' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

• The cybersecurity market has been growing rapidly over the years but remains fragmented. Under such circumstances, one should look to market leaders.

• Fortinet is a market leader in multiple segments, due to its diversified business model, and its suite of products that creates cross-selling and up-selling opportunities.

• Fortinet has an impressive track record, consistently raking in profits and free cash flow over the years, and we foresee this to continue.

• The company has a solid growth trajectory in a fast-growing market with its suite of superior offerings and integrated solutions.

• Based on our fair P/E multiple of 35X, we arrive at a target price of USD 84 by the end of 2026, implying an upside potential of 24%. More risk adverse investors can consider the Global X Cybersecurity ETF (NASDAQ:BUG), which invests in the broader cybersecurity sector.

Cybercrime has become rampant in recent years, with losses soaring to more than USD 8 trillion in 2023 according to World Economic Forum. As the variety and sophistication of malware expands, the cost of each cyberattack has increased as well. The global average cost of a data breach has reached USD 4.45 million in 2023, an increase of 15% in just over three years. Looking ahead, as the world continues on its path of digitalisation and adoption of artificial intelligence (AI), we expect to see more cybercrimes, making cybersecurity more important than ever for both consumers and corporates alike.

Cybersecurity market remains fragmented, focus on the market leaders

The cybersecurity market is fragmented. It is made up of many segments ranging from infrastructure protection, network security, cloud security, and endpoint security to name a few. While some smaller cybersecurity companies may specialise in just one or two segments, most of the larger companies usually have solutions that span across multiple segments. For instance, Fortinet (NASDAQ:FTNT) offers not only network security solutions, but also multi-cloud security, endpoint and device protection as well as other services.

In such a fragmented market, we believe that looking at larger players or market leaders would be wise, due to their larger pool of capital and talents. Not to mention, these large players often have the means to acquire smaller players to further grow market share, such as the acquisition of Splunk by Cisco Systems in an all-cash deal seen in September 2023 and Broadcom’s acquisition of Symantec back in 2019.

Market capitalisation wise, some of the largest pure play cybersecurity companies include names such as Palo Alto Networks (USD 93 billion), CrowdStrike (79 billion), Fortinet (52 billion), and Zscaler (30 billion), as of 14 March 2024. While all four of them have demonstrated strong revenue growth rates, only Palo Alto Networks and Fortinet have a consistent track record of being profitable. With this in mind, we will take a closer look at Fortinet in this article.

Fortinet is a market leader in multiple segments with a diversified business model

Fortinet engages in cybersecurity solutions across both product and service segments, offering a wide range of networking products and cloud services (Table 1), suitable for users and clients across a diverse spectrum. Its business model can be broken down into three segments, namely:

1) Secure Networking (68% of revenue mix): Think of this segment as protection mechanisms to keep your digital networks safe from cyber intruders, just like how you protect your home from burglars using fences and locks. An example would be the firewall, which acts as a barrier between your network and the outside world. Another example would be virtual private networks (VPNs), which allows you to securely connect to your network from anywhere.

2) Unified Secure Access Service Edge (SASE) (21%): This segment acts as a gatekeeper which not only protects your network, but also manages how users can access it from anywhere at any time. This comprehensive solution is highly scalable and efficient due to cloud integration within its platform, and largely utilises a subscription-based model, which is stickier in nature and generates recurring revenue for Fortinet.

3) Security Operations (11%): In simple terms, this segment acts as a security team that continuously monitors your network for potential threats and respond swiftly to security incidents, while generating incident reports and analysing potential pitfalls in your network. Furthermore, it constantly evaluates its strategies and improve the defenses of your network.

Table 1: Comprehensive suite of products in each segment

|

Secure Networking |

Unified SASE |

Security Operations |

|

FortiGate Firewall FortiSwitch FortiAP FortiExtender FortiDDoS +more |

SD-WAN FortiClient FortiMonitor FortiWeb FortiProxy +more |

FortiAnalyzer FortiSandbox FOrtiSIEM FOrtiMail FortiRecon +more |

|

Source: Fortinet Investor Relations Presentation Data as of Feb 2024 |

||

While Fortinet does not typically provide a detailed breakdown of its revenue by hardware and software segments in its financial reports, it reports its revenue under broader categories such as product revenue and service revenue. Product revenue generally includes sales of hardware appliances, software licenses and related products, while service revenue encompasses subscription-based services, maintenance and support as well as professional services.

