' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

As Japan has exited the negative interest rate era and implemented supportive policies to restore its position as a semiconductor powerhouse, investor interest in this market is burgeoning. If you have been keeping up with our research articles, you will have observed our upward revision of the star rating for the Japanese market to 4 stars since the start of last year. Throughout the past year, we have consistently provided insights by spotlighting noteworthy Japanese equity funds and articulating our investment outlook on the Japanese stock market.

Related article: Reasons to buy Japan and the yen after BOJ’s first hike in 17 years

However, a common pitfall we observe is investors blindly allocating funds based solely on a comparison of cumulative returns among Japanese equity funds on the platform. As illustrated (Fig 1), the top ten ranked Japanese equity funds all fall within the currency-hedged category (sorted by one-year cumulative returns).

Figure 1: Japanese Equity Funds on the platform (Sorted by one-year cumulative returns)

Nevertheless, the decision between currency-hedged and unhedged classes holds significant weight, potentially yielding notable disparities in investment returns. This piece aims to delve into the intricate role of currency hedging and its impact on investor returns. Furthermore, we will provide our insights on which class presents a more suitable choice for Japanese equity funds in the prevailing market conditions.

What is a currency-hedged share class fund?

Let us illustrate currency hedging with an example. Consider the case of the Allianz US High Yield Cl Am Dis H2-AUD. Despite investing in US high-yield bonds, this fund belongs to the AUD hedged share class category. This means it hedges the currency risk for investors who transact in Australian dollars.

Unlike a typical fund denominated in Australian dollars, the performance of this fund will not be affected by fluctuations in the AUD to USD exchange rate. This enables investors who invest using Australian dollars to achieve returns that closely mirror the actual performance of the US market.

How is currency hedging implemented?

After investors invest in a currency-hedged share class fund, the fund manager will convert the investor's capital from the hedged currency to the base currency that the fund is invested in. These funds are then used to purchase assets at the designated market.

Simultaneously, to hedge the investor's currency risk, the fund manager will utilise currency forward contracts. These contracts allow the fund manager to convert the agreed-upon investment amount in the base currency of the investment destination back to the hedged currency at a specified price on a specified future date. This specified price is known as the forward exchange rate.

Since the value of the futures contract is locked in, the fund's return is less exposed to potential currency exchange rate risks. Hence, the fund's holdings are only affected by fluctuations in asset prices. Considering that futures contracts typically expire within a month, the fund manager needs to update and roll over the currency hedging contracts at least once a month.

Examples of Hedged and Unhedged Share Classes of Japanese Equity Funds

It seems that the concept of currency hedging may be a little bit complex. Let us consider another example to further clarify the concept.

Let us take our recommended Japanese equity fund, Eastspring Investments – Japan Dynamic As SGD-H, as an example. This fund predominantly allocates its investments to securities of companies incorporated, listed in, or primarily operating in Japan. Being part of the SGD-hedged share class, it effectively mitigates currency risk for investors using Singapore dollars.

Commencing from March 2022, the US Federal Reserve embarked on a cycle of interest rate hikes. Singapore, as an interest rate taker, has also witnessed a significant surge in its interest rates over the past two years, resulting in a widening interest rate differential between Singapore and Japan. Consequently, the Singapore dollar has appreciated relative to the Japanese Yen. In addition to these interest rate differentials, Singapore's robust economy and consistent influx of foreign capital have also bolstered its currency.

