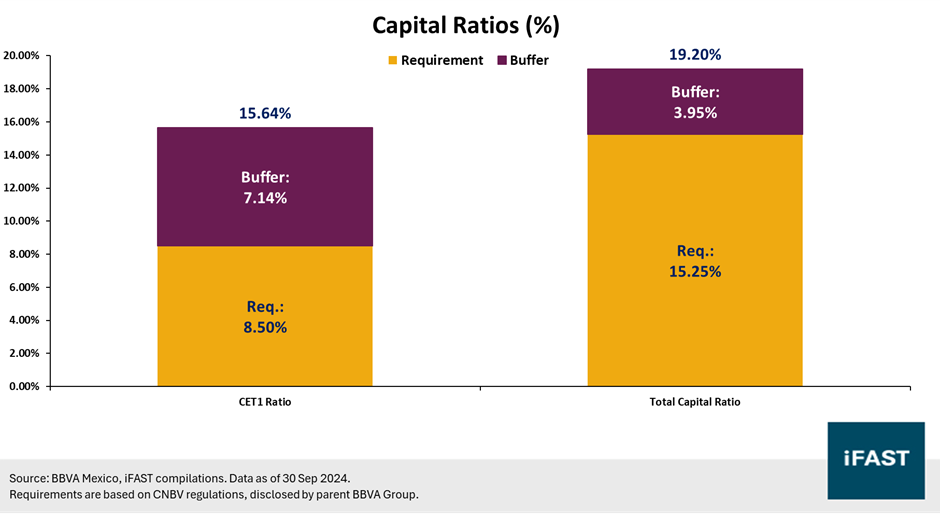

BBVA Mexico remains well-capitalised based on its published capital ratios (Chart 4). Its CET1 ratio was reported at 15.64%, slightly lower than 2Q24’s 15.75% likely contributed by the payment of dividends in September (MXN 15b), but still well above official regulatory requirements of 8.50%. In addition, its total capital ratio of 19.20% continues to have a decent buffer over the minimum 15.25%. However, total capital ratio requirements are slated to increase up to Dec 2025 (not disclosed by issuer, but assuming 1.625% for two more years, new requirements would be 18.50%) which could partially erode this buffer, though we expect BBVA Mexico to continue being able to generate organic capital through profits.

Summarising the above, we think BBVA Mexico is an issuer with sound credit fundamentals. This is especially considering the decent buffers it has for its explicit capital ratio requirements, though we will look more into other (less stringent) capital ratio requirements for coupon deferral and loss-absorption below.

Chart 4: BBVA Mexico remains well-capitalised

About the bonds

BBVA Mexico has several outstanding USD bonds, but we recommend their 2033 and 2034 Tier 2 bonds for their attractive yields. While the issuer itself is investment-grade (A3 by Moody’s, BBB by Fitch), the Tier 2 bonds are considered high-yield (BB) by Fitch due to subordination risks. We highlight some features of these Tier 2 bonds which investors should consider before purchasing these bonds.

Features of BBVA Mexico’s Tier 2 bonds

First, these Tier 2 subordinated bonds come with coupon deferral risks. The regulator CNBV may order corrective measures, including coupon deferrals, if BBVA Mexico’s capital ratios fall below their explicit requirements listed above (CET1 below 8.50%, total capital below 15.25%). In addition, mandatory coupon deferral will occur if BBVA Mexico’s CET1 ratio drops below 7.5% or total capital ratio drops below 9.5%. These deferrals will generally be cumulative unless directed otherwise by the regulator. We think coupon deferral looks unlikely given the issuer’s existing capital ratios, and track record in generating organic capital thus far.

Second, these Tier 2 subordinated bonds come with loss-absorption risks. Tier 2 instruments can be written down to supplement capital if BBVA Mexico’s CET1 ratio drops below 4.5%; Mexican regulators have also clearly stated that such write-downs must occur before authorities can step in to support the bank. Nonetheless, we think this scenario remains extremely unlikely, considering the issuer’s latest CET1 ratio of 15.64% has a strong buffer over the 4.5% threshold.