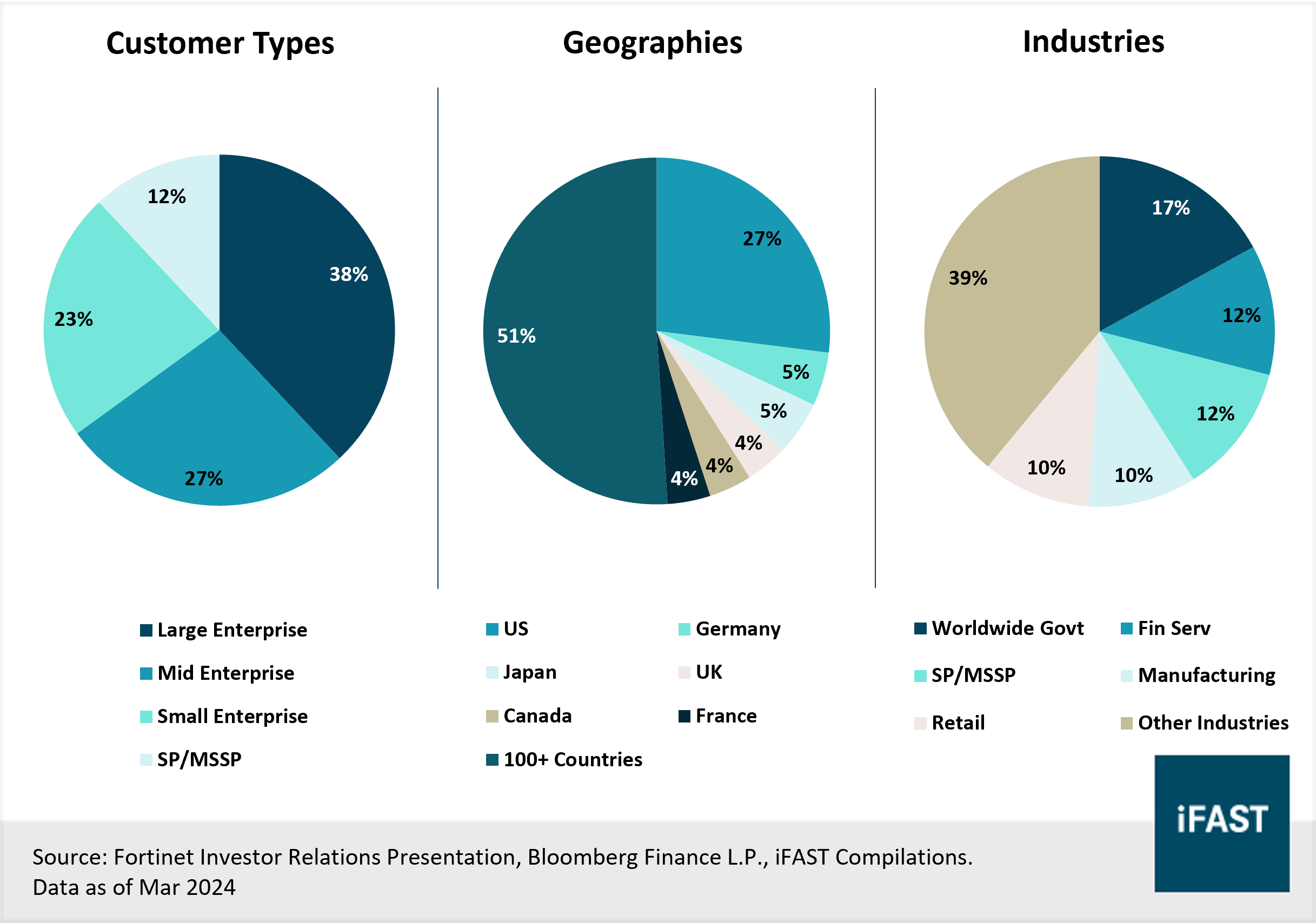

In addition to its wide range of products and services, Fortinet also has a diversified revenue stream, across customer types, geographies and industries (Figure 1).

Figure 1: Fortinet has a highly diversified business model

As Fortinet employs a hybrid business model, selling both software and hardware in its three business segments, it is able to enjoy network effects by cross-selling and up-selling. The hardware component for instance, plays a crucial role in establishing an ecosystem. Once a device is deployed at a customer's site, cross-selling becomes more seamless between products and services to existing customers, resulting in higher revenues and greater customer loyalty.

