' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Why Bonds Financing Now?

Few years ago, using leverage to invest in bonds would be potentially disastrous. Rising interest rates caused bond prices to fall, resulting in unrealised mark-to-market losses, while margin borrowing costs have also surged due to interest rates hike from central banks. It was a double whammy that made the strategy unviable – until now.

As central banks begin cutting rates around the world, this could potentially lead to (i) bond prices rising (capital appreciation), and (ii) reduction in margin borrowing costs when interest rates decrease. More importantly, financing allows you to free up your capital while seizing market opportunity by using debt strategically for positive carry trades, compared to using margin to engage in speculative short-term trades.

The Case for Bonds

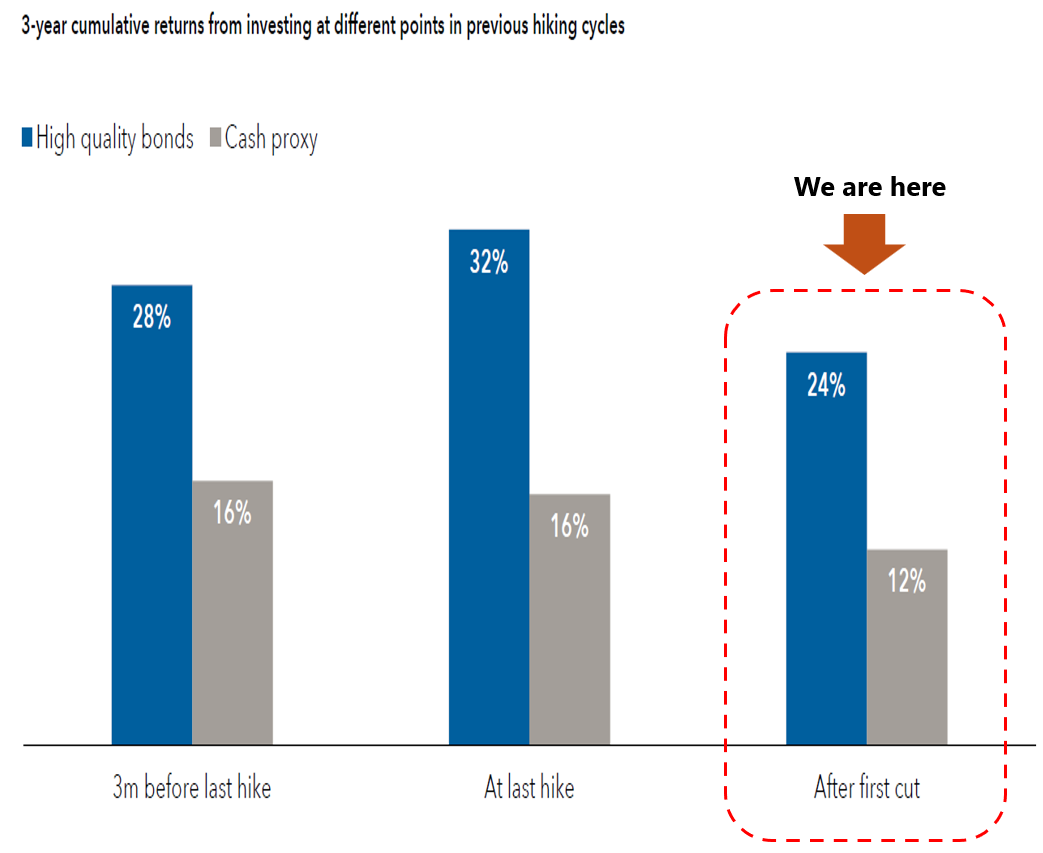

Source: Capital Group, Data as of September 2023. For illustrative purposes only.