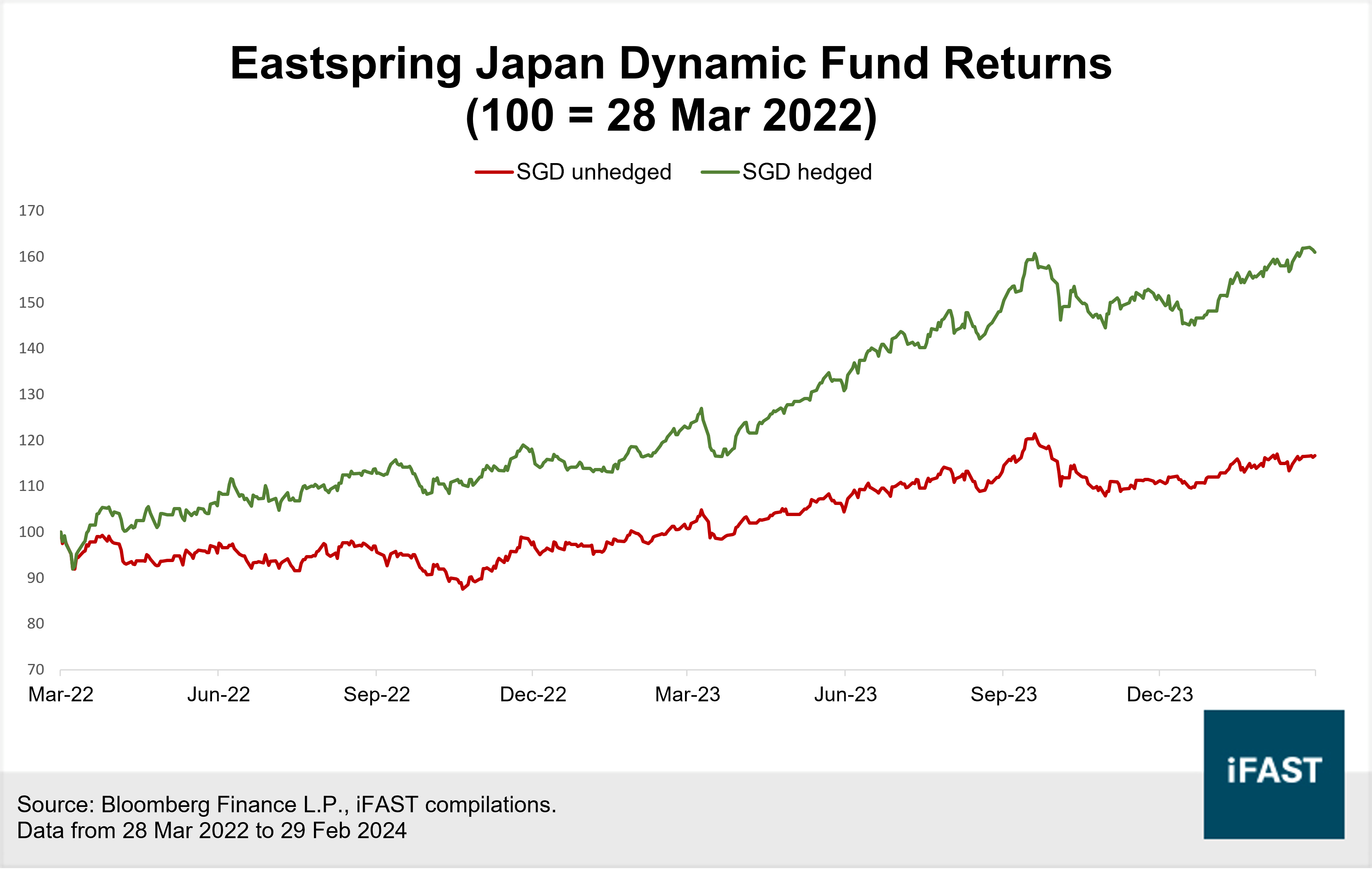

As such, Singapore dollar investors who opted for an unhedged share class in Japanese equity funds would have experienced substantial erosion in the returns of their Japanese stock investments due to the weakening Japanese Yen. This trend is evident in Figure 2, where the performance of the unhedged share class notably lagged behind the SGD-hedged share class.

In contrast, by investing in the SGD-hedged share class, the impact of Singapore dollar appreciation has been significantly mitigated. These observations are also apparent in Figure 2, Singapore dollar investors would have experienced returns more closely aligned with the actual returns of the Japanese stock market during that period, as demonstrated by the SGD-hedged share class.

Figure 2: During periods of Singapore Dollar appreciation, the SGD-hedged share class outperformed the unhedged counterpart

Exchange rate volatility can have a positive impact on investment returns

You might question whether investing solely in the hedged share class fund is enough to shield oneself from currency fluctuations. However, that assumption does not always hold. As discussed in the earlier example of currency hedging, opting for the hedged share class fund locks in the exchange rate. Yet, this also implies that investors cannot reap any benefits from potential appreciation in the exchange rate of the underlying market in which the fund is invested.