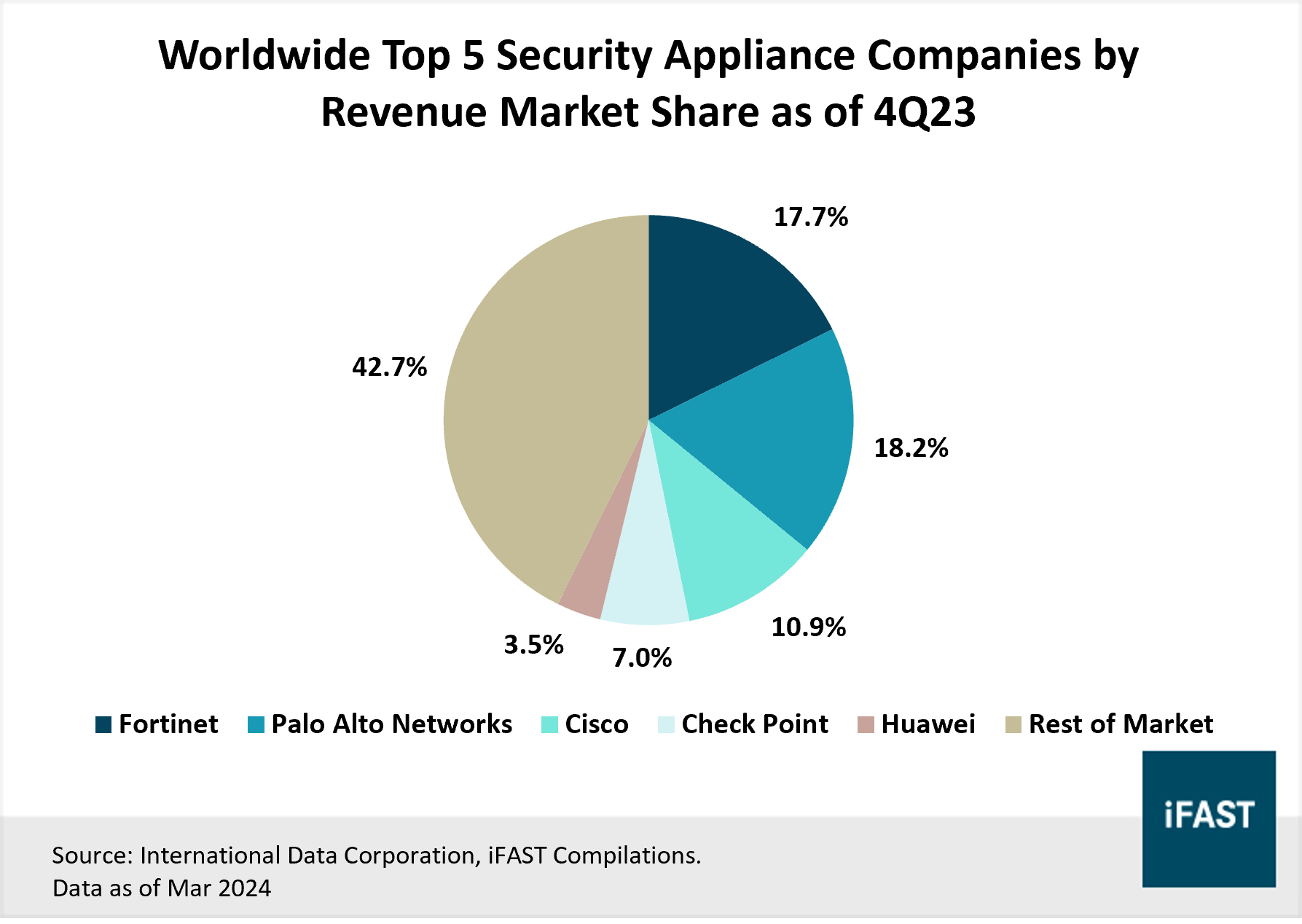

Moreover, it is also worth noting that Fortinet has a strong presence in the hardware market with security appliances, holding the second largest spot in terms of revenue at 17.7% on a global basis, as of end 2023 (Figure 2), and has been consistently ranking in the top two spots in the past few years, according to International Data Corporation.

