' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

- The resurgence of value stocks and inflation worries this year have buoyed the VanEck Vectors Morningstar Wide Moat ETF (BATS: MOAT and ASX: MOAT), even though it is not a dedicated value ETF.

- Growing optimism in the global economic recovery may continue to support the rally in value stocks, as investors increase their exposure to value-oriented stocks to hedge against inflation.

- MOAT tracks the Morningstar Wide Moat Focus Index, which screens for companies that prove to have a sustainable competitive advantage and a favourable valuation.

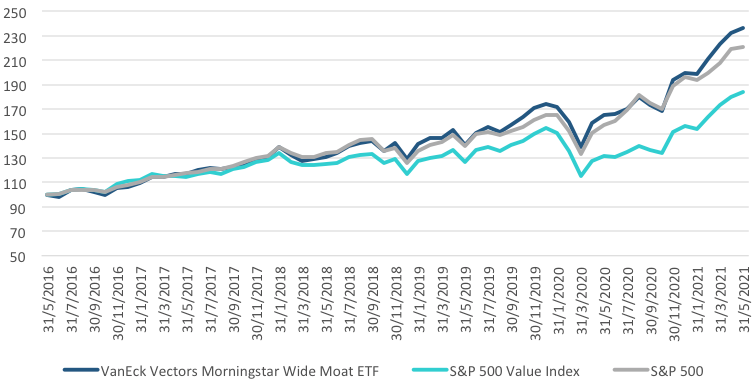

- The quality/value combination is proving beneficial this year. It has helped MOAT outperform the broader US equity market for the calendar year through May 2021, as well as over the longer term horizon as the fund shifted towards a “value” bias (Figures 1 and 2).

- A focus on valuations has long been the cornerstone of Morningstar’s moat investment philosophy, and investors seeking to diversify their portfolios should consider investing in MOAT, listed in the US and Australia (BATS: MOAT and ASX: MOAT). There is also a MOAT UCITS ETF.

Stellar performance

The VanEck Vectors Morningstar Wide Moat ETF (BATS: MOAT and ASX: MOAT) is benefiting from the resurgence of value stocks and investors’ growing concern over inflation. While MOAT is not a dedicated value ETF, the fund is gaining from the revival of value stocks this year. The ETF tracks the Morningstar Wide Moat Focus Index, and its quality/value combination over the past year has rewarded investors with outperformance of nearly 600 basis points relative to the S&P 500 for the calendar year through May. Over the one, three and five-years periods ending 31 May 2021, the fund also outperformed both the S&P 500 Value Index and the S&P 500 (Figures 1 and 2).

Figure 1: Moat’s outperformance

Source: Morningstar Direct. Data as of 31 May 2021. The above chart represents past performance of the fund and the index. Past performance is no guarantee of future performance.

Figure 2: Average Annual Total Returns* (%)

|

|

1 mth (%)

|

3 mth (%)

|

YTD (%)

|

1 Year (%)

|

3 Years (% p.a.)

|

5 Years (% p.a.)

|

MOAT Inception 24 Apr 2012 |

|

MOAT ETF (NAV) |

1.53 |

12.08 |

18.15 |

42.72 |

21.70 |

18.74 |

16.71 |

|

S&P 500 |

0.70 |

10.72 |

12.62 |

40.32 |

18.00 |

17.16 |

15.42 |

|

S&P 500 Value |

2.41 |

12.89 |

17.68 |

39.84 |

13.82 |

13.00 |

12.62 |

Two of the recent stock additions to the MOAT index – Northrop Grumman Corp and Google’s parent company, Alphabet – were among the key contributors to the fund’s performance.

Northrop Grumman reported strong first-quarter results in late April, driving its price higher to where it now trades at approximately 10% above fair value, according to Morningstar. The US defence contractor’s wide economic moat stems from intangible assets related to product complexity and long contract life spans paired with switching costs associated with the mission-criticality of product, extended product cycles, a lack of viable alternative products, and the substantial time investment required for switching.

Alphabet benefits from intangible assets and network effect. Morningstar believes its intangible assets are related to its overall technological expertise in search algorithms and machine learning as well as its access to and accumulation of data deemed valuable to advertisers. Add to that the obvious brand associated with “Googling” something. Alphabet’s network effect is created from its ability to collect data through an extensive network and, in turn, offer the best return on investment for advertisers, further building its network of advertising customers.

Inflation-fighting moat stocks

Lately inflation fears have built up amid the rising price pressures. Although companies are not immune from rising costs, US large-cap stocks have historically weathered inflationary environments better than other asset classes.

Some sectors such as commodity-related materials and industrials stand to benefit from rising inflation. Other more defensive sectors, such as utilities with steady cash flows, are expected to be negatively impacted by inflation. And because the MOAT Index’s focus on valuations has shifted its sector exposure over time, it is hard to predict how it will be positioned when inflation takes centre stage.

Investors looking at a broad-based core US equity strategy may be better off focusing on companies that have built sustainable competitive advantages if inflation persists. Many of these wide moat companies have pricing power that allow them to pass rising costs to consumers. In at least some way, all five sources of economic moat identified by Morningstar contribute to a company’s pricing power and expected ability to maintain profitability in the long term.

Key points of MOAT:

Consider MOAT when positioning your portfolio to include US equity holdings:

- MOAT boasts a history of long-term outperformance.

- MOAT provides investors with exposure to 49 of the most attractively-priced US wide moat companies, which Morningstar believes can deliver consistent earnings for 20 years, via a single trade.

- MOAT is a high conviction US strategy with low passive fees.

Disclaimer:

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")