' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

- Vietnam is shaping up as one of Asia’s economic success stories.

- Vietnam’s GDP grew 8% in 2022, bucking Asia’s general weakening growth trend.

- The long-term outlook is upbeat. Vietnam has long been the beneficiary of the relocation of manufacturing operations; the government is also committed to increasing corporate governance and upgrading critical financial markets infrastructure.

- Investors can consider allocating a portion of their portfolio towards Vietnam to tap into the country’s growth. It also complements traditional foreign exposure with investments beyond mainstream emerging markets.

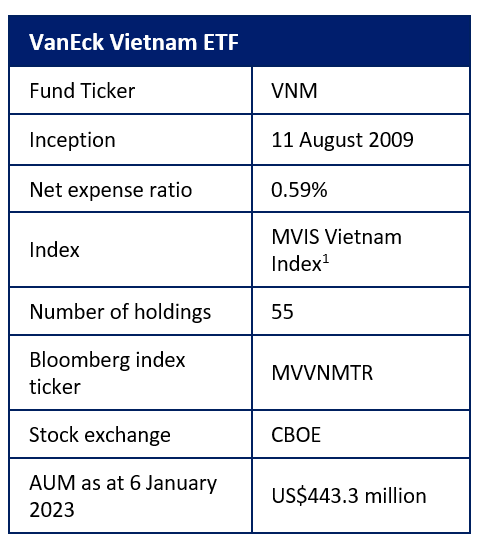

- Investors who want a pure play exposure on Vietnam can consider the VanEck Vietnam ETF (CBOE: VNM).

- There will be an upcoming index change effective on 17 March 2023. The fund’s current benchmark, MVIS Vietnam Index, will change to the MarketVector Vietnam Local Index.

- The new index only includes companies that are incorporated in Vietnam. With the index change, companies that are not incorporated in Vietnam will no longer be eligible for inclusion.

- VNM is the largest and most liquid US ETF that provides exposure to Vietnamese companies.

- Current valuations are attractive, which in our opinion are good entry points for potential investors.

Vietnam is shaping up to be one of Asia’s economic success stories.

During the COVID-19 pandemic, its apparent success in curbing the spread has helped the country maintain positive growth, compared to its regional neighbours that struggled to recover. China’s zero-COVID policy also triggered a new wave of investor interest into Vietnam.

Vietnam’s real GDP grew 8% in 2022 backed by strong domestic retail sales and exports. This upbeat growth bucks the trend in Asia, where most Asian economies are experiencing weakening growth.

Vietnam is a relatively young investable country and is great news for risk-tolerant investors who believe in the country’s potential.

Here are reasons why we are bullish on Vietnam.

China’s reopening will act as a cushion

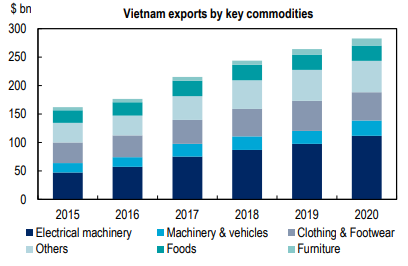

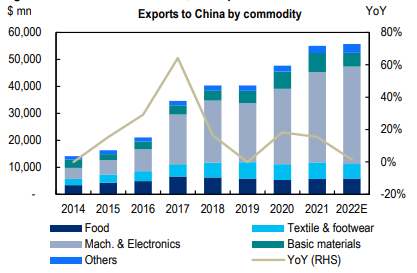

Firstly, amid expected recessions this year in the US and Europe, China’s reopening will act as a cushion for Vietnam. According to a report by Citi Research, the reopening of China will support the recovery of Vietnam’s exports, for items such as food, textiles and electronics.

Chart 1: Electronics comprise 40% of total exports

Source: Citi Research, CEIC Data Company Limited.

Chart 2: Outside of electronics, Vietnam exports food and textiles to China

Source: Citi Research Estimates, CEIC Data Company Limited.