Figure 2: Fortinet remains one of the market leaders

Solid growth trajectory with enormous total addressable market

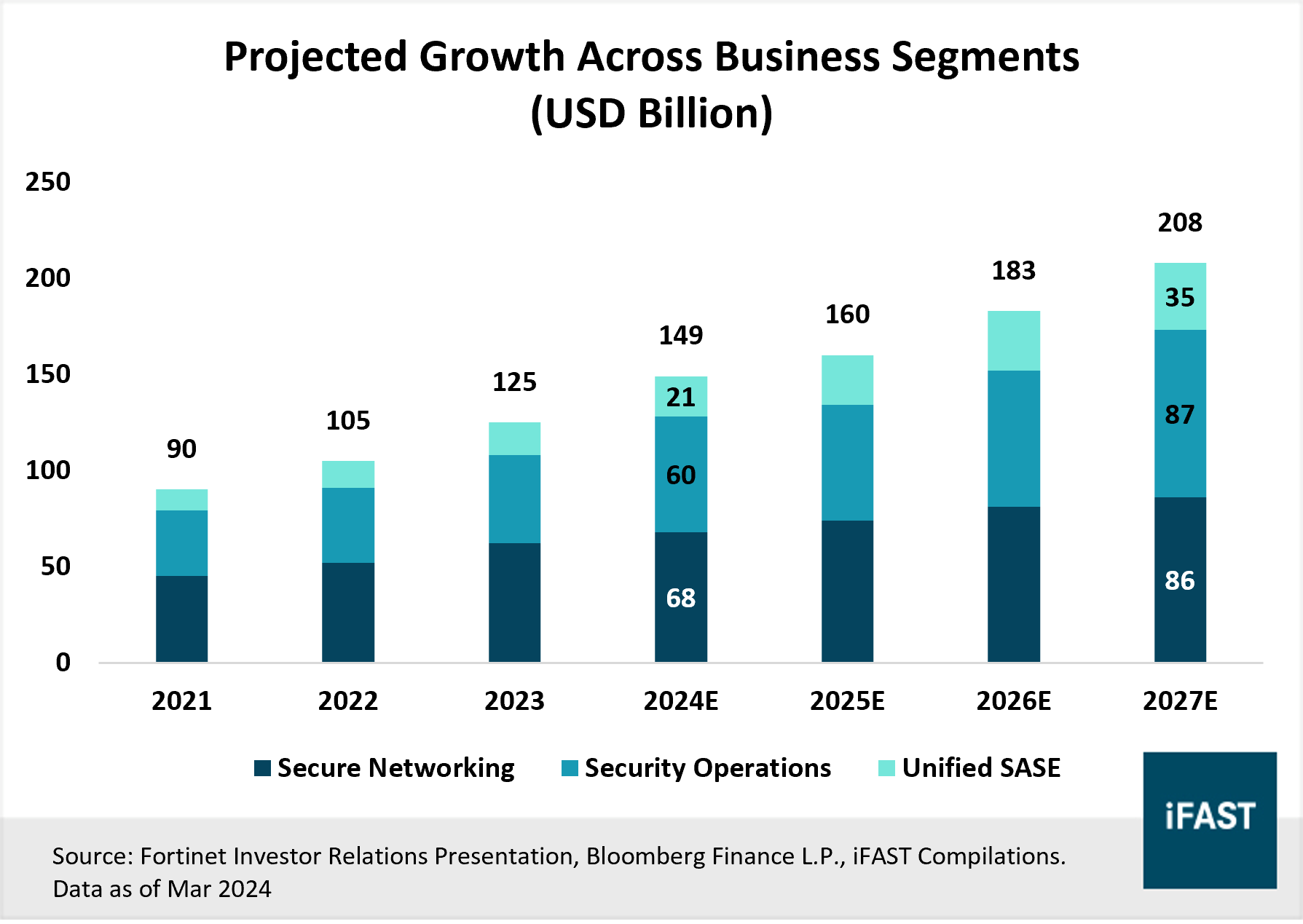

Moving ahead, we think that the long-term trajectory of Fortinet remains bright, with an enormous and growing total addressable market (TAM).

As of 2024, the TAM for Fortinet stands at USD 149 billion, with Secure Networking representing USD 68 billion, Security Operations at USD 60 billion, and Unified SASE at USD 21 billion, and this figure is set to expand to USD 208 billion by 2027, due to growing demand for cybersecurity solutions, driven by evolving threats, digital transformation, cloud adoption and regulatory compliance requirements, which would increase the demand for Fortinet’s suite of products and services.

Figure 3: Growing total addressable market (TAM) across all business segments

With a growing TAM, Fortinet is well-positioned to capitalise on this opportunity by leveraging on its suite of product and service offerings. Fortinet’s management also foresees the current product cycle slowdown to trough in early 2024, before moderating and accelerating towards 2H24 and into 2025, achieving double-digit growth in the upcoming years as the company transitions from shifting reliance from product revenue to service revenue.

The services segment, which is software-oriented, typically commands higher gross margins (82-87%) as compared to the products segment (56%-63%), which is more hardware-oriented. The services segment is also likely to experience faster growth due to the increasing shift of services to the cloud, or potentially AI-driven cyberattacks anticipated by customers, which will help Fortinet to grow its margins and result in higher earnings.