Against the backdrop of a declining interest rate environment, if you are holding on to cash or similar proxies (e.g. money market funds), your potential returns over a 3-year cumulative period could fall short compared to investing in high quality bonds - by a factor of two times! Although returns might have been higher if you had invested during the last rate hike cycle, entering now after the first rate cut still offers an attractive proposition with a potential upside of 24% over a 3-year cumulative period.

Bonds vs Bonds Funds

In August, our article on whole-lot bond financing was published for investors looking to boost their income yield through financing whole-lot bonds. A great alternative for fixed income exposure is through bond funds, which require a much lower minimum investment amount (as low as S$1,000). Bond funds also offer greater diversification since it is comprised of a portfolio of multiple bonds compared to an individual bond.

Finally, the loan-to-value (financing quantum) is higher for bond funds at 71.43% (providing 3.5 times buying power), while loan-to-value for investment-grade bonds will depend on their credit rating (BBB- to AAA).

|

Bond |

Bond Fund |

|

|

Diversification |

Lower (Individual Bond) |

Greater (Diversified Portfolio of multiple bonds) |

|

Liquidity |

Lower, generally traded over the counter (OTC) on secondary market |

Greater, based on prevailing NAV of fund. |

|

Min. Investment Amount |

Higher,

|

Lower, As low as S$1000 |

|

Loan to Value (LTV) Ratio |

50% to 70%, Investment grade bonds & above only |

71.43%, Regardless of underlying bond rating under fund. |

Funds in Focus

To pair with this margin strategy, it is important to select bond funds with strong, sustainable dividend payout and healthy performance track record to capture the potential upside. This ensures that the positive-carry spread will not be compressed due to declining yields or capital erosion.

1. Pimco Income Fund CL E INC JPY-H (Div Yield: ~6.6%)

Pimco is a global leader in active fixed income management and its Income Fund was featured in FSM Choice Awards 2024 as the the top selling fixed income fund. The fund is well-diversified across multiple sectors in the US, with an average overall bond credit rating of AA- (investment grade and above), with securitised assets as its primary holdings.

As of 10 Oct 2024, the JPY-hedged share class offers a dividend yield of 6.6% p.a., with a positive carry spread well above 4.6% after deducting FSMOne JPY margin interest of 1.97% p.a. (or 1.5% with the preferential rate). The JPY-hedged share class has delivered a 3-month return of 1.03% and 4.72% over a one-year period. In comparison with the unhedged USD share class, the JPY-hedged share class will be subject to underperformance due to the hedging costs involved, which may affect the total returns.