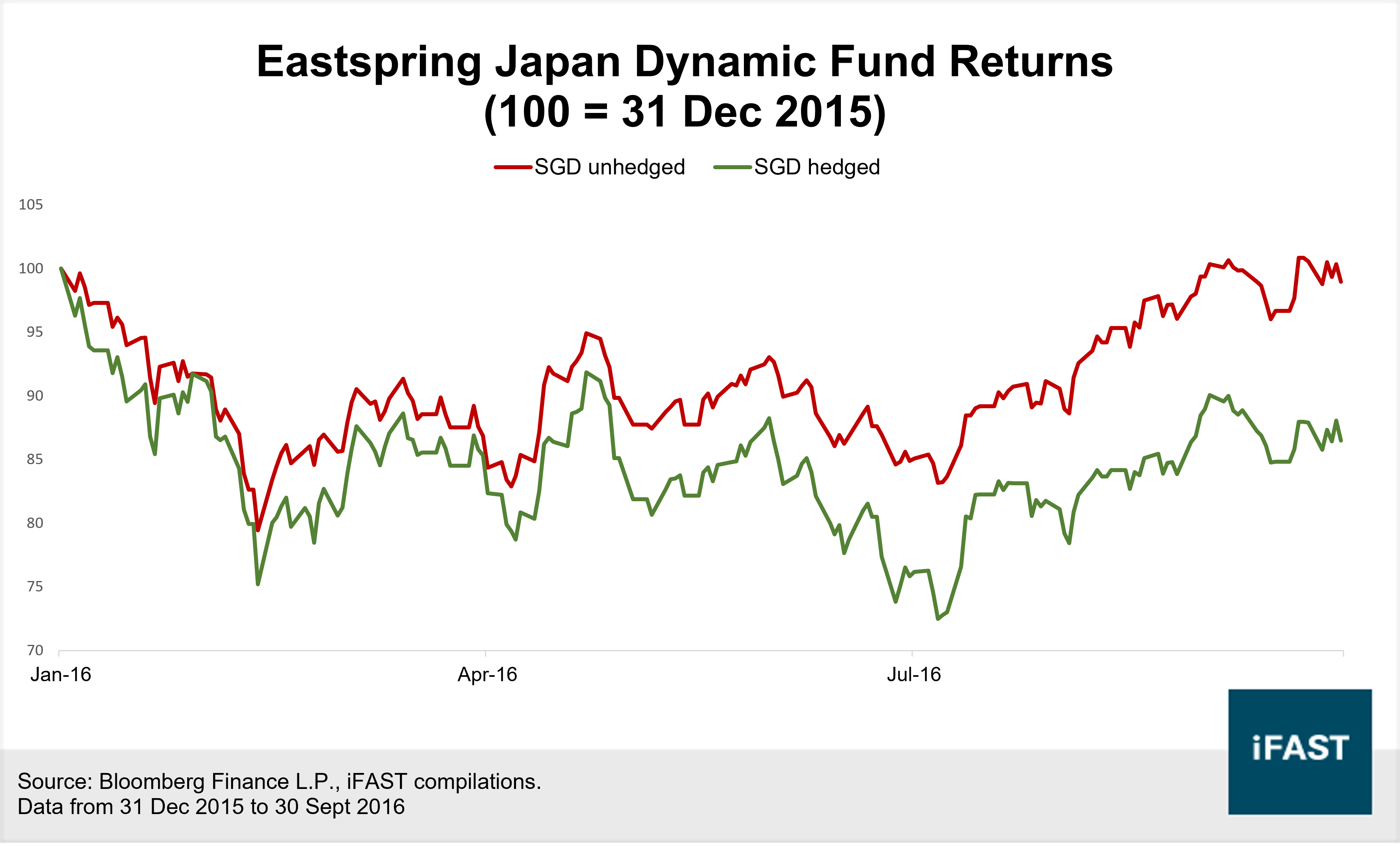

Let us delve further into the example of the Eastspring Investments - Japan Dynamic Fund discussed earlier. Examining Figure 3, spanning from 31 December 2015 to 30 September 2016, reveals a continued strengthening of the Japanese Yen exchange rate during this period. In such a scenario, for Singapore dollar investors, the unhedged share class of Japanese equity funds reaped the rewards of the Japanese Yen's appreciation, yielding higher returns compared to the hedged category.

In essence, the returns of the unhedged category not only reflect the performance of the underlying Japanese stock investment but also factor in the appreciation of the Japanese Yen. This dynamic enables the unhedged share class to outperform the hedged share class in terms of cumulative returns.

Figure 3: During periods of Japanese Yen appreciation, the SGD unhedged share class outperformed the hedged counterpart

Investment Insights

In summary, when investing in the Japanese market, there is not a single all-encompassing answer regarding whether to choose the hedged or unhedged share class. Choosing the hedged share class of Japanese equity funds can effectively mitigate the risk of Japanese Yen exchange rate fluctuations. However, the trade-off is that investors may potentially miss out on returns from the appreciation of the Japanese Yen. When the Yen appreciates, investments in hedged share class funds cannot benefit from the appreciation.

Nevertheless, given our optimistic outlook on the Japanese Yen, especially with Japan's exit from the negative interest rate era and the anticipated gradual narrowing of interest rate differentials between Japan and major countries, there is potential for Yen appreciation. Additionally, it is important to highlight that the Yen remains significantly undervalued, with the SGD/JPY exchange rate reaching its all-time high at above 112 as of 3 April 2024.

We recommend investors consider investing in the unhedged share class of Japanese equity funds. This approach not only captures the potential upside of the Japanese stock market but also enables investors to benefit from potential returns generated by the appreciation of the Japanese Yen. Investors seeking exposure to Japan may find Eastspring Investments - Japan Dynamic AS SGD a compelling option.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")