' fill='%23fff' stroke='%23707070' d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='c'%3e%3cpath data-name='Rectangle 6531' transform='translate(-6319 -2048)' fill='%23fff' stroke='%23707070' d='M0 0h43.2v21.6H0z'/%3e%3c/clipPath%3e%3cclipPath id='a'%3e%3cpath d='M0 0h21.6v21.6H0z'/%3e%3c/clipPath%3e%3c/defs%3e%3cg data-name='Malaysia -Square' clip-path='url(%23a)'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='Mask Group 325' transform='translate(6348 2048)' clip-path='url(%23b)'%3e%3cg data-name='Mask Group 324' transform='translate(-35)' clip-path='url(%23c)'%3e%3cg data-name='Group 21195'%3e%3cpath data-name='Path 14718' d='M-6319-2048h43.2v21.6h-43.2z' fill='%23fff'/%3e%3cpath data-name='Path 14719' d='M-6317.457-2047.229h41.657m0 3.086h-41.657m0 3.086h41.657m0 3.086h-41.657' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3cpath data-name='Path 14720' d='M-6319-2048h21.6v13.114h-21.6z' fill='%23006'/%3e%3cpath data-name='Path 14721' d='M-6319-2034.886h43.2m0 3.086h-43.2m0 3.086h43.2' fill='none' stroke='%23c00' stroke-width='1.543'/%3e%3c/g%3e%3cpath data-name='Path 14722' d='M-6302.5-2045.686l.344 2.353 1.331-1.967-.714 2.269 2.054-1.2-1.626 1.731 2.372-.19-2.218.858 2.218.858-2.372-.19 1.626 1.736-2.054-1.2.714 2.269-1.331-1.97-.344 2.358-.344-2.353-1.331 1.97.714-2.269-2.054 1.2 1.626-1.737-2.372.19 2.218-.858-2.218-.859 2.372.19-1.626-1.736 2.054 1.2-.714-2.267 1.331 1.97zm-1.929.1a4.114 4.114 0 100 7.521 4.629 4.629 0 110-7.521z' fill='%23fc0'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "malaysiaIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='067-hong-kong'%3e%3cpath data-name='Rectangle 6488' fill='%23d80027' d='M0 0h22v22H0z'/%3e%3cg data-name='Group 21086' fill='%23f0f0f0'%3e%3cpath data-name='Path 14432' d='M11.911 8.264c-.248 1.032-.689.835-.905 1.735a2.373 2.373 0 011.109-4.614c-.429 1.803.018 1.956-.204 2.879z'/%3e%3cpath data-name='Path 14433' d='M8.606 9.029c.9.555.581.913 1.37 1.4a2.373 2.373 0 01-4.045-2.481c1.577.964 1.866.586 2.675 1.081z'/%3e%3cpath data-name='Path 14434' d='M8.311 12.409c.807-.689 1.048-.271 1.752-.871a2.373 2.373 0 11-3.609 3.081c1.408-1.202 1.136-1.594 1.857-2.21z'/%3e%3cpath data-name='Path 14435' d='M11.435 13.734c-.406-.98.066-1.08-.287-1.935a2.373 2.373 0 111.815 4.385c-.708-1.71-1.165-1.573-1.528-2.45z'/%3e%3cpath data-name='Path 14436' d='M13.66 11.173c-1.058.083-1.007-.4-1.929-.325a2.373 2.373 0 114.731-.371c-1.846.145-1.856.621-2.802.696z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "hongKongIcon")

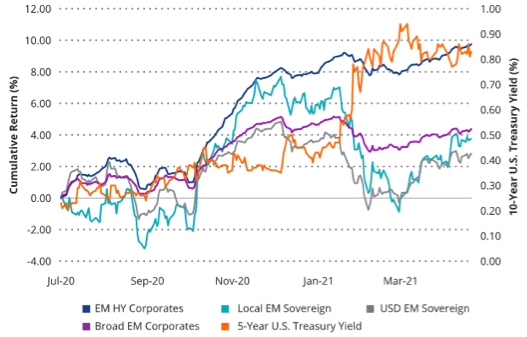

- Emerging markets high yield (EM HY) corporate bonds have been a bright spot within emerging markets debt over the past year, despite the increase in US interest rates.

- EM debt has historically reacted positively to a rising rate environment, particularly if rates are rising because of improving growth outlook.

- This makes sense, given that higher US growth tends to lead to higher imports from EM countries, increased capital flows, and generally greater risk appetite.