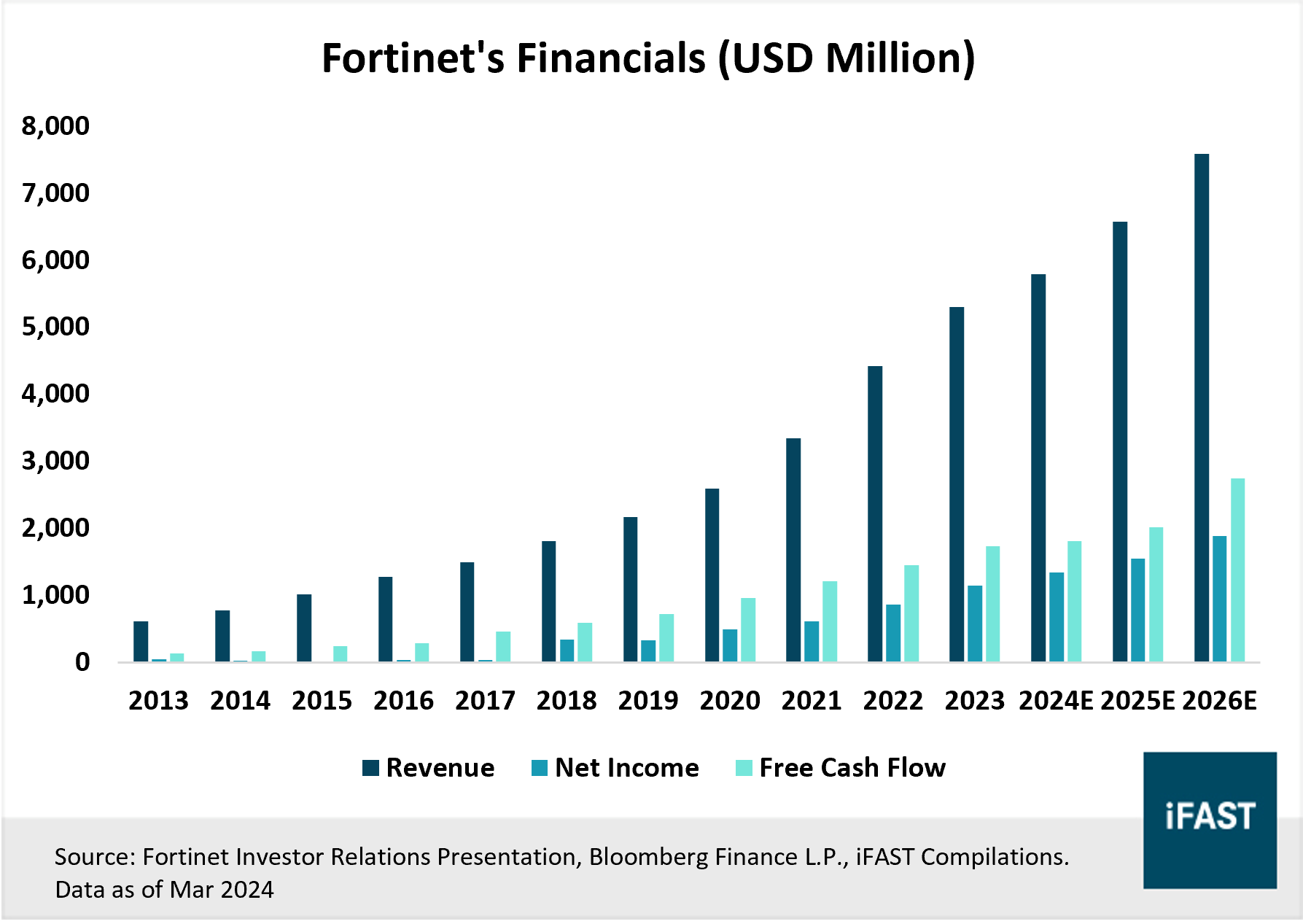

Impressive financials throughout the past few years

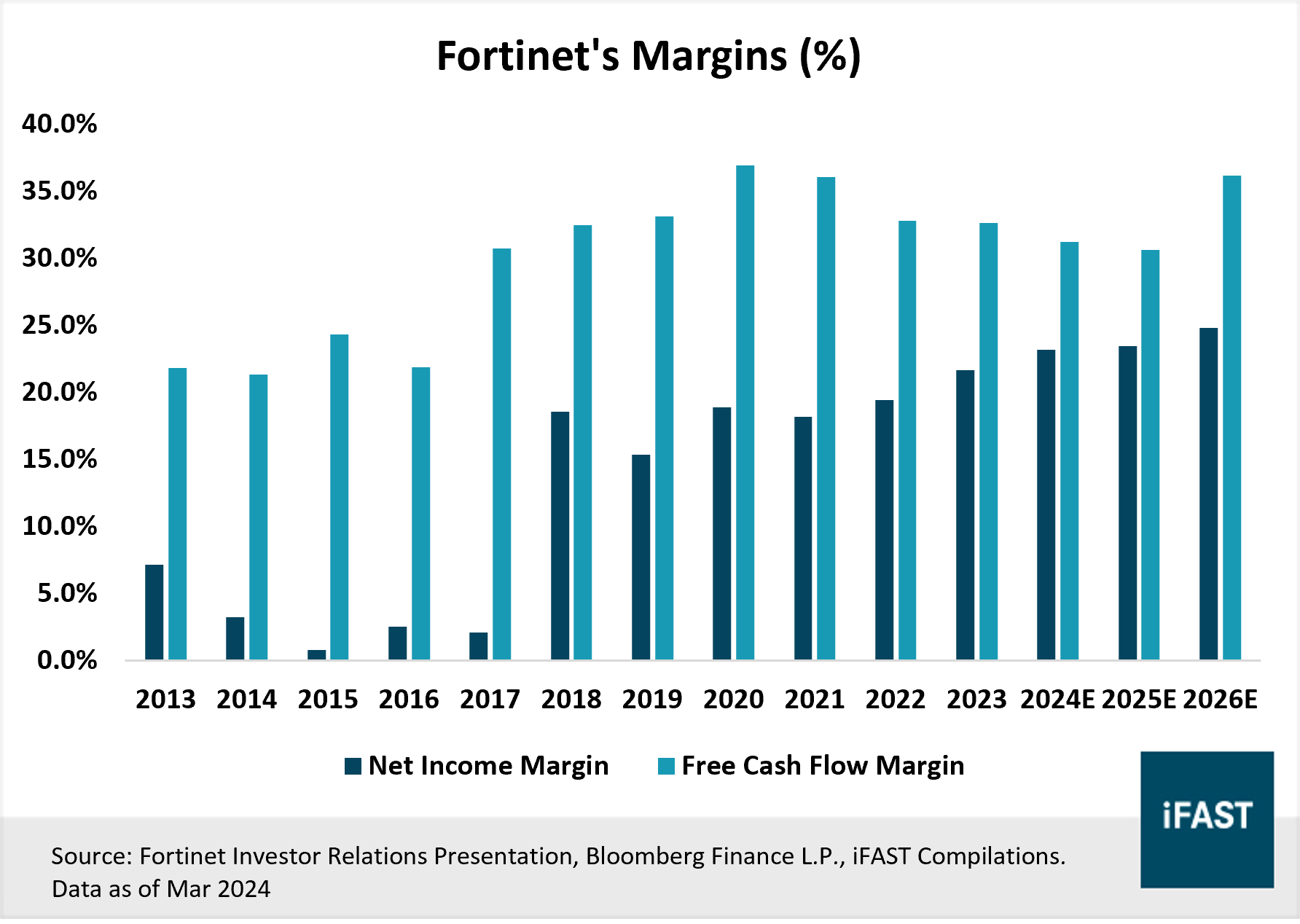

Fortinet has been demonstrating strong growth over the past decade. In fact, it has been growing rapidly, while demonstrating consistent profitability. For instance, with the announcement of its recent 4Q23 results, Fortinet’s revenue grew by 20.1% year-over-year (YoY) on a full year basis in 2023, while net income surged 34% YoY and free cash flow (FCF) grew 19.5% YoY.