Tier 2 capital instruments in Mexico will be subject to amortisation (similar to those in several other jurisdictions) starting from 5 years to maturity: 100% for those over 5 years to maturity, and 20% each year after (0% if it matures in less than 1 year). Consequently, assuming BBVA Mexico maintains a decent outlook based on our expectations described above, we would expect it to call these bonds on their first call date (5 years before maturity).

Our recommendations

Compared with bonds from other Mexican bank issuers, these BBVA Mexico T2 bonds provide a yield pickup over Santander Mexico’s subordinated bonds, reflecting the former’s slightly lower rating. Meanwhile, their yields are just below those of Banorte’s subordinated bonds, reflecting BBVA Mexico’s slightly higher (Fitch) rating. We further highlight that BBVA Mexico is a larger player in Mexico compared to Banorte (#1 against #2), while the former has the prospect of some support from its parent BBVA Group in the unlikely event of distress.

Between BBVA Mexico’s bonds, we like that the T2 subordinated bonds offer attractive yield to calls of 7.25% (2033 bonds) and 7.14% (2034 bonds) respectively. Between these two bonds, we prefer the 2033 bonds for the shorter time to call, as well as their slightly higher nominal yields and spreads; nonetheless, the 2034 bonds may also appeal to some investors depending on their own investment needs and horizons. We think the yield pickup over its seniors appears attractive, considering its seniors are yielding just over 5% for 2 notches (higher) in credit rating. Nonetheless, the 2029 seniors may be suited for more risk-averse investors who wish to stick to investment-grade bonds.

Table 2: Mexican bank bonds (USD) - Recommendations bolded

| Bond Name | Call / Maturity Date (Years to Call / Maturity) |

Ask Price | Yield to Call / Maturity (%) | Credit Rating (S&P / Moody's / Fitch) |

| BBVASM 1.875% 18Sep2025 Corp (USD) | - / 18 Sep 2025 (- / 0.8) |

97.233 | - / 5.26% | - / A3 / BBB |

| BBVASM 5.250% 10Sep2029 Corp (USD) | 10 Aug

2029 / 10 Sep 2029 (4.7 / 4.8) |

99.230 | 5.44% / 5.43% | - / A3 / BBB |

| BBVASM 5.125% 18Jan2033 Corp (USD) | 17 Jan 2028 / 18 Jan 2033 (3.2 / 8.2) |

94.064 | 7.25% / 7.09% | BB / - / BB |

| BBVASM 5.875% 13Sep2034 Corp (USD) | 13 Sep

2029 / 13 Sep 2034 (4.8 / 9.8) |

94.905 | 7.14% / 7.77% | - / Baa2 / BB |

| BBVASM 8.450% 29Jun2038 Corp (USD) | 29 Jun 2033 / 29 Jun 2038 (8.6 / 13.6) |

105.332 | 7.59% / 7.93% | - / Baa2 / BB |

| BBVASM 8.125% 08Jan2039 Corp (USD) | 08 Jan

2034 / 08 Jan 2039 (9.2 / 14.2) |

103.384 | 7.60% / 7.82% | - / Baa2 / BB |

| BANORT 5.750% 04Oct2031 Corp (USD) | 04 Oct 2026 / 04 Oct 2031 (1.9 / 6.9) |

96.812 | 7.59% / 8.38% | - / Baa2 / BB- |

| BSMXB 7.525% 01Oct2028 Corp (USD) | - / 01 Oct

2028 (- / 3.9) |

105.633 | 5.87% | - / Baa2 / BBB- |

| Source: Bloomberg, Bondsupermart, iFAST compilations. Data as of

12 Nov 2024. Note: Some of the peer bonds above (non-recommendations) may not be available on our platform. |

||||

Declaration: For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

Our podcast series, Yield Hunters, is available on Spotify, iTunes Podcasts and Google Podcasts. We share our thoughts on new bond issues and hold discussions on the fixed income space. Listen to our latest episode below and follow us!

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")