- In addition to a shorter duration and higher spread buffer against rising rates, we believe EM HY corporate bonds are well positioned to benefit from the spike in expected global growth rates this year, and investors can gain exposure to this via the VanEck Vectors Emerging Markets High Yield Bond ETF (NYSE: HYEM).

Standout performers

EM HY corporate bonds have been the brightest spots within EM debt in the past year, despite the increase in US interest rates that began last summer and accelerated at the beginning of 2021.

This segment of the market may also be relatively more insulated from higher local interest rates and fluctuations in the US dollar, while the global exposure of many of the issuers allows the category to benefit from the spike in expected global growth rates this year. At the same time, EM HY corporates are one of the few areas where investors can still find yields that are still well above 5%.

Figures 1 and 2: EM HY corporates outperform amid rising rates

|

|

Index |

Wtd. Average Yield |

Effective Duration |

|

EM HY Corporates |

ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index |

5.41 |

3.6 |

|

Local EM Sovereign |

JPM GBI-EM Global Diversified Index |

4.81 |

5.2 |

|

USD EM Sovereign |

JPM EMBI Global Diversified Index |

4.44 |

7.9 |

|

Broad EM Corporates |

ICE BofA US Emerging Markets Liquid Corporate Plus Index |

3.46 |

5.3 |

Sources: ICE Data Indices, J.P. Morgan and Morningstar, as of 5/21/2021. Timeframe for data reflects rise of interest rates.

Factors driving performance

The lower interest rate sensitivity of emerging markets high yield corporates, compared to other US dollar denominated EM debt sectors, has been a key driver of outperformance vs broad EM corporate debt over the past year as interest rates rose (see index definitions in table above).

EM HY corporates have a duration of 3.6, compared to 5.3 of broad EM corporates and nearly 8 of USD EM sovereigns. Further, the segment’s duration has remained close to where it was five years ago. The duration of USD EM sovereigns, on the other hand, has extended significantly from about 6.7 five years ago, while the duration of broad EM corporates was about 4.6 five years ago.

In addition to the shorter duration, EM HY corporates benefit from a high average spread, which provides a potential cushion against rising rates. For the year-to-date through 21 May 2021, the average spread has tightened by 41 basis points, nearly offsetting the 47 basis point increase in the 5-Year US Treasury yield.

The upshot, of course, is that spreads are now at historically tight levels. However, EM HY corporates continue to provide a spread pickup of 135 basis points vs US HY corporate bonds.

Further, with what we view as expected strong global growth, continued easy monetary policies and very benign credit conditions, it is difficult to identify a likely catalyst for widening out, particularly if the recent calmer tone in US interest rates continues. In addition, we believe with the current high exposure to energy (15%) and Basic Industry (16%), EM HY corporates may continue to benefit from the upswing in global commodity prices.

Key points of HYEM:

- Focuses solely on the non-sovereign segment of the HY EM bond market

- Yield pickup and currently lower duration vs US HY corporate bonds

- Adds issuer and country diversification to a US-only high yield exposure

|

Fund details |

as of 1 June 2021 |

|

Distribution yield |

5.51% |

|

Effective Duration (yrs) |

3.57 |

|

Years to Maturity |

7.90 |

|

Distribution Frequency |

Monthly |

|

Exchange |

NYSE Arca |

' d='M0 0h300v57H0z'/%3e%3c/svg%3e "sgFsmLogoEnIcon")

'%3e%3cpath fill='%23fff' d='M0 0h21.6v21.6H0z'/%3e%3cg data-name='141-singapore'%3e%3cpath data-name='Rectangle 6502' fill='%23f0f0f0' d='M0 0h22v22H0z'/%3e%3cpath data-name='Rectangle 6503' fill='%23d80027' d='M0 0h22v10H0z'/%3e%3cg data-name='Group 21092' fill='%23f0f0f0'%3e%3cpath data-name='Path 14455' d='M2.917 5.365A3.128 3.128 0 015.374 2.31a3.128 3.128 0 100 6.11 3.128 3.128 0 01-2.457-3.055z'/%3e%3cpath data-name='Path 14456' d='M6.939 2.46l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14457' d='M5.193 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14458' d='M8.68 3.801l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14459' d='M8.01 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3cpath data-name='Path 14460' d='M5.863 5.811l.222.683h.718l-.581.422.222.683-.581-.422-.581.422.222-.683-.581-.422h.718z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e "singaporeIcon")

' d='M0 0h67v14H0z'/%3e%3c/svg%3e "msFooterLogoIcon")