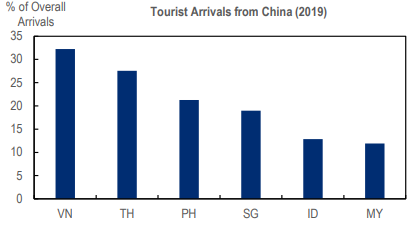

Before the COVID-19 pandemic, China tourists constituted over 30% of arrivals (Chart 3). Going forward, we think China’s reopening will also help the tourism industry recover.

Chart 3: Vietnam’s tourism industry pre-COVID was highly dependent on China

Source: Citi Research, CEIC Data Company Limited, Haver Analytics.

Long-term outlook supported by strong economic growth, FDI inflows and supportive government

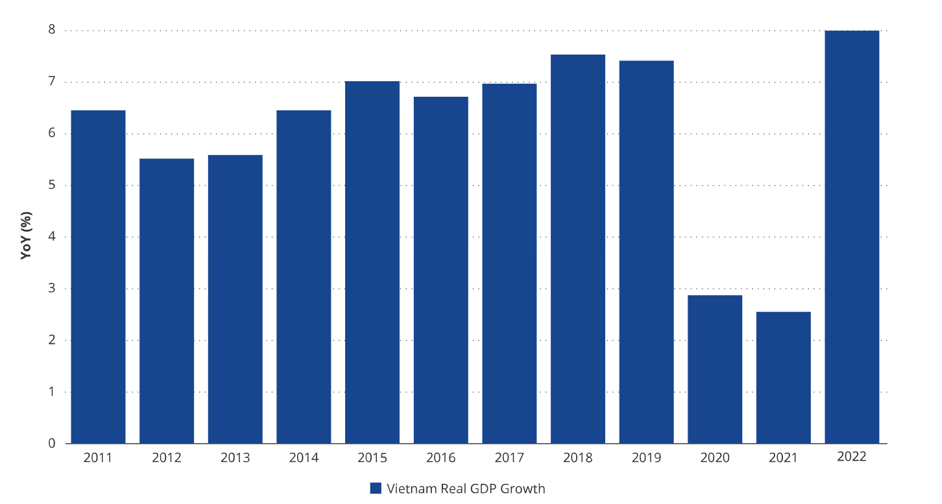

Overall, the long-term outlook is upbeat. The country has witnessed strong domestic consumption, received foreign direct investments (FDI) and maintained a surplus in trade balance with other countries. Vietnam’s GDP grew 8% in 2022, bucking Asia’s general weakening growth trend (Chart 4).

Chart 4: Vietnam real GDP growth

Source: CEIC Data, Jefferies, Reuters as of December 2022.

Vietnam is seen as a beneficiary of US-China decoupling with multinational companies looking to diversify assets out of China. China’s zero-COVID policy has aided the production shift into Vietnam. The country received FDI net inflows totalling US$15.3 billion in 2021, or 4.2% of GDP, up from 3.2% of GDP in 2013. We believe the strong FDI further solidifies the country’s macro outlook.

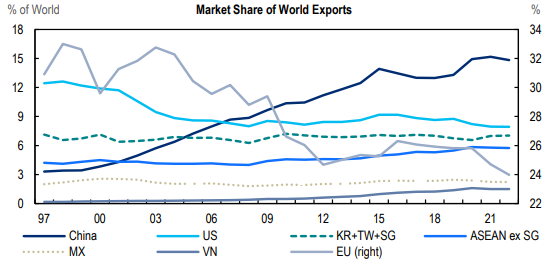

Additionally, Vietnam’s market share in global trade is expected to increase over the medium term. Even though it is still less than 2%, the number has been increasing. Vietnam has been on the receiving end of supply chain relocations as companies diversify their production base.

Chart 5: Vietnam commands a small portion of global trade but it is gaining market share

Source: Citi Research, CEIC Data Company Limited, Haver Analytics.

While other major world economies are curtailing fiscal and monetary policy support in an effort to contain inflation, Vietnam is in a position to support its growth. In January 2022, Vietnam passed a fiscal stimulus package of US$15.4 billion at almost 4% of its GDP to support its 8% growth target for the year.

