' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

Demand uncertainty remained a key concern for semiconductor players in Q3 2022 as tech supply chain inventories continued to increase in the prior quarter. We expect inventories to peak exiting Q3 2022, with new order cuts underway and heading into high season demand. Memory makers face near-term downcycle but continue to focus on manufacturing technology migration, including the adoption of Extreme Ultraviolet (EUV) in DRAM (Dynamic random access memory). For investors, we believe these technological developments are key to watch and may provide favorable upside opportunities on the industry’s next upcycle.

Key Takeaways

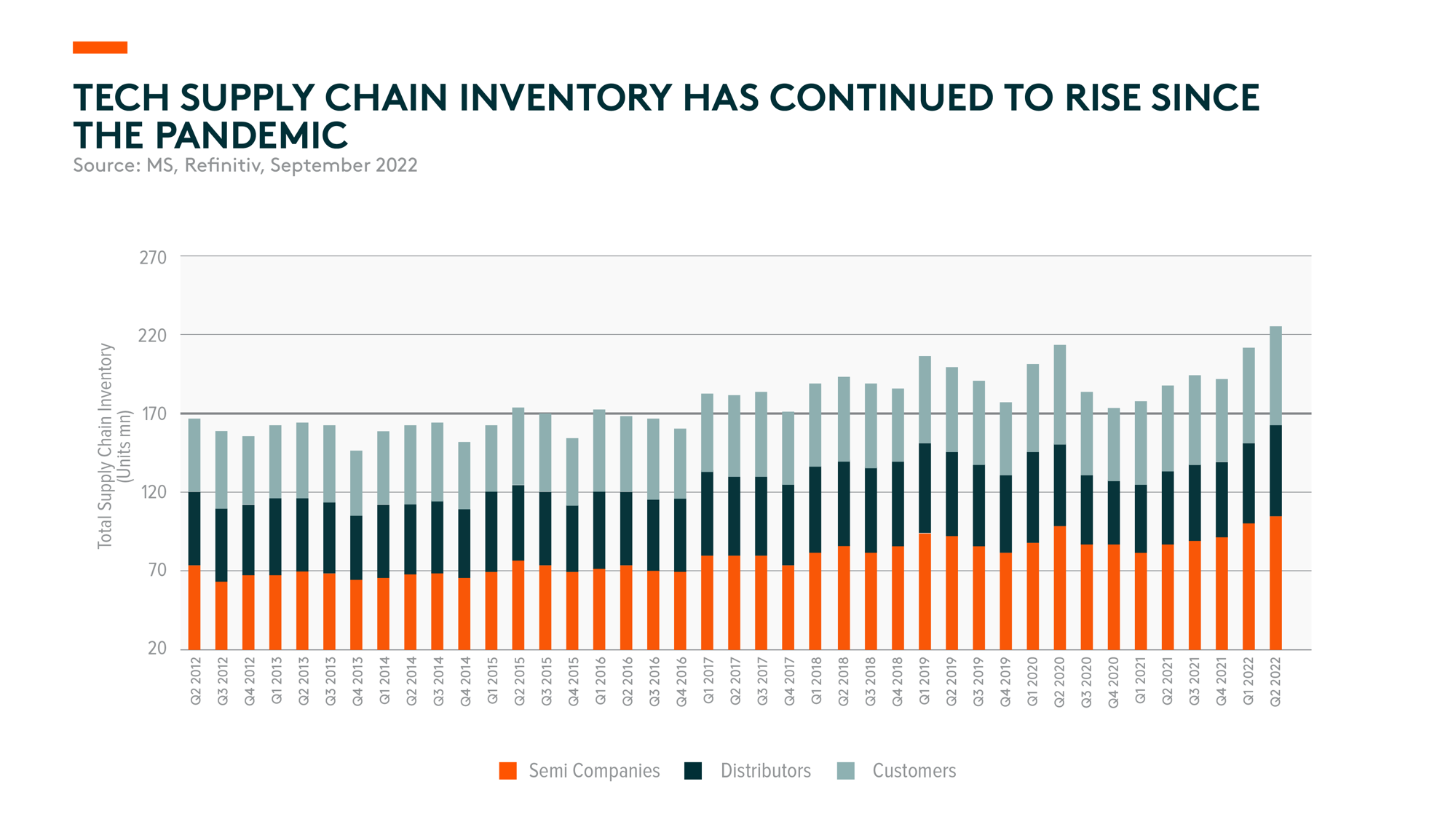

- Tech supply chain inventory continued to rise in Q2 2022, driven by slower end-market demand and supply chain concerns. For foundries, utilization rate remains high for top-tier foundries but lowered for tier-2 players. As we go into Q4 2022, more visibility on 2023 demand will help the industry execute necessary cuts to reach healthy demand-supply conditions.