We also note that Fortinet is operating a highly efficient and profitable business. In fact, its net profit margins have expanded over the past few years, increasing from 7.2% in 2013 to 21.6% in 2023. On top of increasing net profit margins, the company also demonstrated strong and growing FCF margins, which grew from 21.8% in 2013 to 32.6% in 2023 (Figure 4).

Figure 4: Fortinet’s margins have been expanding over the years

Taken together, over the past five years since 2019, Fortinet has grown its revenue at a compound annual growth rate (CAGR) of 24.1%. Similarly, Fortinet has also expanded its net income at a CAGR of 27.9% and its FCF at a staggering rate of 24.2% (Figure 5).

Figure 5: Profitable business operating at high efficiency throughout the years

Additionally, as of end 2023, Fortinet possesses a strong balance sheet, sitting on a net cash position, indicating that the company has sufficient cash on hand to pay down all its debt should it choose to. It also has a positive liquidity ratio with a current ratio of 1.19, indicating the company’s ability to pay off its short-term debt obligations using its current assets without raising external capital.

With such strong financials, operational efficiency and profitability in an ever-expanding market, Fortinet is a wonderful business to own.

Key investment risk:

Growth slowdown and delayed transition to establish new revenue mix: A slower than expected pickup in growth and transition to its newer product lineup would dampen investor sentiments. All in all, we believe this fear in growth slowdown has been overblown, especially when management has clearly stated that growth would normalise and accelerate towards the second half of 2024, once the business pivots more towards the Security Operations and Unified SASE business segments, which are more service-oriented with higher margins and existing in markets with faster growth rates.

Valuation looks attractive on both an absolute and relative basis

All in all, Fortinet is a market leader in multiple segments within the fragmented cybersecurity sector, due to its diversified business model and suite of products. We note that Fortinet possesses strong financials, displayed via its operational efficiency and profitability throughout the years. Furthermore, the company has a strong growth trajectory in a market that is set to grow rapidly.

Moreover, given that the earnings recession in the technology sector is behind us, we believe Fortinet’s earnings would also rebound and accelerate from here, as the growth of the technology sector would naturally increase the demand for cybersecurity solutions.

Related article: The earnings recession is over. Big Tech is set to lead the next phase of growth.