Vietnam’s currency and interest rates also appear relatively stable compared to other countries. Vietnam’s contained inflation at around 4% and low borrowing costs with the central bank discount rate at 4.5%, are supporting a domestic consumption rebound as COVID-19 restrictions are easing. A sharp recovery in personal consumption along with strong export growth contributed to the country’s impressive Q3 2022 GDP growth of 13.67%. Vietnam’s strong macroeconomic position is expected to lift its population out of poverty as more than half of the Vietnamese population is projected to join the global middle class by 2035.

Looking ahead, the government is committed to increasing corporate governance and upgrading critical financial markets infrastructure.

Meanwhile, Vietnam is currently on the secondary emerging markets watch list by FTSE Indices and could be added to MSCI emerging markets watch list in 2023. Vietnam’s regulators are determined to help upgrade the country to emerging markets status.

Improving market liquidity

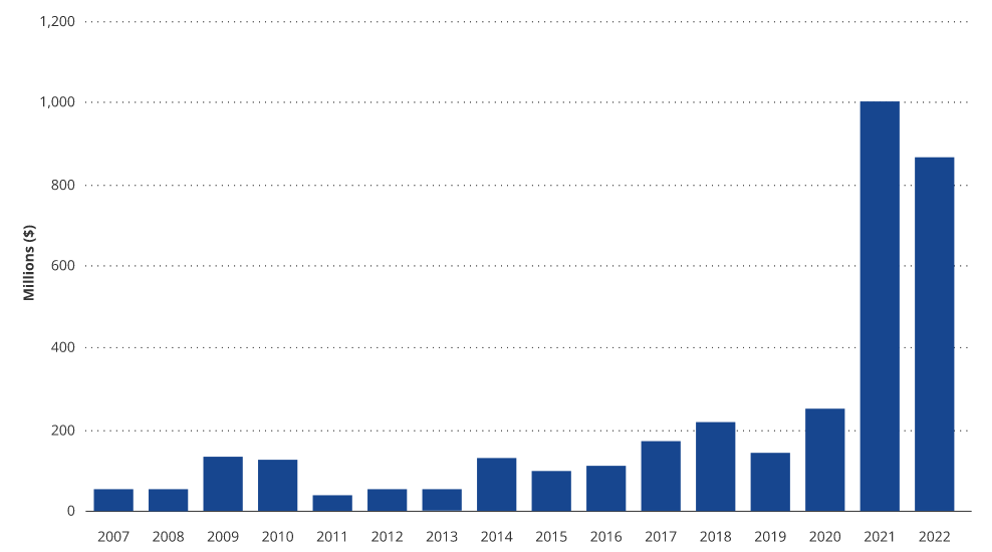

Vietnam’s market liquidity has also improved over the last few years with average daily trading volume rising from US$97 million in 2015 to US$1 billion in 2021. There are now at least fifty listed stocks with a market capitalisation of more than US$1 billion, indicating the growth of the market.

Chart 6: Vietnam stock market average daily turnover

Includes both Ho Chi Minh City and Hanoi stock exchanges. Source: Bloomberg Data.

VanEck Vietnam ETF

Although some emerging market ETFs include small holdings of Vietnamese equities, the VanEck Vietnam ETF (CBOE: VNM) is the closest thing to a pure play Vietnam ETF that investors can find. The fund tracks the MVIS Vietnam Index, which reflects the performance of the largest and most liquid companies that operate in Vietnam.

There will be an upcoming index change effective on 17 March 2023. The fund’s current benchmark, MVIS Vietnam Index, will change to the MarketVector Vietnam Local Index. The new index only includes companies that are incorporated in Vietnam. With the index change, companies that are not incorporated in Vietnam will no longer be eligible for inclusion.

Currently, VNM is trading at attractive valuations.

Chart 7: Attractive valuations for VNM

Source: Factset, 31 December 2022

Key points about VanEck Vietnam ETF (CBOE: VNM):

- VNM is the largest and most liquid US ETF that provides exposure to Vietnamese companies.

- Complements traditional foreign exposure with investments beyond mainstream emerging markets.

- The fund is highly levered to the Vietnamese consumer, with almost one-third of its combined weight to consumer staples and discretionary sectors.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")