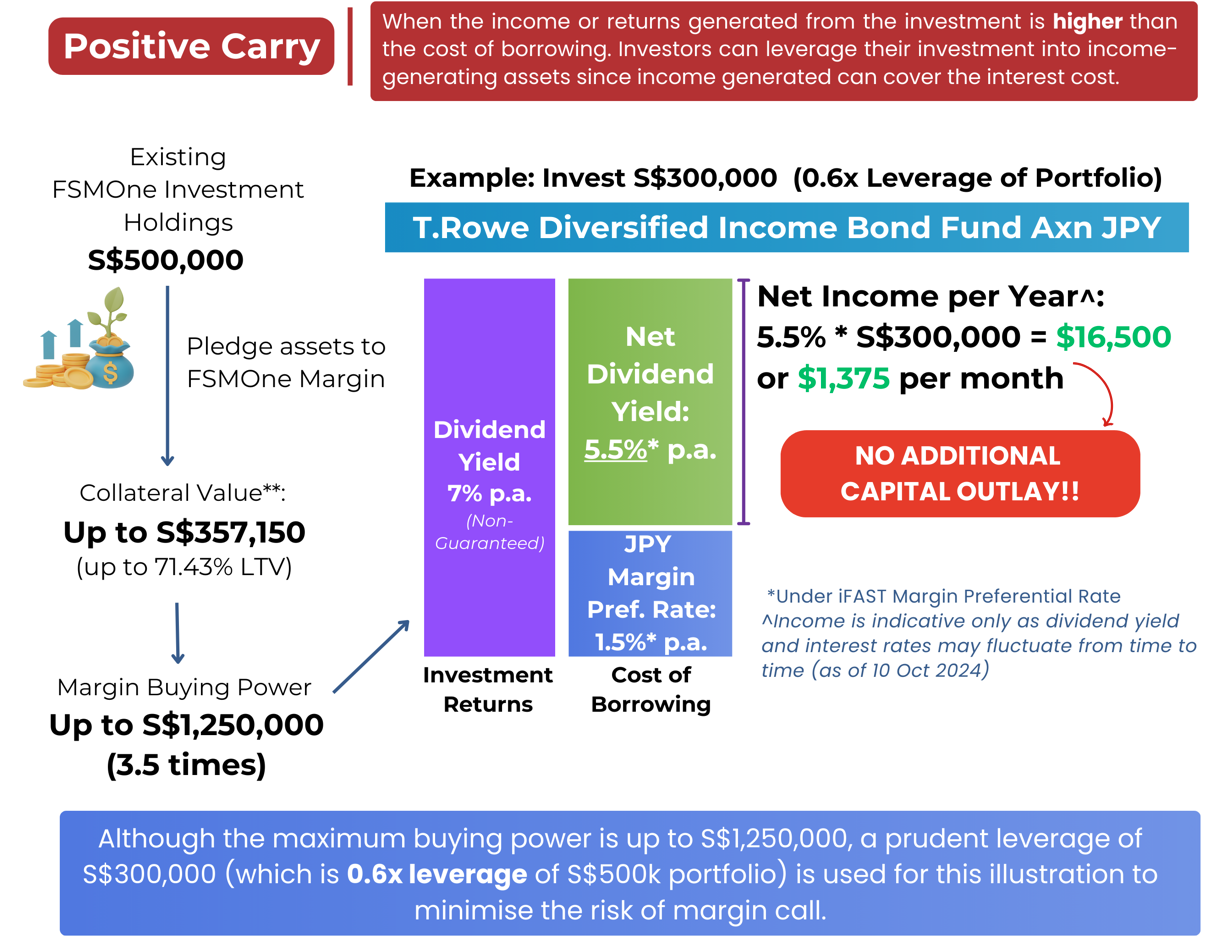

2. T.Rowe Price Diversified Income Bond Fund Axn JPY (Div Yield: ~7%)

The T.Rowe diversified income bond fund holds a globally diversified portfolio of bonds from over 80 countries and 16 sectors, with an average overall bond credit rating of A (investment grade and above). The global exposure has enabled the fund to capture additional returns as central banks outside of the US have also begin cutting interest rates.

Recently, iFAST Research conducted a Q&A session with T.Rowe Price to understand their investment approach in constructing a diversified bonds portfolio and the sustainability of their dividend payouts. The fund’s dividend policy focuses on delivering sustainable income through active management without relying on capital payouts.

As of 10 Oct 2024, the JPY-hedged share class offers a dividend yield of 7% p.a., with a positive carry spread well above 5% after deducting FSMOne JPY margin interest of 1.97% p.a. (or 1.5% with the preferential rate). The JPY-hedged share class was newly incepted in July 2024 and has delivered a return of 0.97% since its inception. In comparison with the unhedged USD share class, the JPY-hedged share class will be subject to underperformance due to the hedging costs involved, which may affect the total returns.

Source: Bloomberg Finance L.P., iFAST Compliation Data as of September 2024.

Although the returns may appear modest, both funds in its original USD share class have significantly outperformed the benchmark over a 4-year period. This is evident that active management plays a crucial role in fixed income investment as compared to passive management (e.g. bond ETF), as the benchmark posted negative returns of over 12% over the same period. For income investors, this highlights the value of achieving positive returns while still receiving a stable investment income from the fund.

What Should I Know about Some Key Risks?