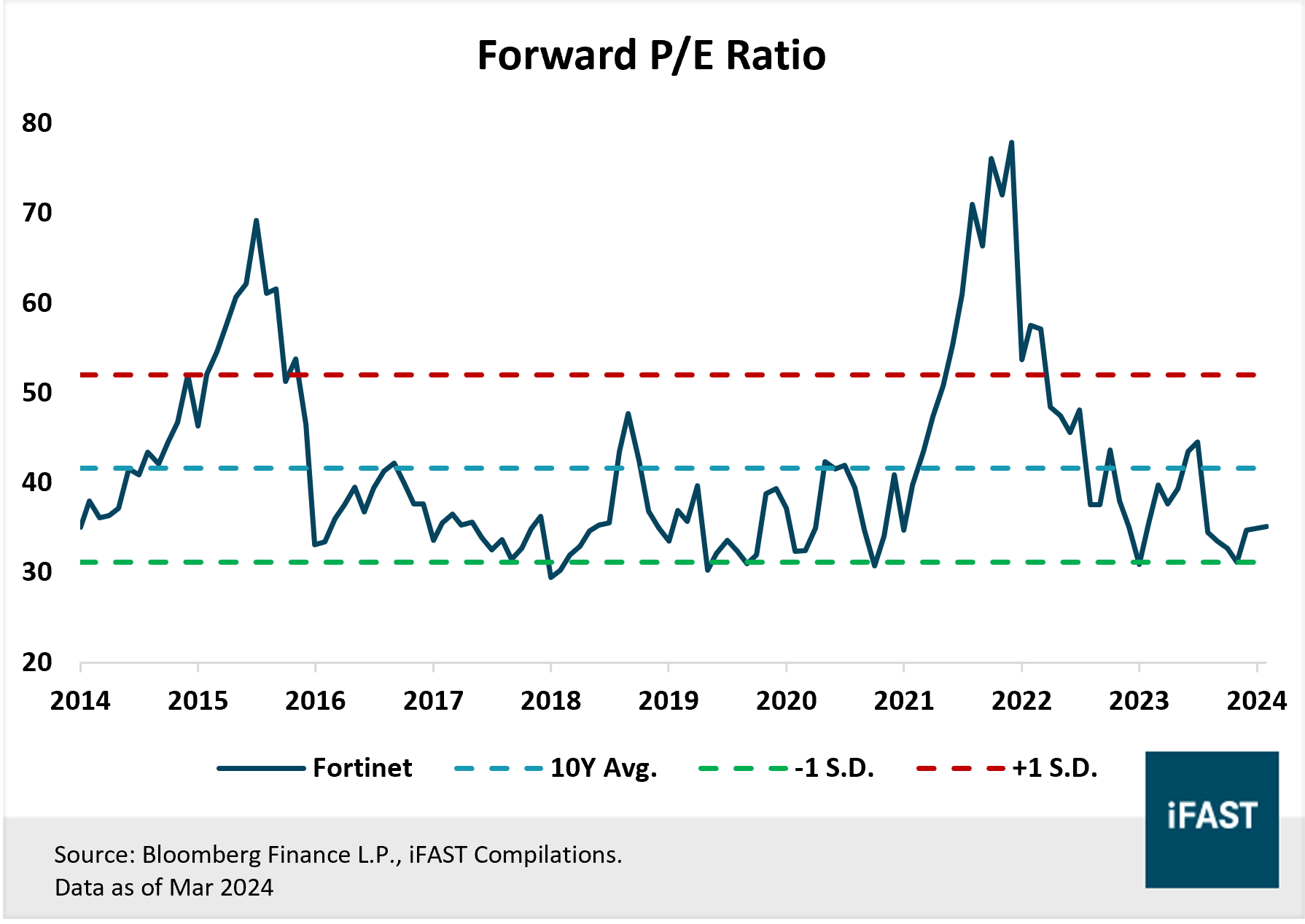

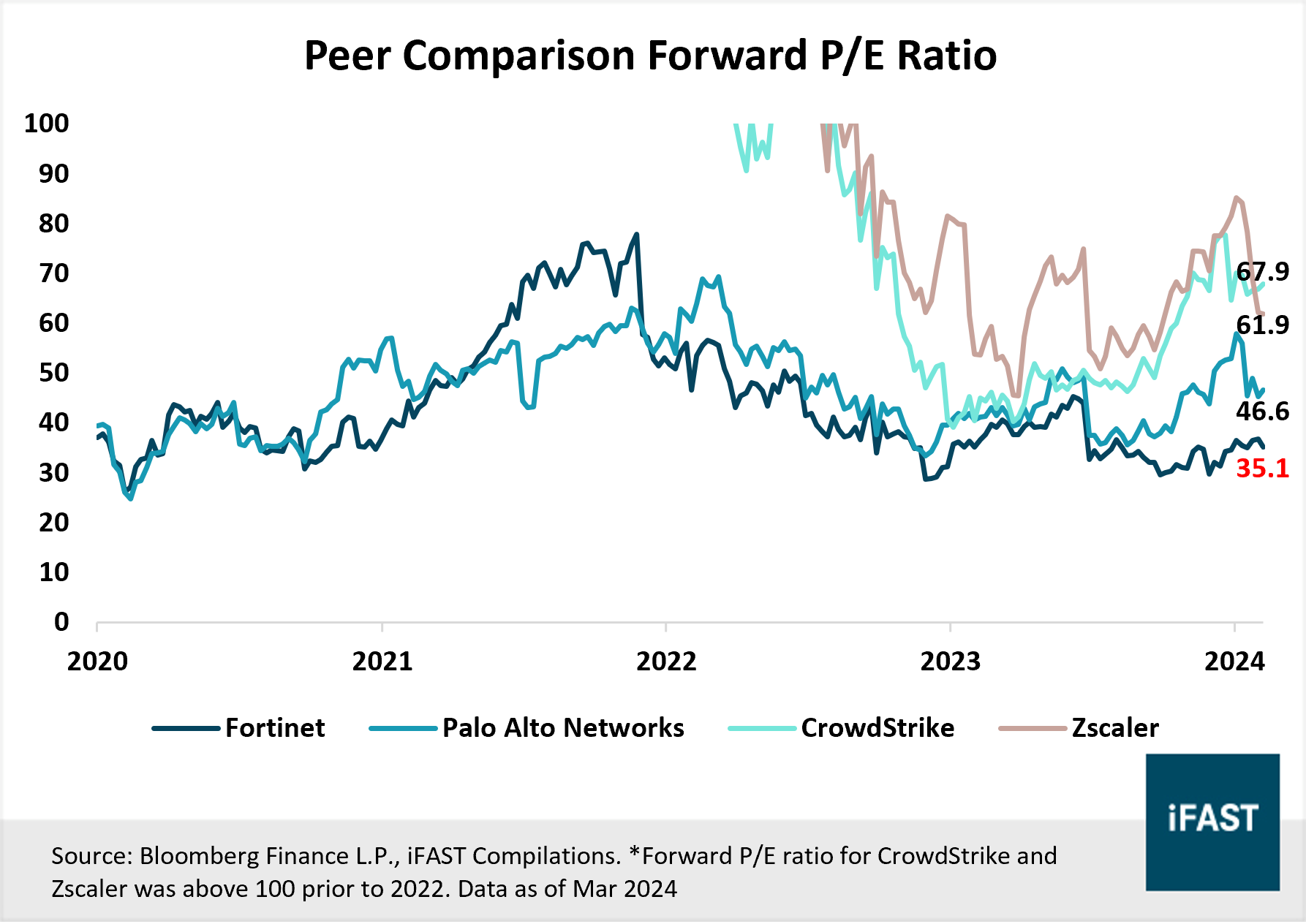

Valuations wise, Fortinet currently trades nearly one standard deviation below its past ten-year historical average P/E (Figure 6), and also trades at a significant discount to its larger peers. (Figure 7).