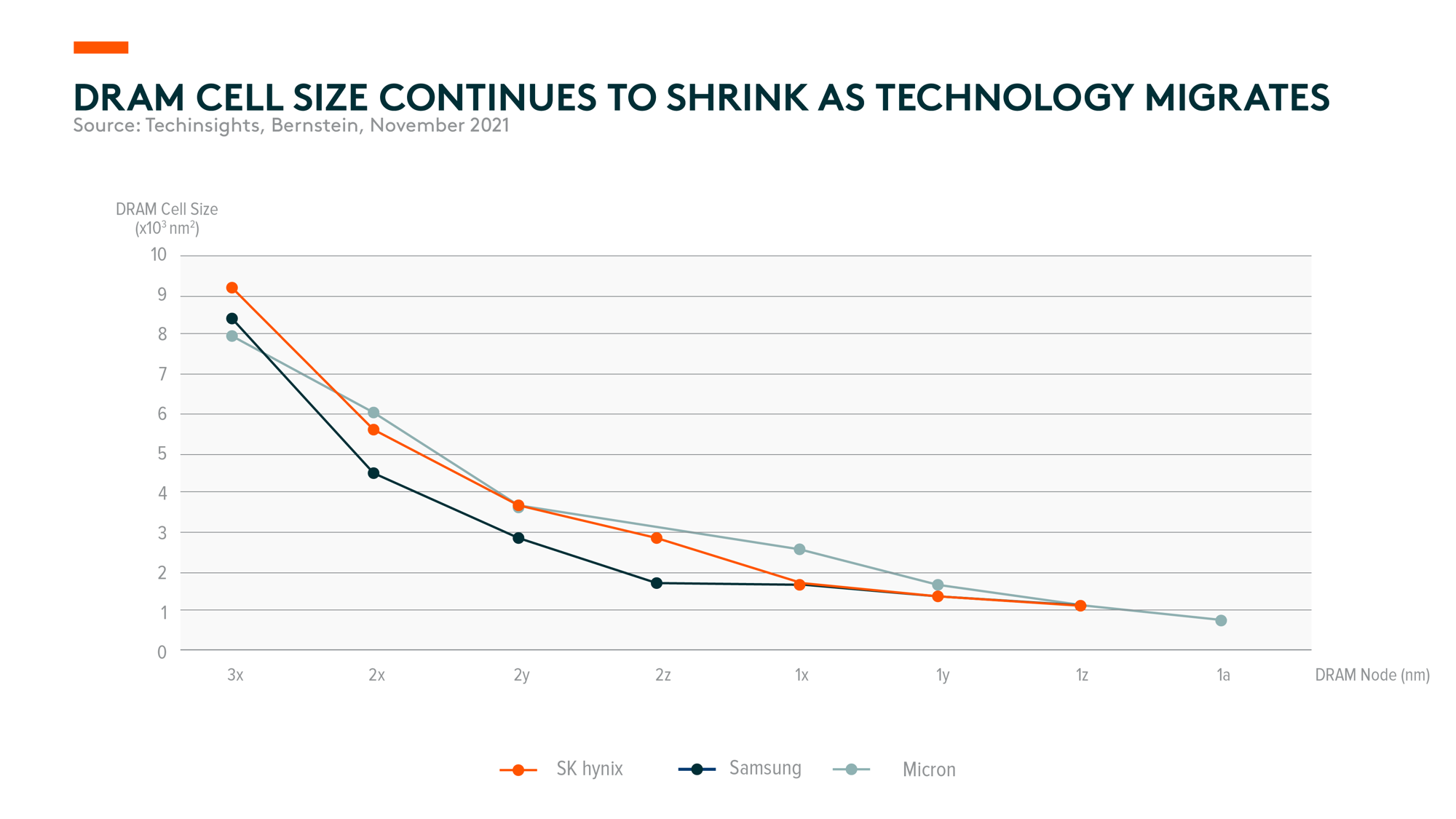

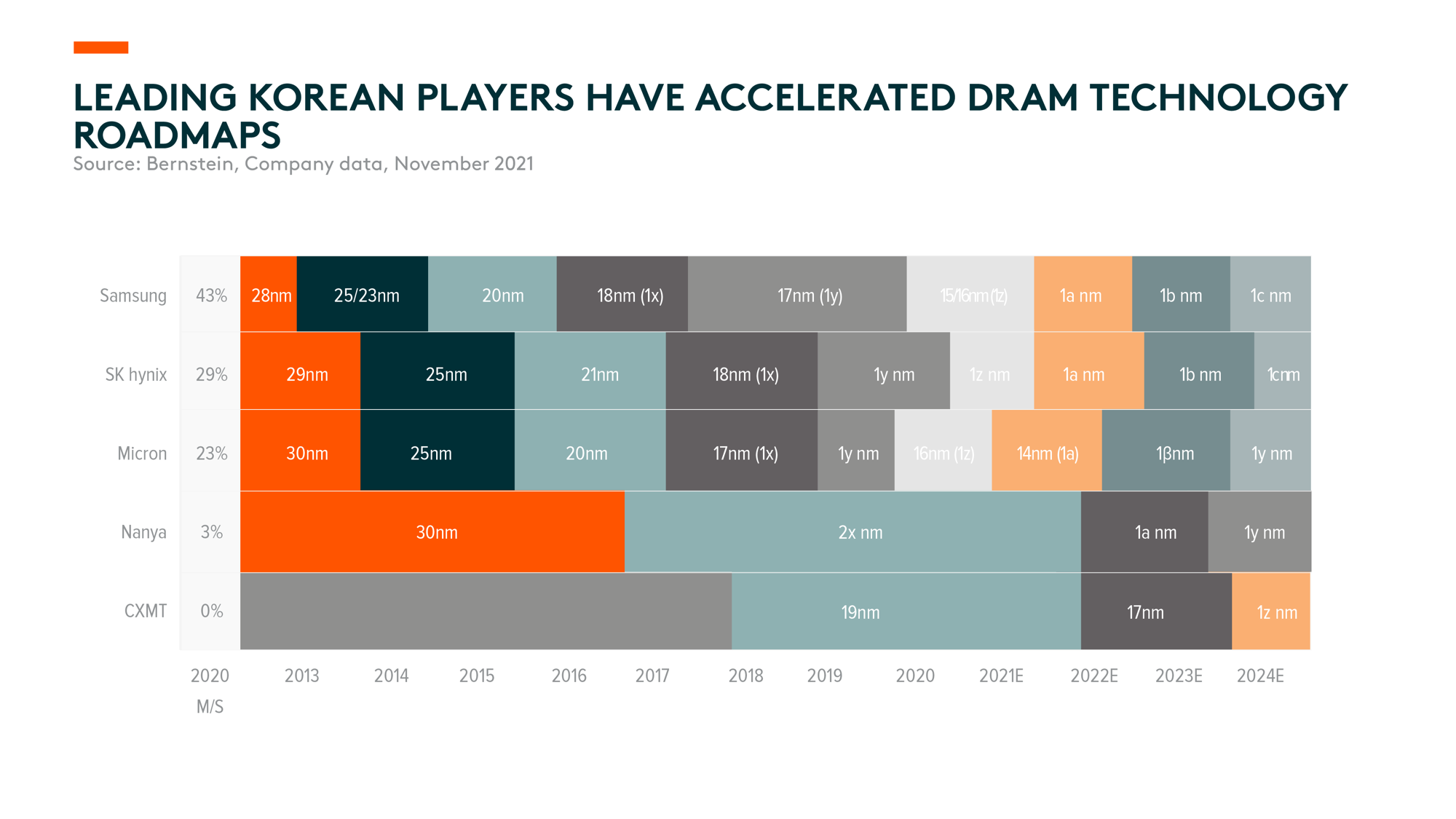

- The adoption of EUV lithography has been relatively low in DRAM compared to advanced logic semiconductors. But leading Korean memory makers are now leveraging the technique to drive greater bit growth per wafer and reduce costs.