1) Market Risks

Bonds typically carry lower in risk and volatility compared to equities, making them ideal for income investors. While default risk is a key concern for bonds, bond funds help mitigate this by having a portfolio of well-diversified bonds.

Notwithstanding, the fund’s NAV can still fluctuate due to interest rates movement. Although interest rates are generally expected to decline, which would push bond prices up, we advise against excessive leveraging which poses significant margin call risk. To maintain a safety buffer and protect against market downturns, it is recommended to keep the margin ratio not more than 70%.

To recap, margin ratio is calculated by taking the account’s outstanding loan balance divided by total collateral value, expressed as a percentage. A margin call occurs when this percentage surpasses 100% and above, indicating a substantial decline in collateral value relative to the loan amount, where it necessitates the need to restore the margin ratio to below 100%.

2) Interest Risks

Since this is a JPY-hedged share class, investors would be borrowing in JPY to invest. Hence, margin interest rates would be impacted by Japan’s central bank policy, which has seen two recent rate hikes so far in 17 years (still relatively low compared to other countries).

The Bank of Japan has affirmed that they would take a slow and cautious approach since rapid rate hikes would adversely impact its economy. This strategy would remain favourable as the net dividend yield of this carry trade currently offers above 5% p.a.. If margin rates were to increase by an additional 1% next year, the net dividend yield would still exceed 4% p.a. which would remain highly attractive.

3) FX Risks

FX risk would be present when investors borrow in JPY and invest into a cross-currency investment e.g. USD bonds. However, in this hedged share class, FX risk between JPY and its base currency, USD, is largely mitigated by the fund’s portfolio manager, who uses derivatives such as currency forwards to hedge against currency movements between JPY and USD.

Hedging incurs costs that directly impact the JPY-hedged share class fund’s NAV (currently ~3% to 4%), reflecting the interest rate differential between USD and JPY. As a result, these costs will affect the total returns of the fund. However, the portfolio manager expects hedging cost to decrease in the medium term (to ~2%) as USD rates decline and JPY rates rise, reducing the impact on NAV performance.

Now that you have a clear understanding of the margin strategy, including its potential upsides and risk management techniques, you may be wondering how to get started with this margin trade.

Simplifying Margin Investments – Margin Payment Method

To recap, FSM accredited investors can complete the margin opt in process in only 7 seconds without the need for supporting documents or minimum asset balances (FSMOne App > Holdings > Margin Facility Enrolment).

Upon completion of opt in, you can invest using a new payment method – Margin, which will be available in the order cart. The margin buying power reflected is universal and will automatically convert to the investment currency you are purchasing (e.g. JPY-denominated fund > JPY Margin).

Contact our FSM Customer Services team to learn more about how you can obtain the iFAST Margin Preferential Rates!

Disclaimer:

The use of margin involves a high degree of leverage and

risk which can lead to losses as well as gains which are of a larger magnitude

as compared to the movement of a security or market. You should therefore

carefully consider whether such a financing arrangement and/or investment

products you are purchasing is suitable for you in light of your own financial

position, experience, objectives, ability to bear risks and other relevant

circumstances.

Investment products involves risk, including the possible loss

of the principal amount invested. Past performance is not indicative of future

performance and yields may not be guaranteed.

All materials and contents found in this advertisement are

strictly for information purposes only and should not be considered as an offer

or solicitation to deal in any capital market products. You should consider

carefully if the investment products you are purchasing are suitable for your

investment objective, experience, risk tolerance and other personal

circumstances. If you are uncertain about the suitability of the investment

product, please seek advice from a financial adviser, before making a decision

to purchase the investment products.

While iFAST and/or any of its third-party providers has/have

tried to provide accurate and timely information, there may be inadvertent

omissions, inaccuracies, and typographical errors. Opinions expressed herein

are subjected to change without notice.

This advertisement has not been reviewed by the Monetary

Authority of Singapore.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")