Figure 6: Fortinet is trading at a discount based off its historical P/E multiple

Figure 7: Fortinet trades at a significant discount relative to its peers in the sector

Based on a fair P/E multiple of 35X we have assigned to Fortinet, we have arrived at a target price of USD 84 by the end of 2026. This implies a potential upside of 24% based on the last closing price of USD 68.04 as of 14 March 2024 (Table 2). While we recommend Fortinet as a top cybersecurity company to invest in, more risk adverse investors who prefer to invest in the broader cybersecurity sector can also consider the Global X Cybersecurity ETF (NASDAQ:BUG).

Table 2: Projections for Fortinet earnings

|

Fortinet (NASDAQ:FTNT) |

2023 |

2024E |

2025E |

2026E |

|

PE Ratio (X) |

41.7 |

37.8 |

33.0 |

28.2 |

|

Projected Earnings Growth (YoY %) |

37.7% |

10.4% |

14.4% |

17.0% |

|

Projected Earnings Per Share (EPS) |

1.63 |

1.80 |

2.06 |

2.41 |

|

Target Fair Price (Based on a fair PE ratio of 35X) |

- |

- |

- |

84 |

|

Potential Upside (%) |

- |

- |

- |

24.0% |

|

Source: Bloomberg Finance L.P., iFAST Estimates |

||||

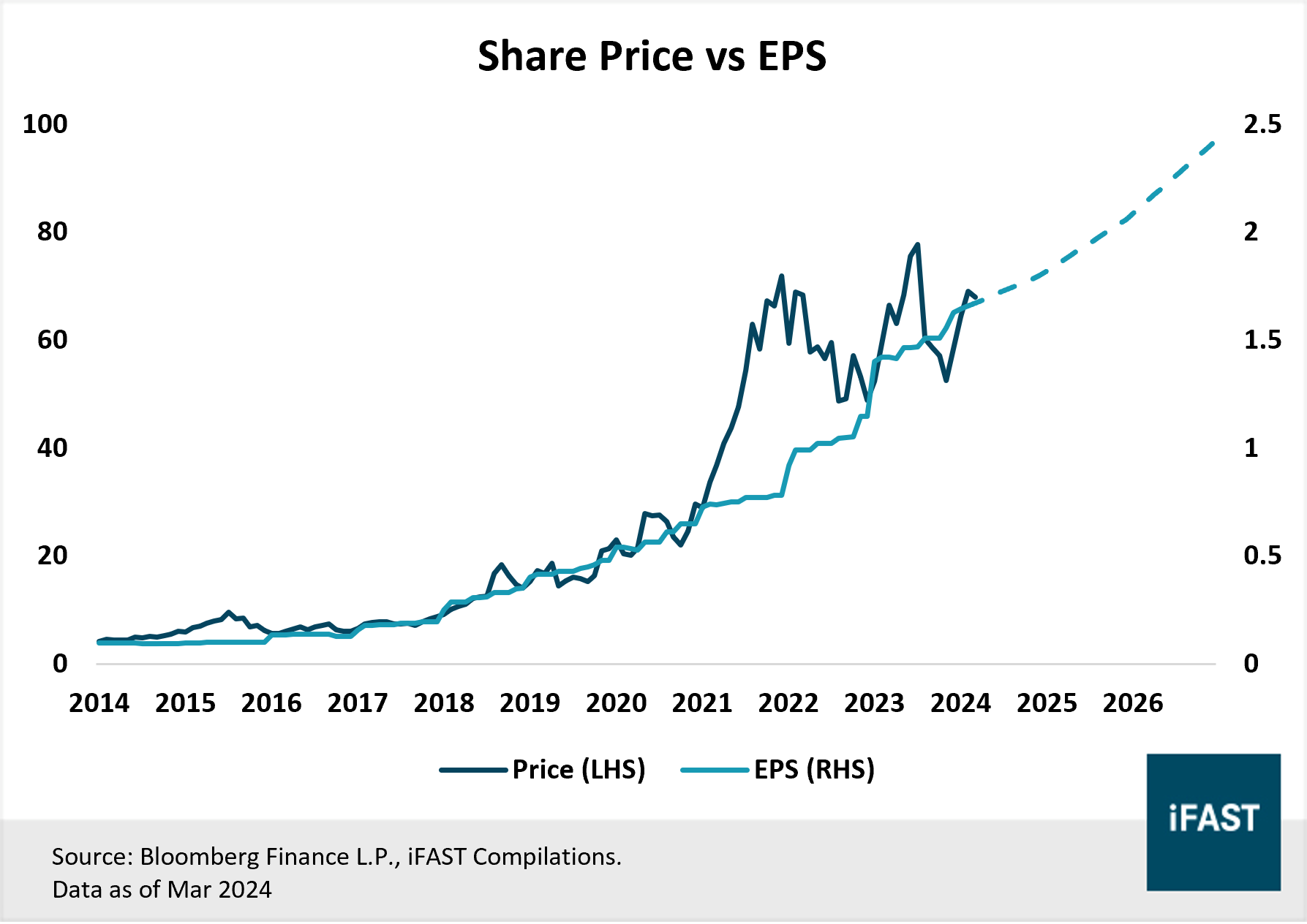

Figure 8: In the long-run, share price is driven by earnings

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")