Inventory Correction Underway

The tech supply chain inventory continued to move up in 2Q22. Semiconductor inventory was up 5 days quarter-on-quarter to 97 days in 2Q22, above the 86-day 2Q average since 2019 and the 71-day median over the past decade.1 The higher inventory is caused by slower end-market demand for tech and supply chain concerns since Covid-19. With order cuts now underway, inventory may peak exiting 3Q22 and start to lower with high season demand. We should get more visibility of 2023 demand going into 4Q22, which will help the industry execute necessary cuts to reach healthy demand-supply conditions. Auto IGBT (Insulated-gate bipolar transistor) and other industrial power chips are the only products under relatively tight supply.

Besides Apple and servers, the demand trend remains weak across most downstream verticals. Chinese Android smartphone suppliers continue to face a challenging macro environment in overseas markets and from the zero-COVID policy impact in China. The International Data Corporate (IDC) forecasts global smartphone shipments to decline by 6.5% year-on-year.2 However, iPhone demand remains healthy after the iPhone 14 launch, with a longer lead time for the iPhone Pro/Pro Max models. For PC, demand deterioration impacts the semiconductor supply chain. The IDC has again reduced its global PC shipment forecast from -8.2% to -12.8% year-on-year in 2022, representing 305.3 million units.3

For foundries, utilization rate remains high in 2H22 for top-tier players like TSMC. Ongoing weakness from terminal makers will likely impact the utilization rate in 1H23 as fabless companies adjust their orders to work down inventory. Key US customers such as AMD and Nvidia are already hit by weaker-than-expected demand. Tier 2 foundries’ utilization rate has moved lower amid an oversupply of various consumer electronics-related semiconductors like display driver integrated circuits, radio-frequency chips, image sensors, etc.

Despite order cuts broadening and the drop in utilization rates, we are yet to see any major cracks appear in foundry pricing. In fact, TSMC is expected to raise its wafer price by a single-digit percentage in 2023. We expect foundries and memory makers to announce 2023 CAPEX cuts as they draft their budgets, which will impact semiconductor equipment suppliers.

Increasing Adoption of Extreme Ultraviolet in DRAM manufacturing

A key focus for memory makers is to achieve the highest bit growth per wafer with the lowest cost. EUV lithography uses shorter wavelengths at 13.5 nanometres (nm). Compared to Deep Ultraviolet (DUV) lithography, which uses 193nm wavelengths, EUV enables the drawing of finer circuitry, and thus the same amount of surface area can store more data.

EUV has been used extensively in the production of advanced logic semiconductors. But for DRAM, the adoption is relatively low. There are several challenges with the application of EUV in DRAM, such as the yield of EUV mask blanks, capacitor design, etc. DUV processes typically use multiple masks to create a single wafer due to the complexity of the circuits. More masks used means more process steps are required, lengthening the production lead time and leading to higher costs. On the other hand, EUV can draw circuits in smaller and more detailed formations, which enables the adoption of single patterning. Single patterning with improved yields will save time and cost.

Samsung is one of the industry’s earliest adopters of EUV for DRAM. Their use of EUV will notably widen in 1-alpha nm process nodes, with the number of EUV layers extending to five layers for DDR5 (Double data rate 5) products. As a result, the company expects EUV to bring around a 10% cost advantage in DRAM. Elsewhere in South Korea, SK Hynix plans to use EUV technology for the production of all its 1-alpha nm DRAM products going forward. The company projects 1-alpha nm to achieve a 25% increase in the number of DRAM chips produced from the same size wafer compared to the earlier 1z nm node. In the US, Micron’s plans for EUV adoption are slower. The company will not use EUV for production until 1-gamma nm for limited layers and 1-delta nm for more layers.

Overall, bit density improvement has been slowing in recent years. Considering the relatively limited scale of EUV adoption to date, the cost benefits have not been reflected in financial results in a noticeable manner yet.

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")